Starwood Property Trust (STWD)

Starwood Property Trust (STWD) was founded in 2009 and is America's largest commercial mortgage REIT. The firm invests across the real estate capital structure and focuses primarily on originating, acquiring, financing, and managing commercial mortgage loans and other commercial real estate debt investments in both the U.S. and Europe.

Starwood Property Trust is externally managed by Starwood Capital Group, which has over $50 billion in assets under management and more than 25 years of commercial real estate experience.

Starwood Property Trust is externally managed by Starwood Capital Group, which has over $50 billion in assets under management and more than 25 years of commercial real estate experience.

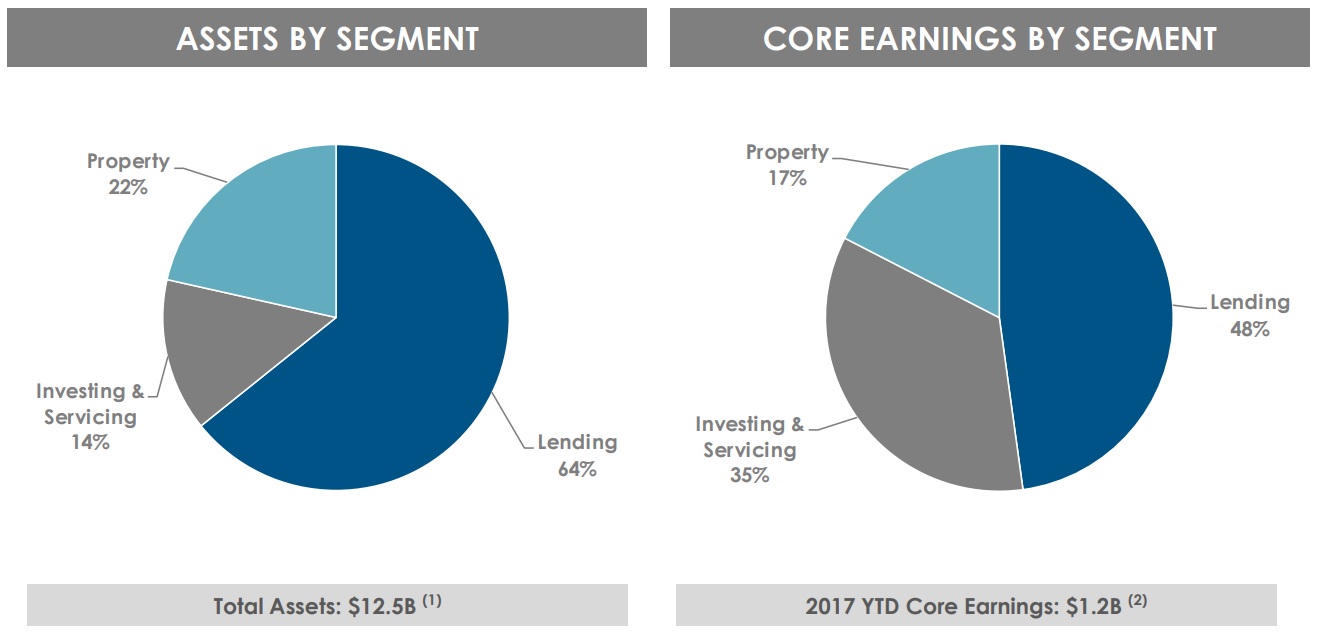

The commercial mortgage REIT, or CmREIT, has three business segments:

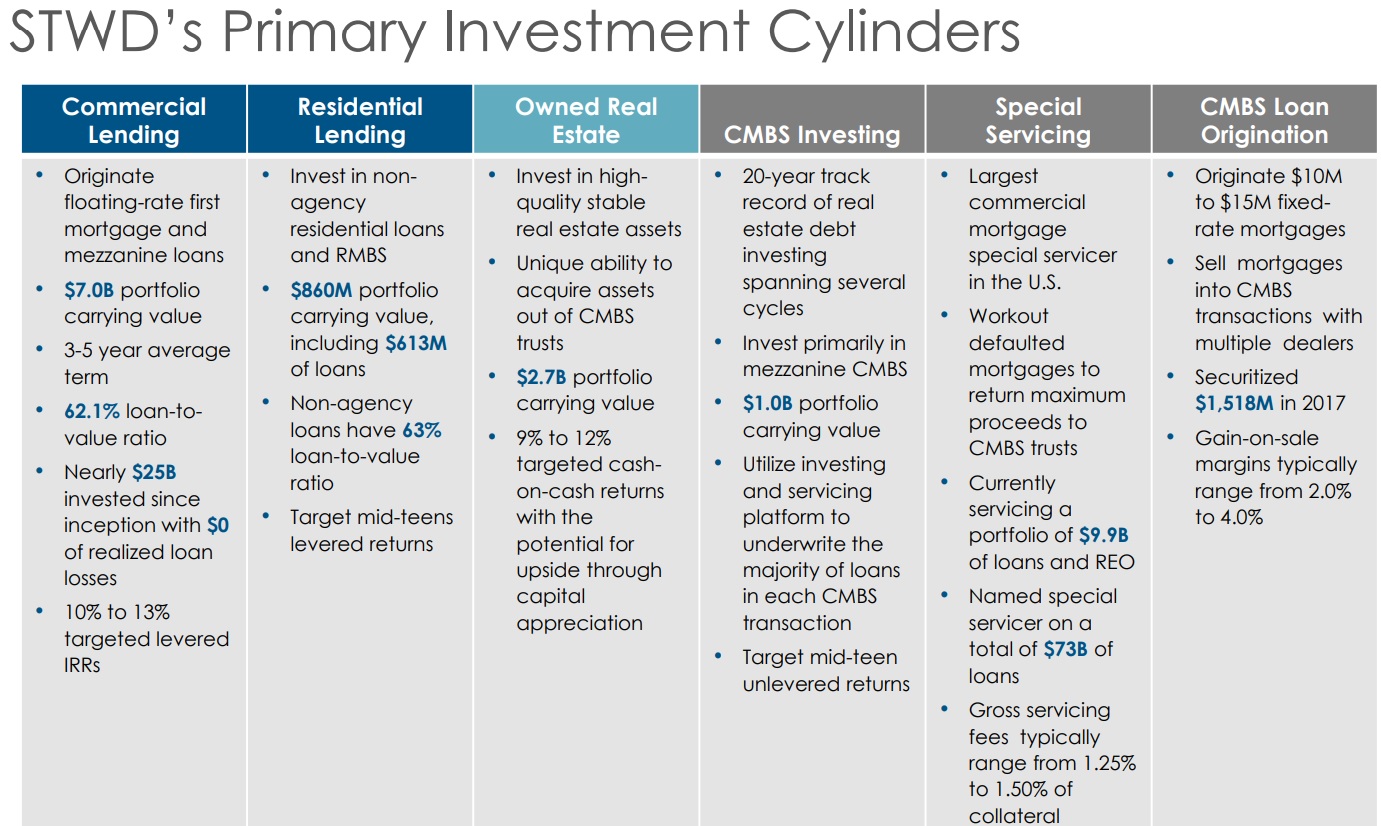

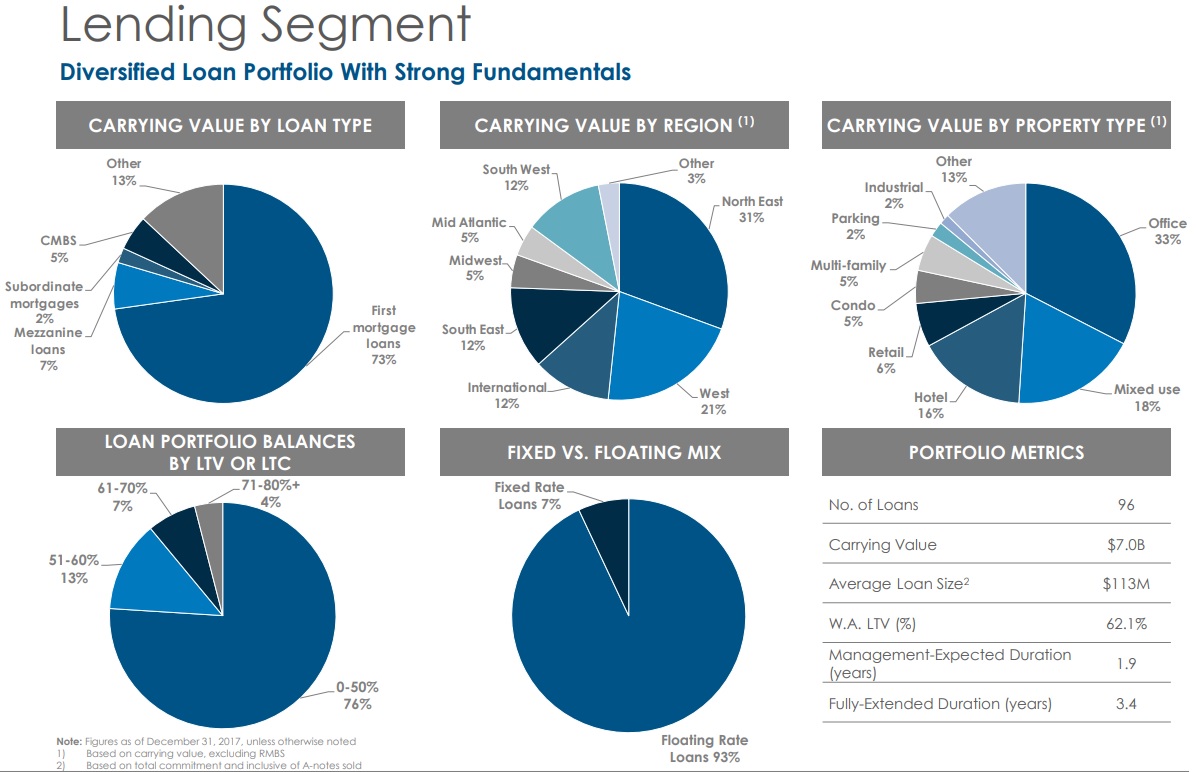

- Real Estate Lending (48% of earnings): Starwood offers real estate borrowers financing in the form of first mortgages, subordinate debt, mezzanine loans, B-notes and preferred equity. The company possesses the size and scale to serve as a one-stop lender, leveraging its expertise across virtually every real estate asset class to help source, structure, and underwrite real estate transactions.

- Real Estate Investing and Servicing (35% of earnings): includes a variety of business lines focused on commercial mortgage-backed securities (CMBS) and commercial real estate investments (Starwood can underwrite hundreds of loans within a short timeframe), special servicing operations (Starwood manages and works out non-performing assets and property liquidations), and a commercial mortgage conduit platform (Starwood originates five-, seven- and 10-year fixed-rate mortgages).

- Real Estate Property (17% of earnings): in 2014, Starwood began investing in real estate assets to complement its other businesses. These equity investments, totaling approximately $3 billion, comprise high-quality, stable real estate assets such as apartment buildings, office buildings, and retail properties.

Since the company actually owns physical commercial rental properties, Starwood Property is a hybrid between mortgage REITs and equity REITs. That being said, lending and servicing commercial mortgages still make up the vast majority of its assets and earnings.

Business Analysis

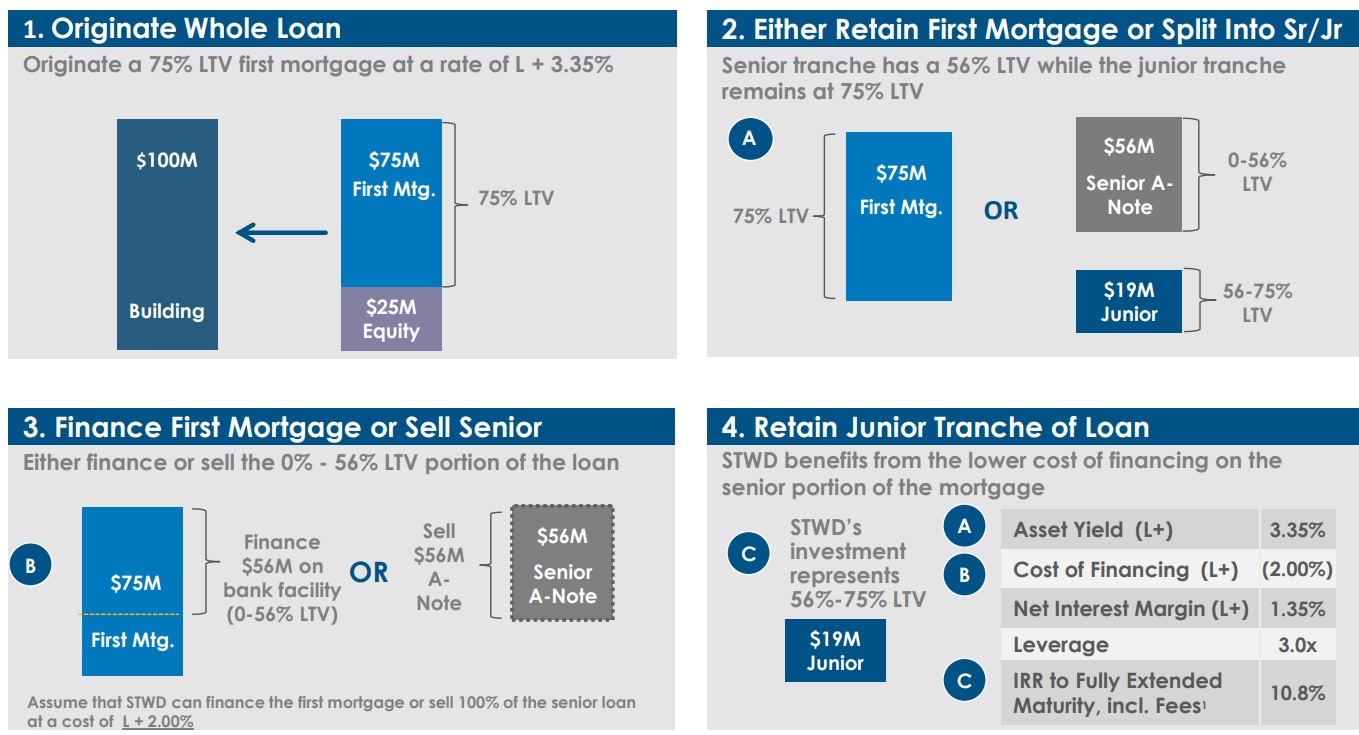

Starwood Property's core business works by financing commercial mortgage loans for three to five-year terms.

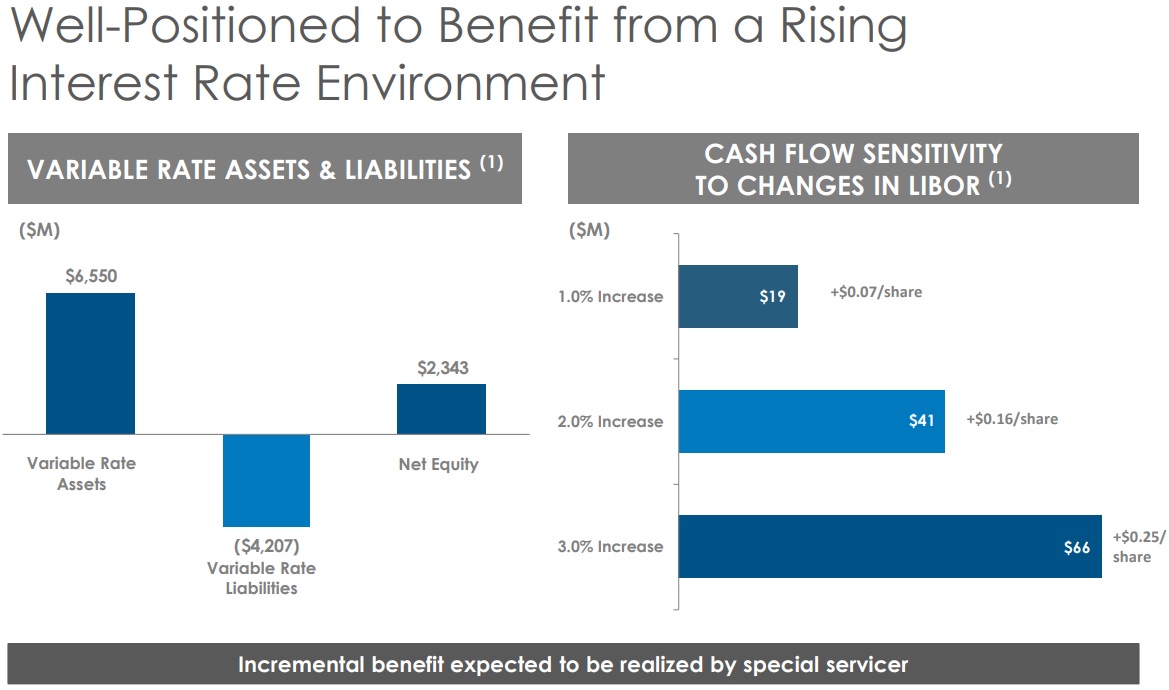

Over 90% of these loans are indexed to LIBOR (the London Interbank offering rate), a global benchmark for commercial loans. Through the use of leverage, Starwood is able to earn attractive returns (about 11% internal rates of return) on such loans which customers make to acquire or build commercial real estate.

In addition, as the graphic below shows, Starwood often securitizes or sells part of these mortgages to third parties, usually keeping about 25% of the loan on its books. This grants it the mortgage payments from such deals while allowing it to also recycle capital into further profitable loans.

Over 90% of these loans are indexed to LIBOR (the London Interbank offering rate), a global benchmark for commercial loans. Through the use of leverage, Starwood is able to earn attractive returns (about 11% internal rates of return) on such loans which customers make to acquire or build commercial real estate.

In addition, as the graphic below shows, Starwood often securitizes or sells part of these mortgages to third parties, usually keeping about 25% of the loan on its books. This grants it the mortgage payments from such deals while allowing it to also recycle capital into further profitable loans.

Starwood's operations also include ancillary commercial mortgage business lines including servicing other commercial mortgages. This means that Starwood operates as a third-party back office for other commercial loan originators.

Specifically, Starwood will handle the day-to-day logistics of collecting payments and make advances on payments when a customer is late with a payment (thus providing smoothed out cash flow for the commercial mortgage lender).

In the event of a default, Starwood makes advances on legal fees and handles the foreclosure procedures for commercial properties. In exchange, the company collects a small percentage of the mortgage payment.

Specifically, Starwood will handle the day-to-day logistics of collecting payments and make advances on payments when a customer is late with a payment (thus providing smoothed out cash flow for the commercial mortgage lender).

In the event of a default, Starwood makes advances on legal fees and handles the foreclosure procedures for commercial properties. In exchange, the company collects a small percentage of the mortgage payment.

In recent years, Starwood has been diversifying into other businesses including owning residential mortgage-backed securities (RMBS). This means the company is buying loans backed by bundled home mortgages.

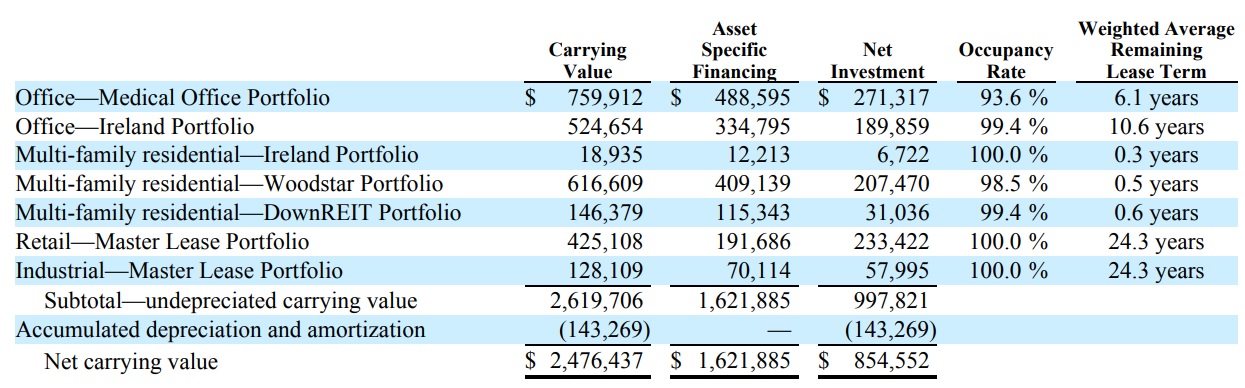

Since 2014, Starwood has also been acquiring real estate properties to own and manage for others, on which it collects rent and management fees. The firm has invested a total of $2.5 billion in 113 properties, including 10,733 apartment units. The weighted average occupancy rate is 97.8%, and management is focusing mostly on commercial properties with very stable cash flow generated by long-term leases.

Since 2014, Starwood has also been acquiring real estate properties to own and manage for others, on which it collects rent and management fees. The firm has invested a total of $2.5 billion in 113 properties, including 10,733 apartment units. The weighted average occupancy rate is 97.8%, and management is focusing mostly on commercial properties with very stable cash flow generated by long-term leases.

Given the amount of financial leverage involved in this business, good risk management is key to successfully running a mortgage REIT. Starwood's moves to diversify its business into other areas certainly helps, and disciplined underwriting and loan management are critical to reduce the risk of loan defaults and losses.

So far, the firm's track record is flawless. Since its 2009 IPO, Starwood has made $39 billion in investments with zero realized loan losses on its $26 billion of commercial real estate loans.

Now it should be noted that the firm's perfect record is largely due to the fact that that global economy has been growing since 2009, resulting in rising commercial property prices and generally favorable financial conditions for borrowers.

That being said, Starwood is very conservative with its lending. For example, 73% of its loans are first lien mortgages, meaning that in the event of a default, the firm gets first crack at recouping its capital. In addition, the mortgage REIT's average loan-to-value (LTV) ratio is just 62%, and 76% of its loans have LTVs of 50% or less.

The LTV ratio reflects the amount of a property's value that was borrowed, with the remainder representing amount that is the borrower's equity. A lower LTV ratio indicates that the borrower has a more substantial amount of equity in the property, reducing some of Starwood's risk if the property's value declined and they stopped making payments.

So far, the firm's track record is flawless. Since its 2009 IPO, Starwood has made $39 billion in investments with zero realized loan losses on its $26 billion of commercial real estate loans.

Now it should be noted that the firm's perfect record is largely due to the fact that that global economy has been growing since 2009, resulting in rising commercial property prices and generally favorable financial conditions for borrowers.

That being said, Starwood is very conservative with its lending. For example, 73% of its loans are first lien mortgages, meaning that in the event of a default, the firm gets first crack at recouping its capital. In addition, the mortgage REIT's average loan-to-value (LTV) ratio is just 62%, and 76% of its loans have LTVs of 50% or less.

The LTV ratio reflects the amount of a property's value that was borrowed, with the remainder representing amount that is the borrower's equity. A lower LTV ratio indicates that the borrower has a more substantial amount of equity in the property, reducing some of Starwood's risk if the property's value declined and they stopped making payments.

In the event that a client defaults, Starwood's focus on making relatively low LTV loans means that it can repossess a property and sell it, thus recouping its investment and improving its chances of avoiding a loss.

Of course, that only works if the commercial real estate market is strong and prices haven't declined as they usually do during recessions. To minimize this risk, Starwood maintains a highly diversified portfolio with properties spread out across the U.S. and even internationally.

Of course, that only works if the commercial real estate market is strong and prices haven't declined as they usually do during recessions. To minimize this risk, Starwood maintains a highly diversified portfolio with properties spread out across the U.S. and even internationally.

One big benefit that commercial mREITs have over their residential mREIT cousins is that the bulk of their loans are floating rate (residential mortgages are almost all fixed-rate). As a result, commercial mREITs have the potential to benefit from rising interest rates because most of the time the yield on their loans rises faster than their borrowing costs.

For example, management expects that if LIBOR were to rise by 300 basis points, then Starwood's core earnings would increase by $0.25 per share ,or about 11% above 2017's level. In the past year, LIBOR is up about 120 basis points as rising interest rates in the U.S. (and to a lesser extent overseas) have pushed up commercial lending rates.

For example, management expects that if LIBOR were to rise by 300 basis points, then Starwood's core earnings would increase by $0.25 per share ,or about 11% above 2017's level. In the past year, LIBOR is up about 120 basis points as rising interest rates in the U.S. (and to a lesser extent overseas) have pushed up commercial lending rates.

The combination of conservative management and disciplined underwriting has allowed Starwood Property to be one of the most reliable mortgage REITs when it comes to covering its generous dividend. Since 2013, the mREIT's core earnings payout ratio has been 88%, and it fell to 86% in 2017.

While Starwood's payout ratio is high on an absolute basis, remember that mREITs must pay out 90% of their taxable income as dividends. As a result, the core earnings payout ratio for typical commercial mREITs is usually about 90% to 100%. Starwood's industry-leading low payout ratio indicates that it has solid dividend coverage today and should be able to continue its streak of uninterrupted payouts, at least over the short to medium term.

As far as commercial mREITs go, Starwood Properties is one of the best-managed firms in the space. However, there are some very important risks to owning any mREIT, even an industry leader like Starwood.

Key Risks

One of the most important differences between equity REITs and mortgage REITs is that almost all mortgage REITs are externally managed. This means that rather than work directly for shareholders, management services come from an external manager. As a result, conflicts of interests between retail investors and management can sometimes arise.

That's because externally managed REITs have compensation plans (called management agreements) that effectively make them operate almost like hedge funds since management is paid a fixed base management fee and an incentive fee.

In the case of Starwood Property Trust, the base management fee is 1.5% of shareholder equity (total share issuances and retained earnings over time). In addition, management is paid an incentive fee of 20% of core earnings growth above an 8% annual hurdle rate.

In recent years, management fees in 2015, 2016, and 2017 have totaled:

- 2015: $96.9 million, or 13.2% of revenue

- 2016: $93.8 million, or 12.0% of revenue

- 2017: $109.9 million, or 12.5% of revenue

This high amount of revenue going to management incentivizes large growth in assets, including from the frequent issuance of new equity (shares) to buy more assets and thus inflate management pay.

The problem is that it also creates very high cost of capital that can make it challenging for the mREIT to grow its core earnings (due to share dilution), which ultimately sustains and grows the dividend over time.

The problem is that it also creates very high cost of capital that can make it challenging for the mREIT to grow its core earnings (due to share dilution), which ultimately sustains and grows the dividend over time.

Larger and better capitalized firms, such as the big banks, have much lower costs of capital. Should they infringe on Starwood's core business, the firm could struggle to find profitable investment opportunities.

Speaking of profitability, the margin Starwood can obtain on its new mortgages is not just dependent on current interest rates, but also on the supply and demand balance of the industry.

In recent years, more competition has come from commercial banks increasing capital inflows into commercial mortgage lending, and private equity firms have launched their own commercial mREITs as well. The more competition there is, the greater the risk that Starwood will be priced out of the best deals which could threaten its ability to grow profitably over time.

In recent years, more competition has come from commercial banks increasing capital inflows into commercial mortgage lending, and private equity firms have launched their own commercial mREITs as well. The more competition there is, the greater the risk that Starwood will be priced out of the best deals which could threaten its ability to grow profitably over time.

While management continues to find attractive opportunities for deploying capital, including $9.5 billion in investments over the past 16 months, remember that most of those investments are in relatively short-term loans that will have to be replaced within about three years.

Or to put it another way, the same strong economy that is fueling a boom in commercial lending is also attracting more low-cost capital to fund those loans. Thus, while Starwood has enjoyed solid growth in its core earnings in recent years, its ability to do so in the future is far from certain.

Or to put it another way, the same strong economy that is fueling a boom in commercial lending is also attracting more low-cost capital to fund those loans. Thus, while Starwood has enjoyed solid growth in its core earnings in recent years, its ability to do so in the future is far from certain.

Another potential problem for mREITs like Starwood is that they can't retain a lot of internally-generated cash flow to fund growth since they are required by law to pay out at least 90% of their taxable income as dividends. As a result, they must take on a lot of debt and sell new shares to raise growth capital.

However, due to the high amount of leverage required to run a mortgage REIT business, Starwood has a junk credit rating. The firm faces relatively high borrowing costs and would see its cost of capital move even higher if interest rates continue to rise.

Another problem for mREITs is that if their share price is too low, such as below book value per share, then any equity raised is dilutive to investors and reduces book value over time. This is important because in the mREIT industry, price-to-book value is one of the most common valuation methods.

In other words, if Starwood's share price were to trade at a discount to book value (which has happened before), then it can't raise equity growth capital profitably. Any shares sold will reduce the book value per share (and raise the cost of the dividend) and can trap the share price in a downward spiral that cuts off growth and threatens the safety of the dividend.

Another important risk to consider is that unlike equity REITs, who own hard assets that generate steady cash flow, mREITs mostly own assets with limited lifespans. For instance, commercial mortgages usually have three to five-year durations (Starwood's average loan is for 3.4 years) which means that the company must frequently replace maturing loans with new ones. Therefore, even if Starwood's current core earnings cover the dividend well, its financial situation could change meaningfully in the future.

Finally, Starwood's core earnings and dividend safety are ultimately tied to the health of the economy. Most mREITs, including Starwood, went public after the financial crisis and don't have a track record of how their loan portfolios will fair in an economic downturn.

Rising loan defaults are likely to result in falling interest income and potential loan losses that could force the company to cut its dividend. Mortgage REITs with long enough operating histories performed very poorly during the last recession, with virtually all of them cutting their dividends.

Rising loan defaults are likely to result in falling interest income and potential loan losses that could force the company to cut its dividend. Mortgage REITs with long enough operating histories performed very poorly during the last recession, with virtually all of them cutting their dividends.

Overall, mortgage REITs, even commercial ones like Starwood that can benefit from rising rates, are very different than equity REITs. Equity REITs are arguably far better choices for risk averse investors looking for simpler, safer, and consistently growing dividends in all different types of economic and interest rate environments.

Closing Thoughts on Starwood Property Trust

Commercial mortgage REITs are a potentially attractive way for risk-tolerant income investors to profit during times of strong economic growth. And Starwood Property Trust is arguably one of the best companies in the industry thanks to its leading scale, diversification, and somewhat more conservative lending practices.

However, investors must understand that all mortgage REITs are extremely complex businesses with major differences compared to equity REITs. Their use of leverage to magnify investment returns, sensitivity to the economy and interest rates, opaque balance sheets, and external management teams mean that conservative investors are likely best off avoiding the space.