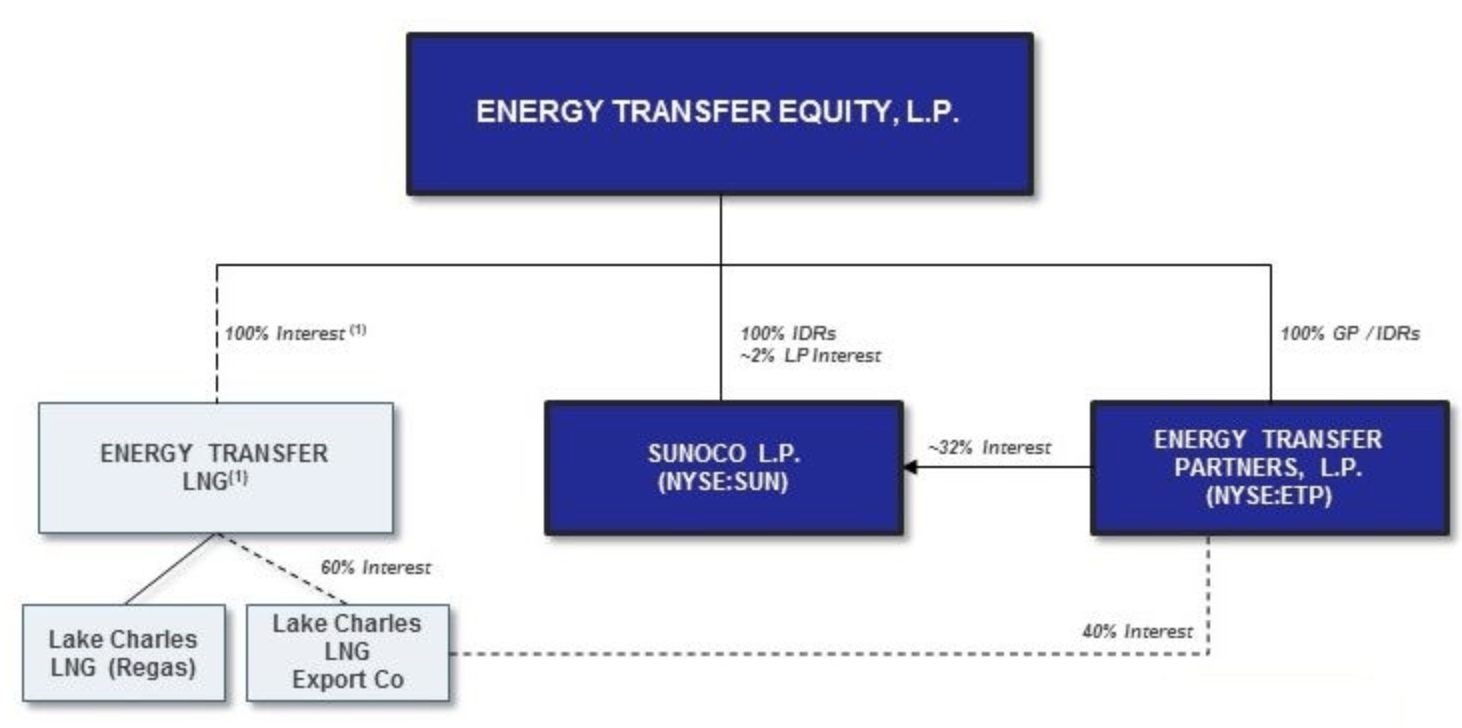

Founded in 1995, Energy Transfer Partners (ETP) is one of America's largest midstream master limited partnerships, or MLPs. The company is part of the larger Energy Transfer family of companies and MLPs, which is overseen by founder and CEO Kelcy Warren. Warren owns 17% of Energy Transfer Equity (ETE), the sponsor and general partner of Energy Transfer Partners.

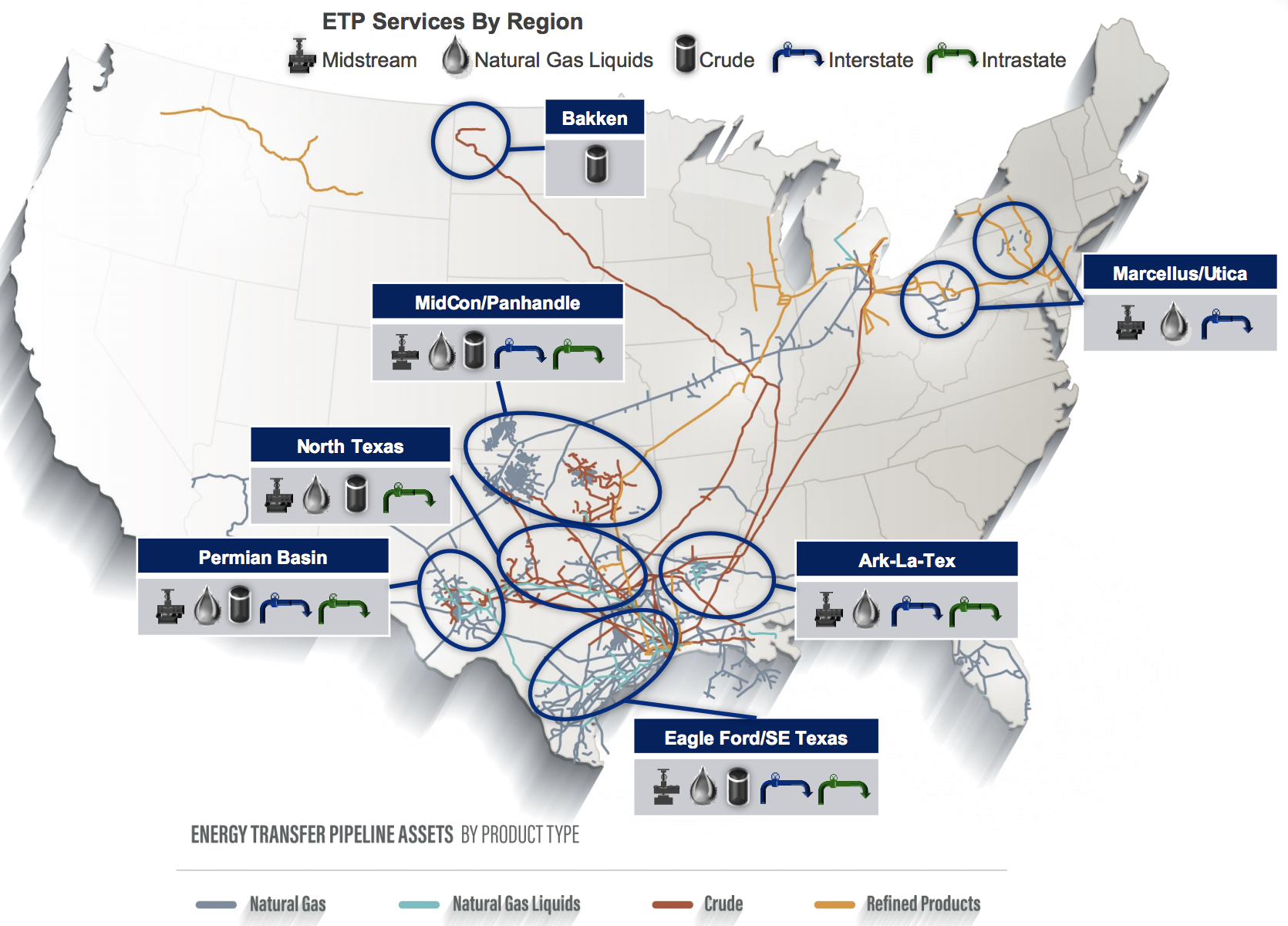

Energy Transfer Partners serves nine of America's largest 10 shale oil & gas formations via its large and vertically integrated network consisting of:

Over 30,000 miles of natural gas, natural gas liquids (NGLs), refined products, and crude oil pipelines

11.5 billion cubic feet per day of gas gathering capacity

15 billion cubic feet per day of gas transportation capacity

3.8 million barrels per day of oil transportation capacity

455,000 barrels per day of NGL fractionation capacity

7.9 billion gallons of fuel sales (Sunoco stake)

40% stake in Lake Charles LNG export terminal which has an export capacity of 1.8 billion cubic feet per day.

Source: Energy Transfer Partners Investor Presentation

The partnership's most valuable asset is its Texas intrastate gas network, which is the largest and most comprehensive of any MLP in the country. Texas is America's largest gas supplier, and Energy Transfer Partners has a near monopoly on gas transmission throughout the state.

Business Analysis

Midstream MLPs tend to have impressive durability, driven largely by two factors. First, pipelines, storage facilities, terminals, and other transportation infrastructure can cost billions of dollars to construct, making it hard for smaller companies to enter the space.

In addition, midstream MLPs are highly regulated at state, local, and federal levels. As a result, it can take several years just to obtain the required permits to embark on a new project. Interstate pipelines are under the purview of the Federal Energy Regulatory Commission, or FERC.

FERC generally won't approve a new pipeline unless there is strong need from energy producers. One of FERC's most important jobs is to ensure that companies charge “just and reasonable” fees and that exploration and production companies have fair access to transport products. Rates are usually set on a cost-of-service basis, factoring in capital and maintenance costs to keep the infrastructure running.

In this way, the midstream industry is similar to regulated utilities, in which an MLP is entitled to earn a reasonable but not lavish return on capital in exchange for providing a reliable, mission-critical service.

The cash flow derived from midstream assets is usually highly stable, as oil & gas producers like to lock in long-term contracts, sometimes for as long as 25 years. In addition, many contracts are "take or pay" in nature, meaning that customers are reserving volume capacity and paying the MLP whether or not they actually ship any product.

In other words, many midstream MLPs can be thought of as tollbooth operators, with highly stable, fixed-fee cash flow from which to pay their distributions.

However, not all MLPs are created equal. Like all industries, there is a lot of complexity related to how safe and dependable an MLP's distributable cash flow, or DCF (similar to free cash flow for an MLP), really is.

Energy Transfer Partners may be one of America's largest and most vertically integrated MLPs, but it's also one of the most troubled. Since 2008, the MLP has grown and diversified away from its highly profitable legacy Texas intrastate gas network.

This network was arguably the most advantaged and attractive asset the MLP owned, with virtually no competition, a very friendly state regulatory body, and strong pricing power. Energy Transfer Partners could frequently raise its tariffs on that pipeline network and grow its cash flow while having to spend very little on maintenance.

To take full advantage of America's shale & gas boom, the MLP began investing heavily into new assets, including oil pipelines to supply the thriving Bakken (North Dakota), Eagle Ford (East Texas), and Permian basins (West Texas). The company also began investing heavily into infrastructure for natural gas liquids, which are a byproduct of gas production and serve as important feedstocks for the petrochemical industry.

However, management made the mistake that many MLPs did during the boom times, when oil prices were above $100 per barrel. Rather than grow the distribution slowly and maintain strong distribution coverage (DCF/distribution) ratios, MLPs like Energy Transfer Partners grew their payouts very quickly. They essentially retained no cash flow to fund growth projects and relied almost exclusively on tapping debt and equity markets to raise capital.

When oil prices plunged over 70% between mid-2014 and January 2016, credit and equity markets slammed shut for most MLPs that had taken on dangerous amounts of debt.

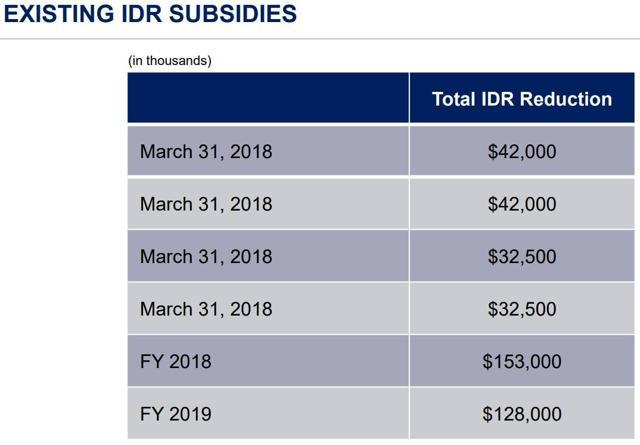

Energy Transfer Partners was one of those MLPs, and its leverage ratio (debt/adjusted EBITDA) peaked at over 9 in 2016. In order to help its struggling MLP, Energy Transfer Equity (ETE), who provides the management and owns the incentive distributions rights (IDRs), announced it would be waiving nearly $1 billion in IDR fees that Energy Transfer Partners was scheduled to pay.

Source: Energy Transfer Partners Investor Presentation

About $656 million of those IDR waivers came in 2017, and the cash ETP saved was able to be invested in the MLP's massive backlog of growth projects. Completing these projects helped raise the troubled MLP's distribution coverage from dangerously low levels (sub 1) to 1.2 for 2017.

However, excluding the IDR waivers, which are decreasing rapidly and will go away entirely beyond 2019, the coverage ratio was just 1.01.

In the MLP industry, a coverage ratio of 1.1 or above often signals a sustainable distribution with some capability of long-term growth. Fortunately, Energy Transfer Partners' ex-IDR waiver ratio rose to 1.09 in Q4 2017, indicating that the current payout is reasonably well covered by cash flow.

Between mid-2017 and mid-2019, management plans to put into service $10 billion of new projects which are expected to massively increase the firm's cash flow and greatly improve the MLP's financial situation. That includes continuing Energy Transfer Partners' efforts to deleverage the balance sheet.

Most recently, Energy Transfer Partners has sold off its contract compression business for $1.2 billion and exited part of its stake in Sunoco LP for $540 million. Proceeds were primarily used to reduce debt.

Source: Energy Transfer Partners Investor Presentation

There are several reasons why Energy Transfer Partners is so focused on deleveraging. First, interest rates are rising, so a strong investment grade credit rating is essential for ongoing access to low-cost growth capital.

That's especially important since the MLP's unit price is so low that it can't profitably raise equity capital, making it almost entirely dependent on low-cost borrowing for fundraising.

Perhaps most importantly, Energy Transfer Partners, like many other MLPs, believes that simplifying its corporate structure is essential for the continued growth of the business. The oil crash forced many MLPs and their sponsors to lower their costs of capital via either the sponsor buying out its MLPs (Kinder Morgan, ONEOK), or the MLP buying the IDRs rights of the sponsor (Holly Energy Partners, MPLX, Spectra Energy Partners).

By eliminating IDRs, which send up to 50% of marginal cash flow to the general partner, an MLP retains far more cash flow. Retained cash flow from operations can either be invested in growth, or used to pay investors safer distributions. Relying more on internally-generated cash flow also greatly reduces the cost of capital and makes future investments more profitable.

However, these corporate restructurings often require either a lot of debt or equity issuances. This means that an MLP and sponsor usually need to have a strong credit rating before they can proceed with a corporate consolidation.

Energy Transfer Partners' CEO Kelcy Warren has indicated that he is eager for such a move but that the top priority remains preserving the investment grade credit rating. ETP's currently rated BBB- and just one downgrade away from junk, which would greatly increase future borrowing and refinancing costs.

"If we're allowed to accelerate a consolidation of ETE and ETP, we will do that. It's just fundamentally simple as in – Ross you know the numbers about as well as anybody in the industry. We just can't risk any kind of negative view by rating agencies and until we get our financial health improved and the family, we will not be doing any kind of consolidation. But as soon as we can, we will." - CEO Kelcy Warren

If Energy Transfer Partners can execute on its turnaround plan, specifically bringing those $10 billion of new projects online, than both the balance sheet and distribution should become a lot safer.

Then Energy Transfer Partners can consolidate, most likely with Energy Transfer Equity buying its MLP. Management has said that it will reconsider such a deal in late 2019, after its growth backlog is complete.

A consolidated Energy Transfer Partners would be well situated to take advantage of the major boom in U.S. oil & gas that's expected over the coming decades. For example, the International Energy Agency expects the U.S. to be exporting five million barrels per day by 2023, making it the second largest net exporter in the world behind Saudi Arabia.

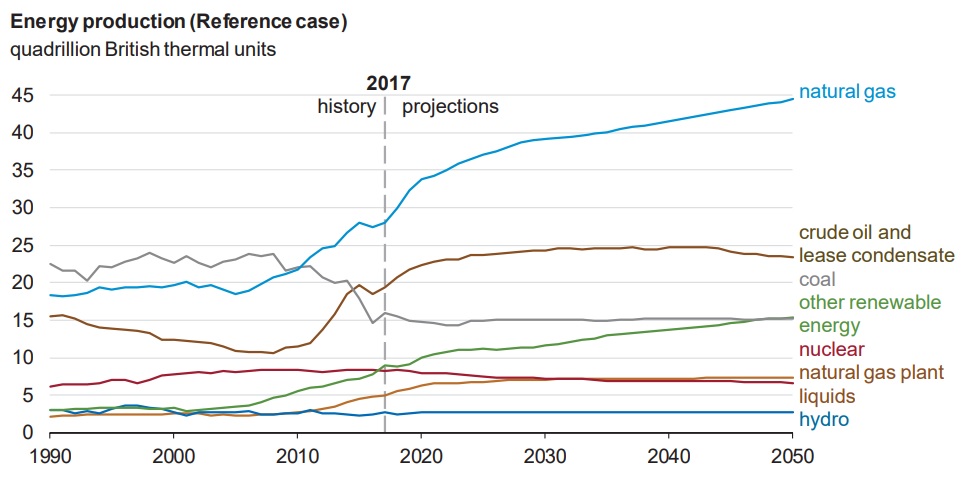

And according to the U.S. Energy Information Administration, domestic oil and condensate production is expected to remain strong through at least 2040, while U.S. natural gas production will keep rising through 2050.

Source: U.S. Energy Information Administration

The end result is an even greater need for midstream infrastructure. In fact, the long-term growth in oil & gas production is expected to require between $700 billion and $900 billion in new midstream investments through 2040, per analyst firm IHS.

In other words, if Energy Transfer Partners can succeed in its turnaround, then investors might be rewarded with many years of safe and growing distributions.

However, there are several important risk factors to consider that could make this MLP unsuitable for all but the most risk tolerant income investors.

Key Risks

Regulations are the first risk to consider. The same high regulations that raise the industry's barriers to entry can also cause major headaches when it comes to growth.

First, the most recent FERC ruling, which removes a tax allowance on cost of service contracts for interstate pipelines, is not expected to impact Energy Transfer Partners' tariff rates or distributable cash flow.

FERC's jurisdiction only applies to interstate pipelines, and many of Energy Transfer Partners' assets are not regulated by FERC, such as its LNG assets, intrastate pipelines, and storage facilities. Most of Energy Transfer Partners' contracts are also negotiated market rates, many of which are below the FERC-approved maximum tariff rate.

While the FERC rule change may not negatively impact the MLP, like all midstream operators, Energy Transfer Partners still faces numerous regulatory hurdles when it comes to completing its projects on time and on budget.

For example, in 2017 an accident on part of its Rover pipeline system, which represents the MLP's largest growth project, caused FERC to order it to cease construction. As a result, the partnership's targeted first-quarter 2018 service date will be pushed back several months.

Energy Transfer Partners was also ordered to halt construction on part of an NGL pipeline it was constructing, delaying that projects launch by 18 months, and the firm battled costly legal battles and environmental-related setbacks from regulators for years before finally completing its Dakota pipeline in the Bakken formation in 2017.

Simply put, completing large midstream projects is costly, time consuming, and fraught with delays. This can cause major funding issues, which threw management's ambitious growth plans for a loop in 2017. Which brings up another big risk, the MLP's current liquidity problems.

Energy Transfer Partners has a very large growth backlog but is having problems raising enough cheap capital to funds its construction. That's because often the expected cash flow from a project coming online will be used as collateral for financing other projects.

In 2017, the continued delays on the Dakota pipeline disrupted financing for two other projects and forced Energy Transfer Partners to try to sell $5 billion in assets to private equity giant Blackstone (BX). However, this deal fell apart at the last minute and forced the MLP to go through necessary, but very expensive, financial engineering.

In mid-August 2017, ETP had to sell $1 billion in new units, at a cost of equity well north of 10%, far above the cash yield any of its projects are expected to generate. But that was just the start of a very busy year of iffy capital raises the MLP was forced to undergo.

In October 2017, the MLP had to sell 32% of its stake in the $4.2 billion Rover Pipeline for $1.6 billion, resulting in a big hit to future cash flow generation. Just one month later, ETP issued $1.5 billion in preferred stock at yields of 6.25% to 6.6%. While this is certainly preferable to a common equity rause, preferred shares have first claim on any distributions, which could make it harder to maintain the current payout.

Finally, in January 2018, Energy Transfer announced two major deals to hopefully wrap up its short-term capital raising needs. The partnership sold $1.2 billion in compressions assets to USA Compression Partners (USAC), and 17.3 million units of Sunoco LP (SUN) back to that Kelcy Warren-controlled MLP for $540 million.

Both deals mean reduced DCF going forward. However, management now believes that the company should have enough capital to complete all of its planned $4.5 billion in project costs for 2018, helping the company avoid any more costly equity raises at dilutive prices.

The takeaway to remember is that MLP's are extremely capital-intensive businesses. If they are on shaky financial ground (high IDRs, risky DCF payout ratios, too much leverage, very high dividend yield), they can quickly fall into a liquidity trap and be forced to choose between funding their full distribution, continuing all of their growth projects, or maintaining their credit rating.

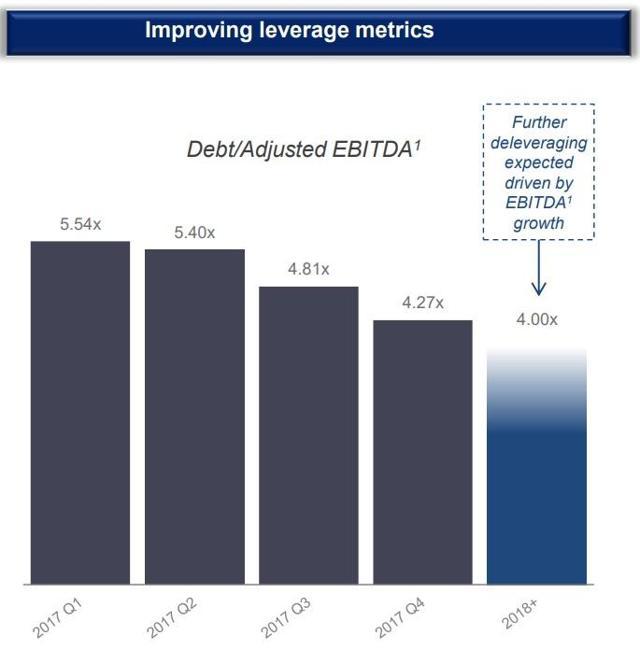

Maintaining a strong investment grade credit rating is especially important in a rising interest rate environment. Energy Transfer has a BBB- credit rating from S&P, just one level above junk due to the its previously very high leverage (debt/adjusted EBITDA) ratio. Credit rating agencies like to see leverage ratios of 4.5 or less for this type of business.

While Energy Transfer Partners projects its leverage ratio will fall to a safer 4.0 by the end of 2018, hopefully resulting in credit upgrades, for 2017 it averaged 4.9. That was much higher than the industry average of 4.4.

Another reason for the MLP's relatively low credit rating is because about 20% of its DCF is highly sensitive to commodity prices. With the MLP's ex-IDR waiver coverage ratio currently at 1.09, commodity risk could rather quickly put the distribution on shakier ground.

Energy Transfer Partners is essentially walking a tightrope trying to balance its current distribution while still funding essential growth projects, which it absolutely needs to deleverage and secure its credit rating.

While the partnership can still borrow relatively cheaply due to its investment grade rating, it must balance any new debt issuances with equity as well to keep its relative debt metrics from rising. This is what forced the MLP to issue so much equity at horribly dilutive rates, as well as sell billions of dollars in cash flow-producing assets.

With that said, if management can in fact complete its projects on time and on budget, than Energy Transfer Partners is likely to see its DCF increase significantly over the next few years, increasing its distribution coverage ratio to more sustainable levels.

The potential issue is management's ability to bring projects online at expected costs and on time. Unfortunately, many of the challenges standing in Energy Transfer Partners' way are beyond management's control.

For example, according to the Association for Oil Pipelines, the recently imposed 25% steel tariffs will increase the cost of the average pipeline project by $76 million, and the expense of a major project by $300 million or more.

Next there are those pesky regulators and legal challenges that can force long and costly delays in construction. According to CFO Tom Long, permitting delays on part of the Rover Pipeline mean that this project's expected completion date has now been pushed back, yet again, to the second quarter of 2018.

Meanwhile, a Federal Judge in Louisiana just revoked the previously issued permit for the Bayou Bridge oil pipeline, citing environmental concerns. The MLP will appeal the action, but this project might, like Dakota, spend years in legal limbo.

And remember that Energy Transfer Partners has no large liquidity reserves. Any unexpected cash flow disruption or delay might result in the firm not having enough capital on hand to complete its remaining growth projects, which it's counting on to dig out of its current liquidity trap.

In other words, at least over the short to medium term, Energy Transfer Partners appears to be a higher risk stock with little wiggle room. Depending on how various factors play out (many of which are outside of the company's control), management might still be forced to cut the payout, as it did in 2017 when it merged Sunoco Logistics Partners with Energy Transfer Partners in a $20 billion all-stock deal.

Technically, Sunoco Logistics purchased Energy Transfer Partners; however, the larger MLP retained the current moniker. More importantly, the large amount of dilution involved in the deal forced the payout to be cut 24%.

With management indicating that it's eager to simplify Energy Transfer's corporate structure further, there remains a large amount of uncertainty about whether or not Energy Transfer Partners’ distribution will remain safe, even if the coverage ratio rises to normally secure levels.

Closing Thoughts on Energy Transfer Partners

Energy Transfer Partners is one of America's largest owners of attractive midstream assets. Given the long-term growth potential of U.S. oil & gas production, and thus the midstream MLP industry, Energy Transfer Partners could have an attractive growth runway for many years to come.

However, to realize its potential, the partnership has to successfully clear several hurdles, making it a higher risk and very uncertain turnaround story. Almost nothing can go wrong with management's ambitious growth plans over the next two years.

When combined with management's desire to simplify Energy Transfer's corporate structure and the implications that could have for the distribution, conservative income investors should probably avoid this MLP.