Founded in 1917, Parker-Hannifin (PH) is a global industrial conglomerate specializing in motion control systems, specifically electromechanical, hydraulics, and pneumatic components such as valves, pumps, filters, and motors. The company's products serve over 430,000 global customers in every significant manufacturing, transportation, and processing industry.Parker-Hannifin has two main operating units that serve virtually every significant manufacturing, transportation, and process industry: diversified industrials and aerospace systems.

Diversified Industrials (81% of sales, 79% of operating profit in 2017): this segment manufactures and sells a wide range of motion-control and fluid systems and components across Parker-Hannifin’s automation, engineered materials, filtration, fluid connectors, hydraulics, and instrumentation company groups.

Aerospace Systems (19% of sales, 21% of operating profit in 2017): these products are used on commercial and military airframe and engine programs.

Thanks to its $4.3 billion acquisition of filter manufacturer Clarcor in 2017, about 54% of Parker-Hannifin's industrial sales come from higher-margin aftermarket business. This is where Parker partners with more than 13,200 global distributors to earn recurring revenues via replacement parts and long-term maintenance contracts.

In recent years, Parker has successfully differentiated itself from being merely a supplier of quality industrial components, moving up the value chain by creating a strong systems-focused business. Specifically, the company integrates its components for customers based on their individual needs and helps them to maximize their returns on investment. About 25% of sales now come from Parker-Hannifin’s systems division, which should result in less volatile sales and cash flow going forward.

The company is also highly diversified with no single product representing more than 1% of revenue and no customer account for more than 3% of sales. Approximately 60% of sales are derived from the U.S. with the remaining 40% from other international countries.

With 61 consecutive years of dividend growth to its name, Parker-Hannifin is a dividend king.

Business Analysis

As an industrial conglomerate, one that services many cyclical end markets such as the oil & gas industry, Parker-Hannifin’s sales can be highly volatile from year to year.

However, the company also has several competitive advantages that have allowed it to achieve far more stable earnings, free cash flow, and returns on capital than its cyclical revenue would imply. This has allowed Parker-Hannifin to deliver 61 consecutive years of dividend growth through all manner of economic, industry, and interest rate environments.

The company's first major competitive advantage is its long operating history, which has allowed the firm to build relationships with some customers that span decades. Parker-Hannifin produces mission-critical components for its customers and, in many cases, specifically designs individual parts and integrated systems tailored to a client's specific needs. The company then installs its products in a customer's factory and provides ongoing replacement parts and maintenance as well.

In most cases, the parts Parker-Hannifin sells to its clients represent about 5% of their total costs. And since Parker-Hannifin has spent decades improving the durability, reliability, and profitability of its products (lower long-term operating costs), it enjoys a wide moat and strong pricing power.

That's because a customer wanting to switch suppliers would need to first work out their exact needs (tailor-made systems and parts), and then endure costly delays in retooling their manufacturing facilities. And if the new parts ended up not meeting quality standards, then they might fail and put its customers at high legal liability (say if a jet engine fails because of a faulty part).

Parker-Hannifin also has the broadest technology platform in the market, allowing it to help customers create more systems and subsystems than any of its competitors. While most competition competes on one or two technologies, about 60% of Parker-Hannifin’s customers buy from four or more of its operating groups, indicating strong cross-selling power and a wide moat.

Most of these technologies have patents or trade secrets protecting them and focus on extremely important parts of the products they go into. By focusing on high-margin niches and offering a greater breadth of protected technologies, Parker-Hannifin is able to maintain solid profitability.

Parker-Hannifin’s aftermarket business, which accounts for a little over half of its sales and an even greater share of profits, is very important for the company’s strong margins and long-term outlook.

While Parker-Hannifin’s top and bottom lines are somewhat cyclical, the company’s meaningful maintenance, repair, and overhaul (MRO) business provides a source of stability and entrenchment with customers.

Unlike OEM parts, aftermarket parts and services are necessities when equipment wears down, making the MRO business less cyclical. Parker-Hannifin’s strong market share in this business is reinforced by its world-spanning distribution network, which boasts over 13,200 locations around the world and is larger than any of its competitors’ networks.

When equipment breaks down, it needs to be serviced immediately. Customers would prefer to work with a company like Parker-Hannifin that has a distribution network in close proximity that can quickly get the machinery back up and running.

Parker-Hannifin’s distribution network has been in development for more than 50 years and would take competitors decades of time and substantial financial costs to replicate.

Maintaining a global network that covers numerous technologies and geographies also helps Parker-Hannifin win business with large multinational customers, which need to be reliably serviced around the world.

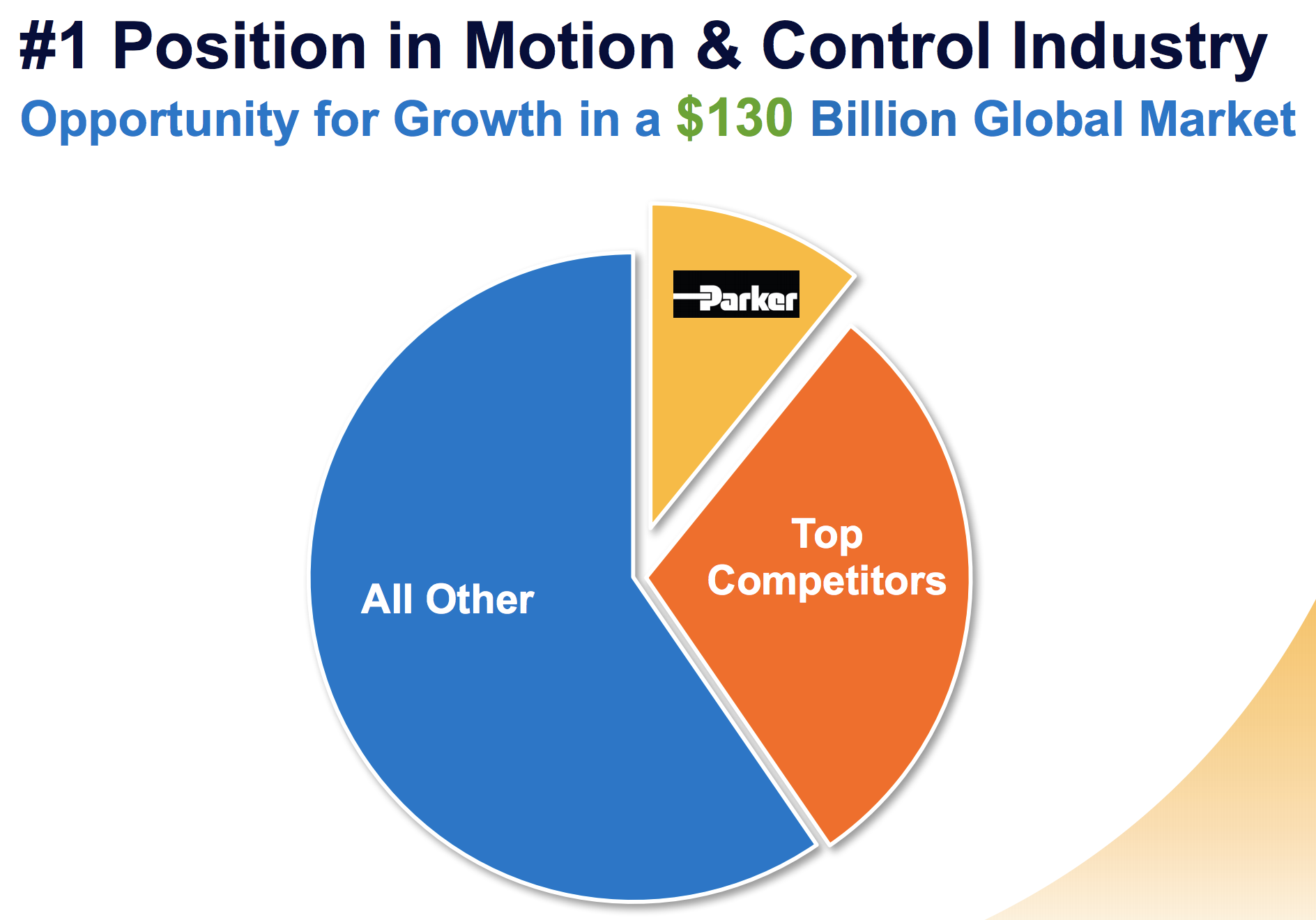

This strong distribution network has allowed Parker-Hannifin to gain about 10% market share and become the industry leader in its niche. That might not sound like a lot, but in the $130 billion motion control market that the company operates in, there are literally thousands of rivals fighting for market share.

Source: Parker-Hannifin Investor Presentation

Few of these competitors have the resources to recreate or beat Parker-Hannifin's distribution network. Nor can they achieve the same economies of scale that include sourcing raw materials from the lowest cost areas and optimizing its manufacturing and distribution facilities.

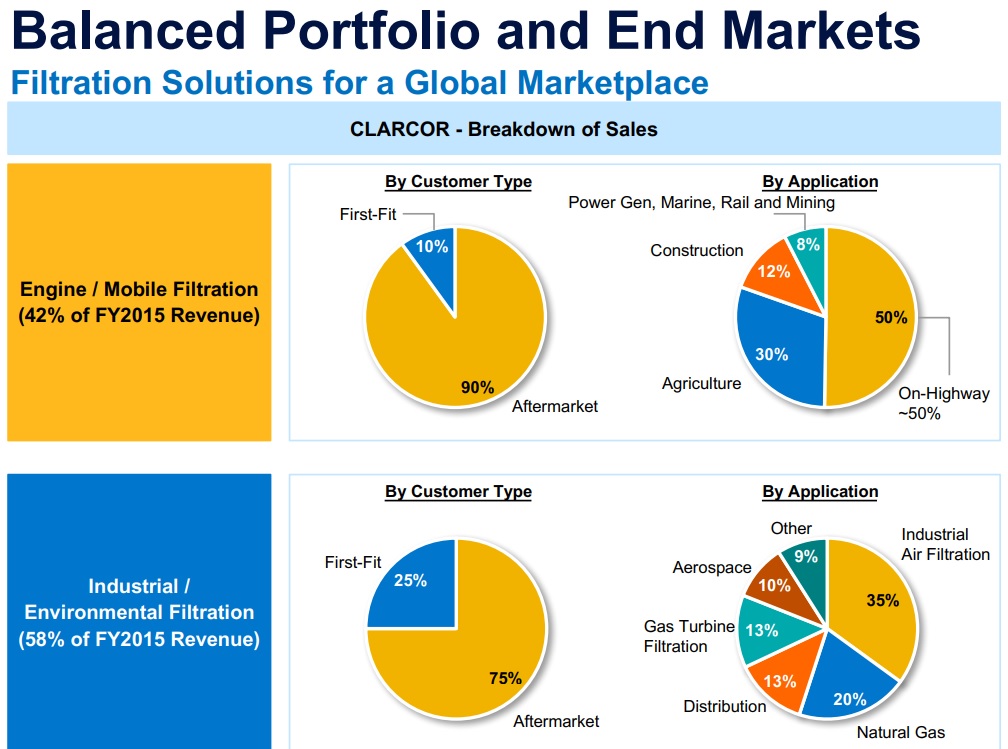

Finally, Parker is very good at acquisitions, which are very frequent in this highly fragmented industry. Remember that successful industrial companies usually have strong customer relationships with high switching costs, so often the fastest way to gain market share is to acquire a smaller rival. Parker-Hannifin spent $4.5 billion in 2017 on three acquisitions, the largest of which was filter maker Clarcor.

Clarcor is a great example of the kinds of companies that Parker-Hannifn goes after. Clarcor's specialized filters are fast consumables, meaning clients need to replace them frequently. As a result, the vast majority of Clarcor's business is in the aftermarket, resulting in high margins and substantial recurring revenues.

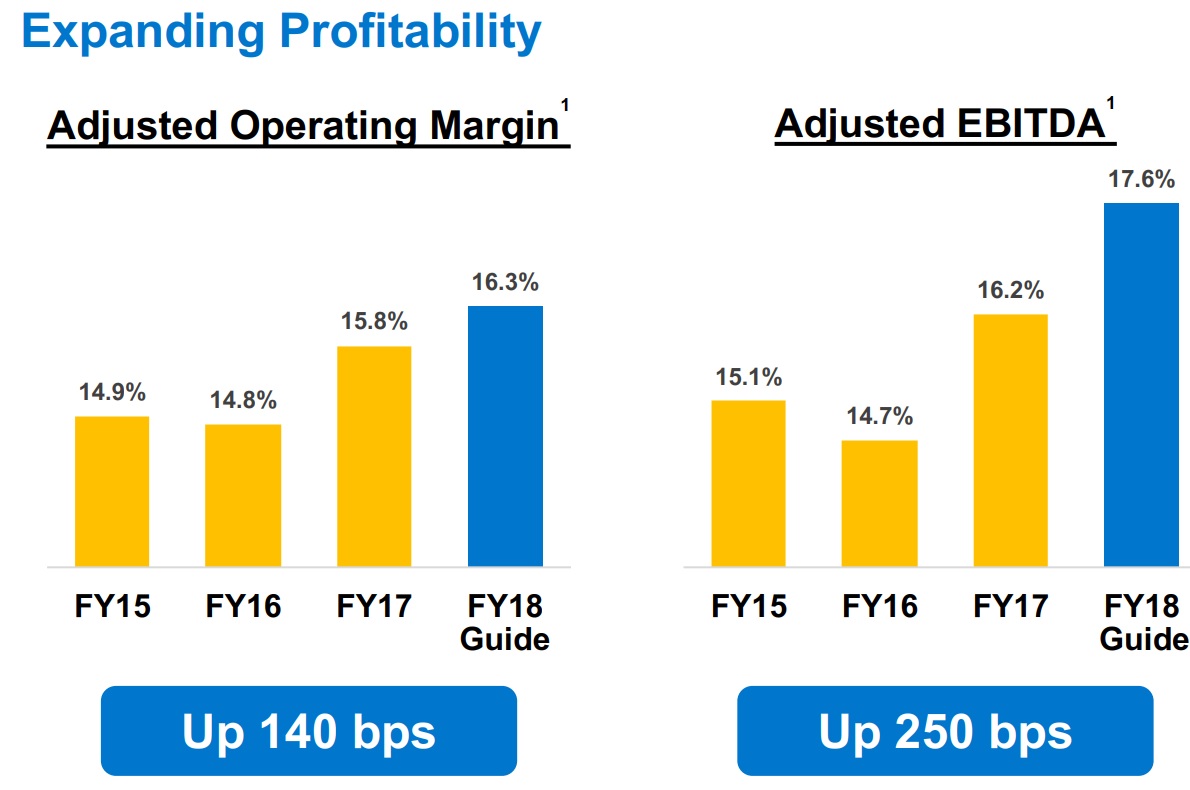

Prior to being acquired, Clarcor's 18.3% EBITDA margin was actually much higher than Parker-Hannifin's (14.7%). In other words, after the Clarcor acquisition, Parker-Hannifin is even better positioned to enjoy higher profitability and more consistent sales, earnings, and cash flow.

The combined businesses are also more diversified and benefit from having just over 50% of their total sales from aftermarket applications, providing nice stability compared to OEM sales.

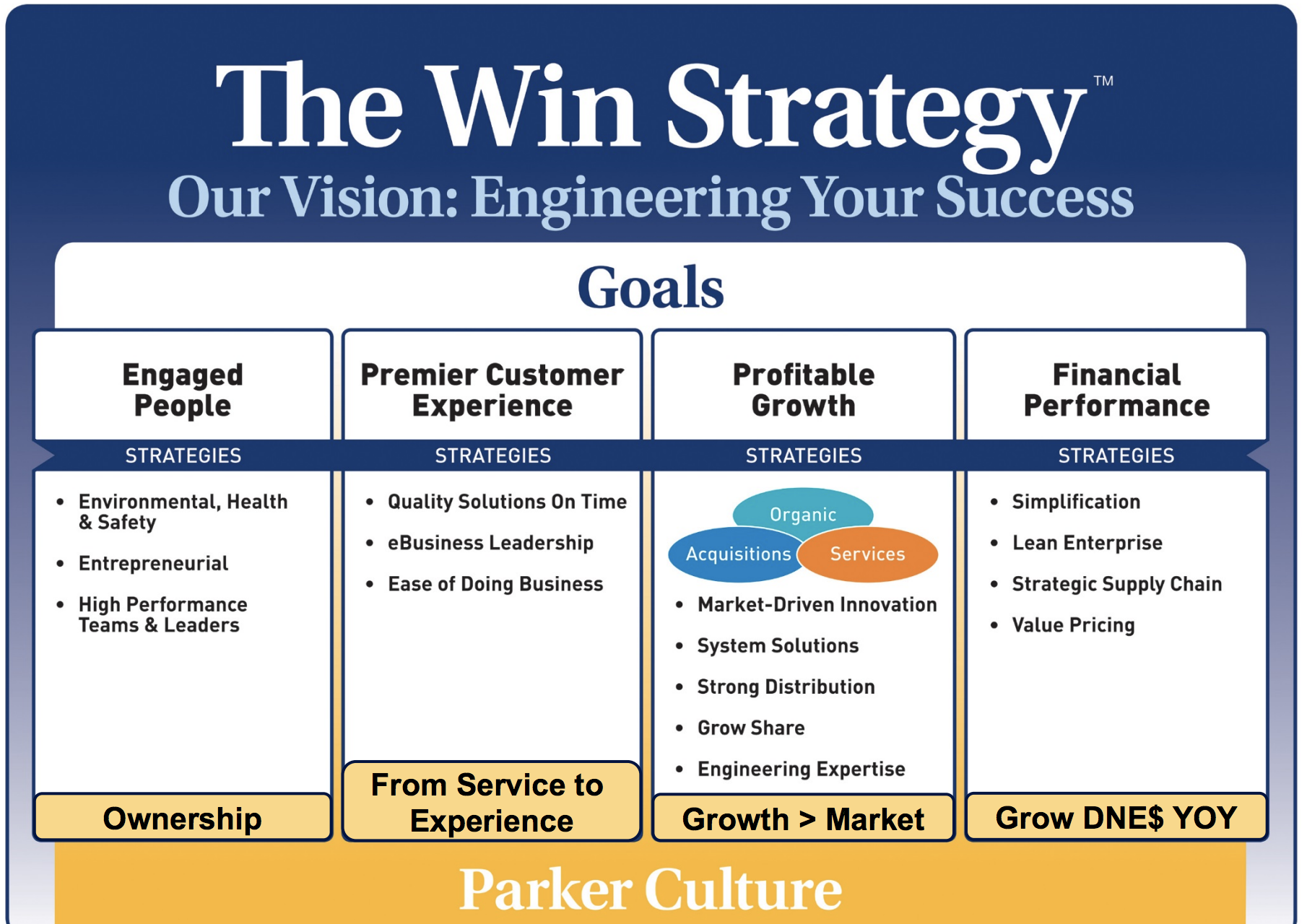

In addition, Parker-Hannifin now believes that it will be able to achieve $160 million in synergistic cost savings from the Clarcor purchase by 2020, up from $140 million originally. All told, Parker now expects Clarcor's EBITDA margins to increase about 300 basis points to reach close to 21% by 2020. In other words, the Clarcor integration is proceeding better than expected. That's largely thanks to Parker's operating culture which it calls its WIN strategy.

Source: Parker-Hannifin Investor Presentation

A large part of Parker-Hannifin’s success is driven by its culture of lean manufacturing, which really began in the early 2000s. The company’s efforts to improve profitability, generate more cash, free up working capital, improve product quality, and raise on-time delivery rates have reinforced the company’s global positioning as a powerhouse.

The goal of WIN is to continuously improve the company's supply, distribution, and manufacturing supply chains, just like it has over the years.

Efficiency: 52% reduction in per unit energy usage in last 10 years

Increasing safety: 54% decrease in industrial accidents since 2014

Going forward, the company’s lean expertise will help it gain greater revenue efficiencies (use fewer part numbers, reduce overhead cost, use more e-commerce, pricing strategies, etc.), consolidate divisions, and more. Even if end markets unexpectedly weaken, Parker-Hannifin can be relied upon to continue improving its competitive position and margin profile in anticipation of better times ahead.

WIN also includes optimizing the company's product mix. This means selling off underperforming (slower growing, lower margin) commoditized product lines and focusing exclusively on areas where Parker is strongest. WIN is very customer-focused as well with management being tracked on how quickly and effectively it can resolve any problems its customers report (reliability issues).

In recent years, Parker-Hannifin has turned its R&D budget ($317 million in 2017, or about 2% of sales) towards offering its customers more integrated systems to meet their industrial needs. Most of these systems have very long product life cycles meaning that Parker-Hannifin is able to very efficiently monetize its development costs over many years without making very frequent changes to the products it sells to individual customers.

Many of these industrial products connect to the internet (so-called Internet of Things), which allows them to monitor their usage of Parker-Hannifin's products and systems in real time. This in turn allows more efficient maintenance and repairs that decrease downtime and boost overall productivity and profitability. Combined with the tailor-made nature of many of these systems for each individual customer, this further increases Parker-Hannifin's moat and raises its customers' switching costs.

Going forward, management's expansion plan is a combination of organic growth in current business lines as well as ongoing strategic acquisitions of companies that fit well into its existing supply and manufacturing system. Major purchases are expected to come once the company finishes deleveraging from its acquisition of Clarcor.

A key determinant for Parker-Hannifin on whether or not to acquire a company is how stable a firm's sales are (recurring revenue versus one-time sales), and how fast the company is growing organically. Management will likely remain focused on smaller but faster-growing niche players like Clarcor which enjoy larger amounts of recurring revenue and higher margins.

Margins are a big focus for Parker since the industrial sector usually grows at the same rate as the global economy. This means achieving strong earnings and dividend growth requires controlling costs and maximizing profitability (margins). The company's lean manufacturing culture should help it continually reduce per unit costs, an approach that has served it well in past years.

Source: Parker-Hannifin Investor Presentation

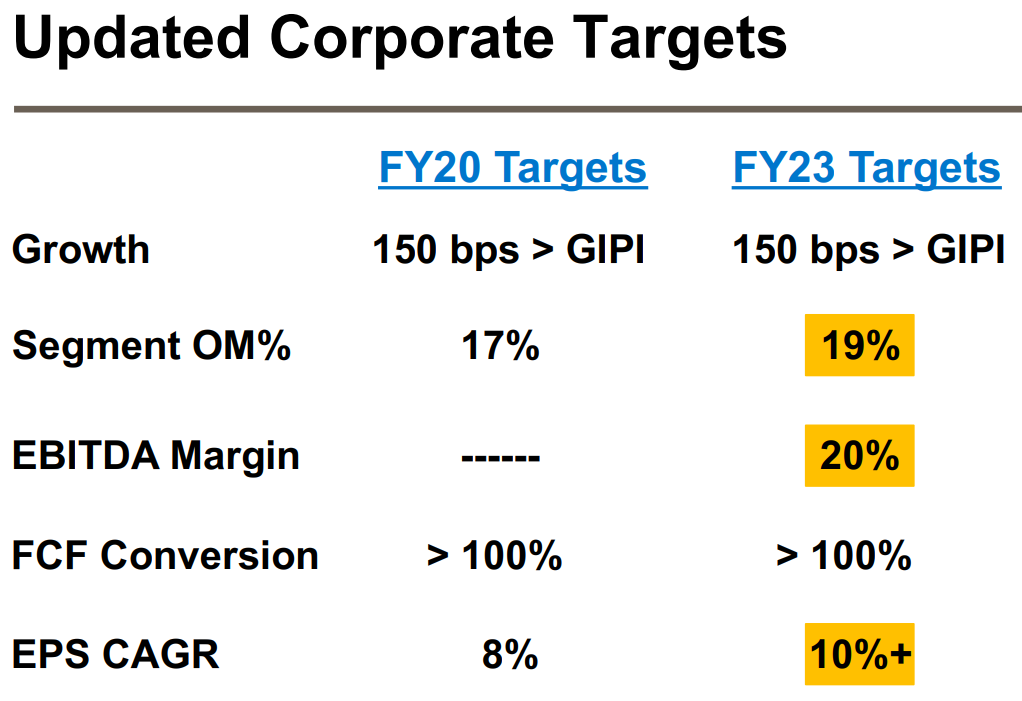

Thanks to improving cost management, management believes the company can raise its operating margin to about 17% by 2020 and 19% by 2023, representing a substantial increase in profitability compared to prior years.

Over the long term, management believes it can grow Parker-Hannifin's EPS by about 8% to 10% annually, with free cash flow per share growing slightly faster. Combined with its low payout ratio, that should allow the company to grow its dividend at roughly the same pace (9% to 10% annually).

That's roughly in line with its 20-year average annual dividend growth rate of 11% and is among the fastest potential payout growth rates of any dividend king. In other words, Parker-Hannifin seems likely to be a solid long-term income growth investment.

Source: Parker-Hannifin Investor Presentation

Key Risks

Despite its high aftermarket mix, Parker-Hannifin's business will still face volatility in revenue during economic and industry-specific downturns such as the oil crash of 2014 to 2016.

The business is most sensitive to manufacturing activity, aircraft miles flown, and construction markets. Not surprisingly, Parker-Hannifin will be impacted by trends in the broader economy and is cyclical.

In addition, margins can be negatively impacted at times by the volatile nature of its raw material which include: steel, brass, copper, aluminum, nickel, rubber, plastics, and various chemicals. U.S. tariffs have caused prices to spike for a number of these materials, including steel and aluminum.

While Parker-Hannifin sources its inputs from around the world, rising raw materials can still put the squeeze on margins and make it harder to hit management's ambitious margin and EPS growth targets.

Escalating trade hostilities between the U.S., EU, Canada, and China mean that Parker's well honed supply chain could also be at risk of disruption. While management can adapt over time, in the short to medium-term this could impair the firm's earnings and dividend growth potential.

With about 40% of sales coming from overseas, Parker-Hannifin also faces some currency exchange rate risk. If the U.S. dollar appreciates against local currencies, then Parker-Hannifin's sales in foreign markets translate into less U.S. dollars, creating a growth headwind that could cause it to miss its long-term targets.

Finally, investors must not forget Parker-Hannifin's heavy focus on acquisitions. While the company has a good track record on M&A, every deal comes with execution risk. That involves both potentially overpaying for a purchase (Clarcor was bought at a rich 17 times EBITDA multiple), and potentially failing to achieve expected cost synergies.

Overall, it's hard to identify a risk factor that could impair Parker-Hannifin's long-term earnings power. With hundreds of thousands of individual products and over 400,000 customers, Parker-Hannifin operates a well-diversified business model that won’t be brought down easily by any single factor. The company’s sturdy balance sheet (including an A credit rating from Standard & Poor's) and free cash flow generation add further protection.

Closing Thoughts on Parker-Hannifin

Parker-Hannifin is a perfect example of a boring but beautiful dividend growth stock. The company's strong relationships with its customers, globe-spanning distribution network, ever-more specialized products, and high mix of aftermarket revenue create a wide moat for this industry leader.

And thanks to management's strong track record of good capital allocation, including well-executed acquisitions, Parker-Hannifin has managed to generate one of America's most impressive long-term dividend growth records.

Going forward, the company's focus on more advanced technology systems, more aftermarket products (greater recurring revenues), and higher-margin business lines should help it continue driving double-digit growth in cash flow and dividends. As a result, Parker-Hannifin appears to be a potentially solid long-term investment with one of the fastest income growth rates of any dividend king.