Compass Minerals: A High Dividend Stock With Unique Assets

Compass Minerals (CMP) boasts an operating history dating back to 1844 and is a leading producer of essential minerals, with 22 global production facilities around the world. Specifically, Compass Minerals primarily sells:

Salt: used mainly by cities for deicing roads but has many consumer and industrial applications as well.

Specialty potash: a premium fertilizer that improves the quality, yield, and shelf life of high-value crops.

Micronutrients: essential minerals that maximize plant yields.

Magnesium chloride: used in numerous ways including roadway deicing, dust control, and as plant nutrients for wheat crops.

Compass Minerals owns a handful of salt mines (including the largest rock salt mine in the world in Canada) and solar evaporation facilities (including the only sulfate of potash production site in North America) that it uses to produce most of its minerals. The business has shifted its mix significantly in recent years. Salt accounted for nearly 80% of sales in 2015 but was less than 60% of revenue in 2018 as Compass diversified the business into specialty plant nutrition products.

The company organizes its business into three segments:

Salt (57% of 2018 sales): about 60% of this segment's revenue is generated from sales of highway deicing salt. The remainder consists of salt sales to consumer and industrial markets for use in water conditioning, ice control, food processing, table salt, animal nutrition, plastics, and more.

Plant Nutrition South America (26% of sales): consists of the operations of Produquímica, a Brazilian company which Compass Minerals acquired for $465 million in October 2016. This business makes a wide array of specialty plant nutrients, and supplements developed and formulated from essential primary and secondary nutrients, micronutrients, and biostimulants. Over 70% of sales are related to agricultural products, with the remainder derived from chemical solutions mostly used in water treatment.

Plant Nutrition North America (16% of sales): sells specialty potash fertilizer used on high-value or chloride-sensitive crops. This segment also sells micronutrients, which play important roles in plant development (nutrient deficient soils must be replenished to obtain higher crop yields).

Overall, 38% of the company's revenue is from deicing salt, 26% from consumer and industrial salt (most of which is also used for deicing), and 36% from plant nutrition.

By geography, the company's revenue breaks out as follows: 52% from the U.S., 26% Brazil, 18% Canada, 6% U.K., 1% other (mostly the EU).

Compass Minerals increased its dividend every year since going public in 2003 but has kept its payout frozen since early 2017 in light of several macro and company-specific challenges.

Business Analysis Compass Minerals' primary advantages are its mineral production sites and logistical networks, which create meaningful barriers to entry and pricing power. Before diving deeper, it’s worth mentioning the relatively attractive characteristics of salt.

Salt is mostly a non-discretionary purchase that has no economic substitutes or alternatives today. Governments must buy salt to keep their roadways safe, regardless of how well the economy is doing.

Over the past 30 years, the production of salt used in highway deicing and for consumer and industrial products in the U.S. has increased at a historical average of approximately 1% per year, according to the U.S. Geological Survey. Over the past 15 years, salt prices in the US have grown at a 3.9% average annual rate and hit $74 in 2018.

The cost of salt typically represents less than 1% of a government’s budget, helping Compass Minerals' pricing ability because its products are a relatively small burden on the budget.

Governments purchase salt by taking in bids between April and October. They award a 12-month contract to the lowest bidder, and most contracts have a minimum volume clause (typically 80%) and fix pricing over the duration of the deal.

Governments keep only enough rock salt on hand for 2-3 applications because it’s too bulky for them to store in large quantities. They reorder as their supply is used, which can significantly shift the supply-demand dynamic in favor of salt producers during extreme winter weather events. Compass Minerals' average price on awarded highway deicing contracts rose by 25% in 2014 as a result of an unusually high number of snow events, for example.

With that said, rock salt is a commodity. What makes it an attractive business for Compass Minerals?

For one thing, with Compass Minerals' highway salt fetching an average selling price of $74 per ton in 2018, the weight-to-value ratio is extremely high for salt. It quickly becomes clear that production and shipping costs define a salt company’s service area. In fact, transportation costs typically account for 30-40% of the total delivered cost of salt.

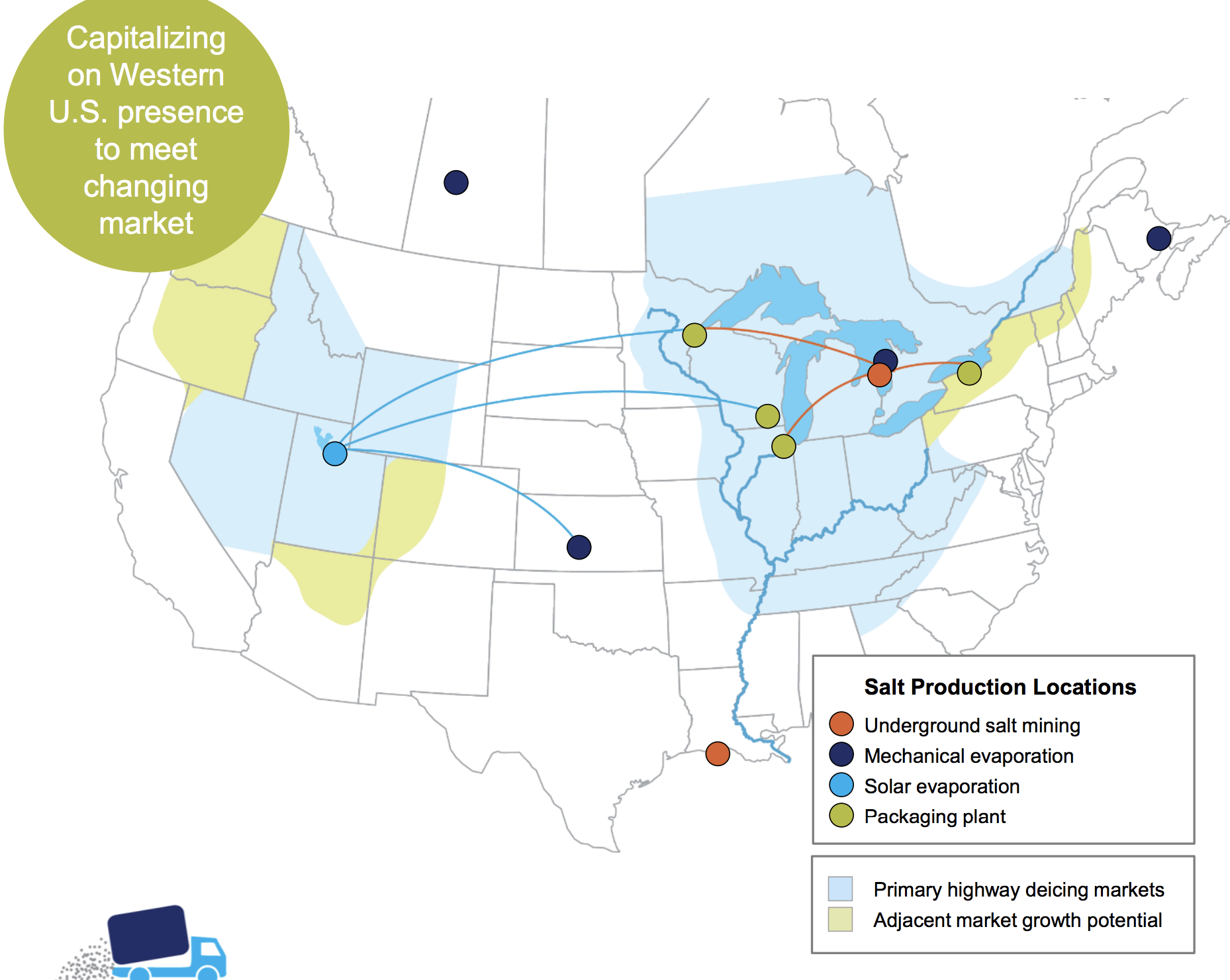

Compass Minerals is the lowest cost producer for the Midwest area because it owns the largest and highest-quality grade rock salt mine in the world in Ontario, Canada, and has a network of 90 supply depots along navigable waterways to reach customers affordably and quickly (its Goderich mine is located right next to Lake Huron and Cote Blanche is near the Mississippi River, which connects to the Ohio River).

Water transportation is about half the cost of rail and one-third the cost of trucking, meaning that Compass Minerals' operations are very cost efficient. The company’s presence in the Midwest also protects it against import competition, which is only somewhat effective on the East and West coasts of the U.S.

Source: Compass Minerals Investor Presentation

Rock salt must also be near customers before winter starts; they can only store so much salt at a time and might need to order some for quick delivery in the event of a severe winter storm. Compass Minerals' network can get salt to customers quickly by rail, truck, barge, or vessel.

Competitors in the market lack Compass Minerals' economies of scale (their mines can’t produce as much salt and have higher costs) and waterway network advantages. Compass Minerals' asset network allows the company to execute a very competitive bidding strategy that significantly protects its market share thanks to its greater efficiencies.

Outside of salt, Compass Minerals' sulfate of potash (SOP) business is also unique. Compass Minerals' solar evaporation pond complex in Utah is one of only four in the world (and the only one in North America) that can produce SOP from a naturally occurring brine source using solar evaporation. This production method has the lowest cost profile in the world.

With limited pond-based feedstocks available in the country due to geological constraints, especially in cost-effective locations for transportation purposes, barriers to entry are extremely high in Compass Minerals' regional markets. SOP’s limited availability contributes to it accounting for less than 10% of all potash consumption.

SOP is also primarily used on high-value or chloride-sensitive crops such as citrus fruits, grapes, almonds, and tobacco. Unlike major global crops such as corn, many of these “specialty” crops have demonstrated more stable economics. It’s also worth mentioning that Compass Minerals' SOP is approved for organic food production, which should only see increased demand over the coming years.

While Compass Minerals' SOP business will be sensitive to broader trends in agricultural markets (most notably farmer's income), its barriers to entry, high value provided to growers of specialty crops, and solid pricing power make the business much less volatile and more profitable than traditional potash fertilizer (which, unlike SOP, includes chloride).

Compass Minerals' former CEO Fran Malecha joined the company in 2013 and made a big push to diversify the business even further into the agriculture industry. From 2000 to 2013, Malecha worked at Viterra, a global agribusiness company based in Canada where he served as chief operating officer of the global grain business.

Given his background, it's not a big surprise Malecha decided to double down on similar businesses at Compass Minerals to drive growth. The push to expand more into the agriculture business is also intended to smooth out the company's salt-driven earnings, which are sensitive to winter weather conditions.

In October 2016, Compass Minerals significantly expanded its plant nutrition business with the acquisition of Produquímica, a company operating two businesses in Brazil – agricultural productivity, which manufactures a range of specialty plant nutrition products, and chemical solutions, which manufactures specialty chemicals, primarily for the water treatment industry. The company also bought Wolf Trax, a premium micronutrients supplier, that same year.

These deals significantly shifted Compass Minerals' overall revenue mix, reducing its dependence on salt (and winter weather variability).

Source: 2018 10-K

Similar to the company's SOP business, Produquímica focuses on selling higher margin, differentiated products. Brazil's soil profile is also weaker than North America's so the need for specialty minerals and fertilizers to boost crop yields is higher. As Brazil's economy continues developing, farmers should increasingly use more specialty fertilizers, and Produquímica's products can also be exported around the rest of the world over time.

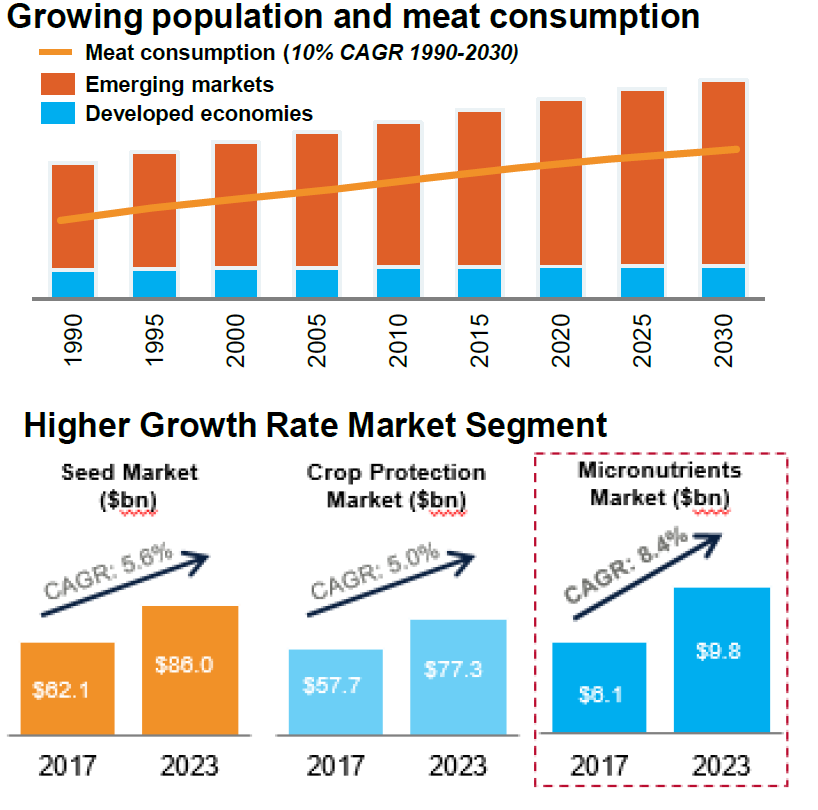

Both of the company's agriculture businesses are also expected to benefit from several secular themes. A growing global population creates demand for more food, and arable land (i.e. land suitable for growing crops) per person is expected to decline. As a result, significant improvement in crop yields will be needed to support higher crop production, bolstering demand for Compass Minerals' specialty fertilizers and plant nutrients.

At the end of 2018, the plant nutrition market was estimated at $10 billion per year, and that is likely to only grow over time. For context, Compass generated less than $1.5 billion in total revenue in 2019, showing just how large of a potential growth runway plant nutrition represents for the company.

Source: Compass Minerals Investor Presentation

Besides acquisitions, the company also completed a $500 million investment program in its key assets to improve the efficiency of its North American businesses and boost SOP production capability, which further increases its exposure to the agribusiness.

Over the long-term Compass believes it can achieve 10% annual revenue growth from its plant nutrition business and 25% EBITDA margins, which should slightly increase the company's overall operating margin.

On the salt side, Compass Minerals has completed a $225 million investment program to install continuous mining and haulage equipment. Management expects these investments to reduce the company's mining costs by approximately $30 million annually (25%) beginning in 2019 and improve the safety profile of its largest mine, which suffered a ceiling collapse in 2017 that resulted in severe business disruption for over a year.

In 2018 a strike (30% of its global workforce is unionized), the Goderich roof collapse, and a slower than expected ramp-up of its continuous mining system further hurt volumes, increased unit costs, and resulted in significant decreases in profitability. Fortunately, those issues appear to have been resolved by the end of 2018, and management expects higher salt volumes in 2019.

While Compass Minerals' assortment of hard-to-replicate assets, low production costs, and long-term growth potential are intriguing, the company faces a handful of meaningful risks.

Key Risks Over the short term, Compass Minerals' business is under quite a bit of pressure. Management's aggressive investment plans and large acquisition of Produquímica stretched the company's balance sheet at an inopportune moment.

Mild winter weather, soft agricultural markets, unfavorable foreign currency exchange rates (26% of revenue is derived in Brazil), and operational challenges (e.g. temporary mine closure) have hurt the company's results in recent years and have potential to create future headwinds.

While Compass Minerals' expansion into global plant nutrition markets reduced the company's exposure to winter weather, this diversification effort also increased the firm's sensitivity to other factors, like global agricultural and specialty potash prices.

Source: Compass Minerals Investor Presentation

Uncontrollable macro factors can have big impacts on the company's profitability, due to Compass' high fixed costs and the capital intensive nature of this industry. For example, back-to-back mild winters in 2016 and 2017 hurt the salt business, and a multiyear downcycle in agricultural markets caused Compass Minerals' adjusted earnings per share to fall from $4.69 in 2015 to $1.77 in 2018.

As a result, the company's payout ratio spiked above 100% and remains at elevated levels, leading management to freeze the dividend.

Source: Simply Safe Dividends

Making matters worse, Compass Minerals' leverage has remained dangerously high following its acquisition of Produquímica in 2016. Thanks to unfavorable macro conditions, various operational setbacks, and substantial growth spending, since 2015 Compass Minerals has failed to generate enough free cash flow to cover its dividend, much less reduce its leverage.

Source: Simply Safe Dividends

Due to its elevated leverage profile and lack of substantial positive free cash flow, both Moody's and Standard & Poor's have assigned the company a junk bond credit rating. Moody's even lowered its rating a notch in April 2019, citing "continued elevated leverage and our expectations for limited debt reduction over the rating horizon."

Compass is finally bringing several of its major growth projects online, which increased operating cash flow by 30% in 2018, but its free cash flow still did not cover the dividend (a free cash flow payout ratio of 104%). Moody's also projects modestly negative free cash flow in 2019 and 2020 after paying dividends, assuming normal winters.

As a result, the company's ability to finance future growth and deleverage to safe debt levels is very challenging. When a business pays out more in dividends than it generates in free cash flow, the shortfall must be paid for with cash from its balance sheet ($44 million), selling new shares (which raises future dividend costs), or taking on debt.

None of these options is a good long-term strategy for a capital intensive and cyclical company that sells commodity products and is largely at the mercy of the weather or global agricultural markets.

Cyclical companies can endure a free cash flow payout ratio well over 100% for a period of time if they are prepared. In fact, Compass Minerals' free cash flow payout ratio exceeded 100% in both 2009 and 2012. However, in the past the company's balance sheet was much stronger before its push into South American agricultural nutrients.

While management has started to reduce its net leverage ratio in recent years, a trend that's expected to continue, the company's ambitious and ill-timed acquisitions of plant nutrition businesses have elevated its risk profile and put it on the brink of violating the credit agreement governing its $300 million credit facility.

Specifically, as Compass Minerals noted in its 2018 10-K, if its "leverage ratio exceeds 4.5x, we would be in default under our credit agreement." The firm's leverage ratio, as calculated under the terms of its credit agreement, stood at 4.3x at the end of 2018. Should a violation occur, then Compass Minerals' creditors could force it to reduce or suspend its dividend.

Compass Minerals currently has $1.3 billion in debt, with about $1.1 billion maturing from 2019 through 2021. As a junk bond-rated company, the firm is at higher risk of tightening credit conditions, which could increase its interest expense or make future borrowing difficult, especially if a recession occurs.

The company's dividend costs $100 million per year, which doesn't sound like much, but that's nearly double its 2018 interest costs of $63 million (bond interest always comes first before dividends).

If the U.S. suffers a recession in the next couple of years, then Compass's still debt-heavy balance sheet could come under pressure and lead management to cut or even eliminate the dividend to secure the company's financial future.

Speaking of management, that has also been a source of drama in recent months. In November 2018 Malecha stepped down as CEO and Richard Grant, who has served on Compass's board for 15 years, became interim CEO.

In May 2019 Kevin Crutchfield became the new permanent CEO. Crutchfield has over 30 years of mining experience, though mostly in the coal industry (he was CEO of two coal companies for the past decade).

The risk is that Compass' new CEO might take the company in a new direction, given how disappointing its ambitious push into agricultural products has been. He might also view the firm's $100 million annual dividend cost as an easy source of cash should Compass run into continued executional challenges that crimp cash flow, or face tighter credit conditions during a recession.

Changes in capital allocation plans are unusual, but the odds are higher following management changes, especially at struggling businesses. Only time will tell. For now, on the firm's May 1, 2019, earnings call Compass Minerals' CFO Jamie Standen said that the team continues to view the "dividend as manageable" and remains "confident that we will continue expanding our free cash flow generation."

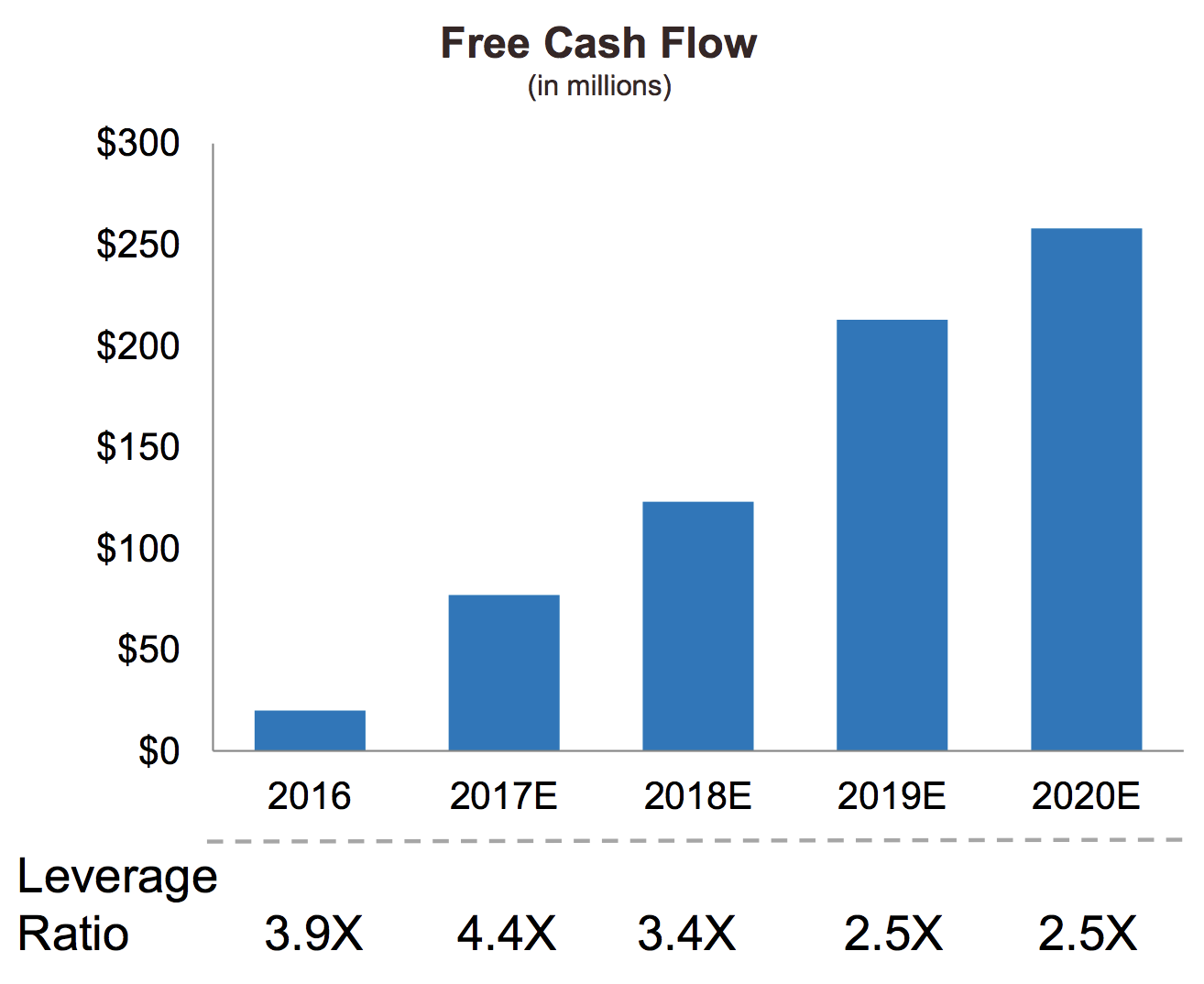

Fortunately, management is guiding for modest annual capex spending of about $100 million going forward now that it's completed most of its investments. That should result in free cash flow eventually rising to $150 million to $200 million per year, representing a 50% to 67% payout ratio. The company also sees leverage falling by a significant amount this year.

Source: Compass Minerals Investor Presentation

If management is able to deliver on its guidance, which can change quickly for a cyclical, commodity-sensitive business), and the economy avoids a recession in the coming years that could pressure the company's refinancing ability, then Compass's dividend may be sustainable.

However, it's important to remember that guidance isn't a promise, only the current forecast based on the best available market data. For example, here's management's free cash flow and leverage guidance from early 2018.

Source: Compass Investor Presentation (2018)

As you can see, despite the company's "success" in achieving cost-cutting and capacity expansion, free cash flow by 2020 was supposed to be $250 million, or $50 million to $100 million higher than the current forecast. Meanwhile, leverage was supposed to decline to management's long-term target of 2.5 by the end of 2019, which is 1.2x less than the current forecast.

Until the company makes more significant progress paying down debt and generating free cash flow after dividends, Compass Minerals' dividend will continue to look speculative. A change in leadership at the top adds to the uncertainty, and the company's cash flow will always remain volatile due to its exposure to factors beyond management's control.

For these reasons, Compass Minerals does not appear to be an appealing dividend stock for conservative income investors.

Closing Thoughts on Compass Minerals Compass Minerals was a reliable dividend growth stock for over a decade and has an even more impressive operating history dating back nearly two centuries. The company's businesses are relatively simple to understand and very durable thanks to their unique assets, which are practically impossible to replicate in many cases.

However, a prolonged stretch of unfavorable macro and operating conditions, combined with previous management's aggressive investments, stretched the balance sheet and have increased Compass Minerals' risk over the short term.

While the firm's CFO seems committed to maintaining the existing dividend until the company's cash flow improves, new leadership at the top could place greater priority on accelerating deleveraging efforts. Either way, conservative investors may be better off waiting on the sidelines until Compass Minerals is in better financial shape and has more breathing room.

After all, while the company's big diversification push into plant nutrition expanded its long-term growth opportunities, it also means that Compass now plans to maintain debt and payout ratios far higher than it has in the past. The company's deleveraging efforts require the economy and various commodity markets to remain at favorable levels in order to be achieved, too.

With a new CEO leading the company, there is especially a lot of uncertainty about how safe Compass Minerals' dividend would be in an economic downturn, when crop prices would likely decline and credit markets could tighten.