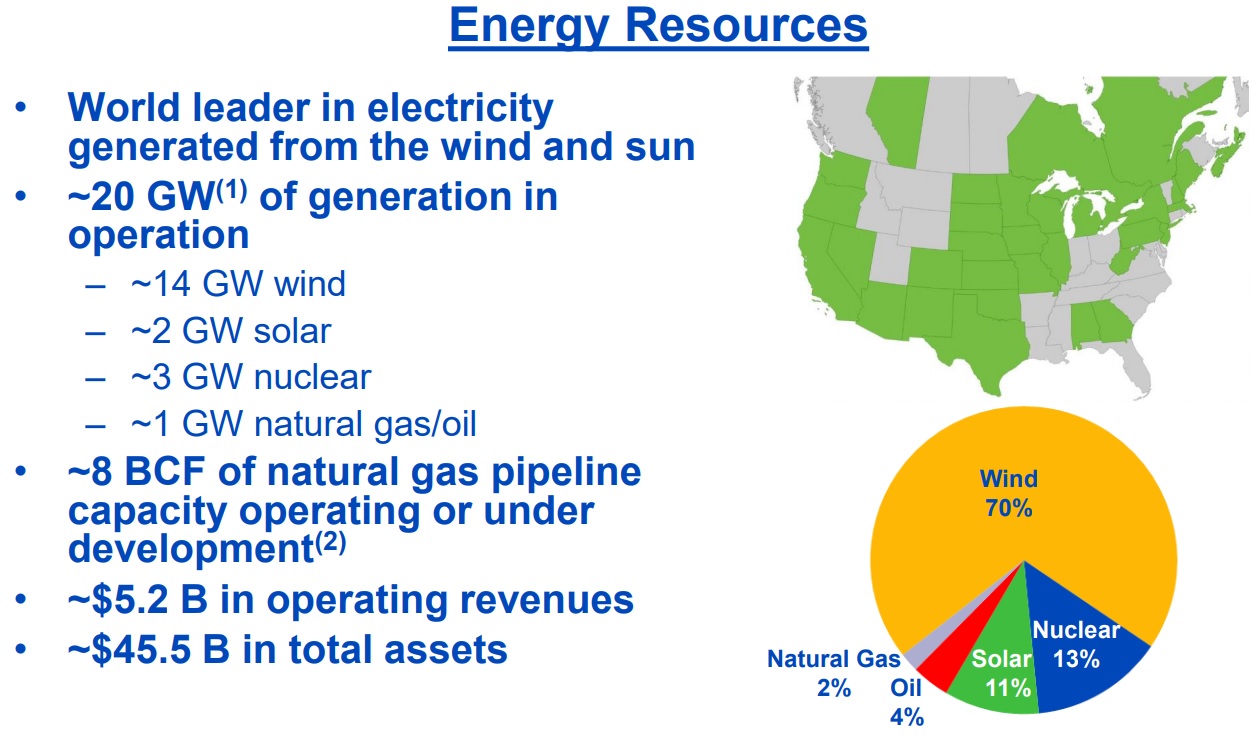

Founded in 1984 as Florida Power & Light (FPL), NextEra Energy (NEE) changed its name in 2010 to better represent its aggressive push into renewable solar and wind power (the company is the world’s number one generator of wind and solar energy).

NextEra Energy has two main business segments:

Florida Power & Light (70% of sales, 64% of operating earnings): the largest rate-regulated electric utility in the state of Florida servicing 9.5 million Floridians via its 5 million FPL accounts.

NextEra Energy Resources(30% of sales, 36% of operating earnings): the world's largest operator of wind and solar projects used to electricity in wholesale markets. NextEra Energy is one of America’s largest electric utilities with 46.8 GW of capacity in 33 states and Canada, and approximately 43% of that capacity comes from this subsidiary. This division provides unregulated power sold under long-term (usually 20-year) contracts and represents the vast majority of the company's renewable energy capacity. It is also investing in battery storage.

Source: NextEra Energy Investor Presentation

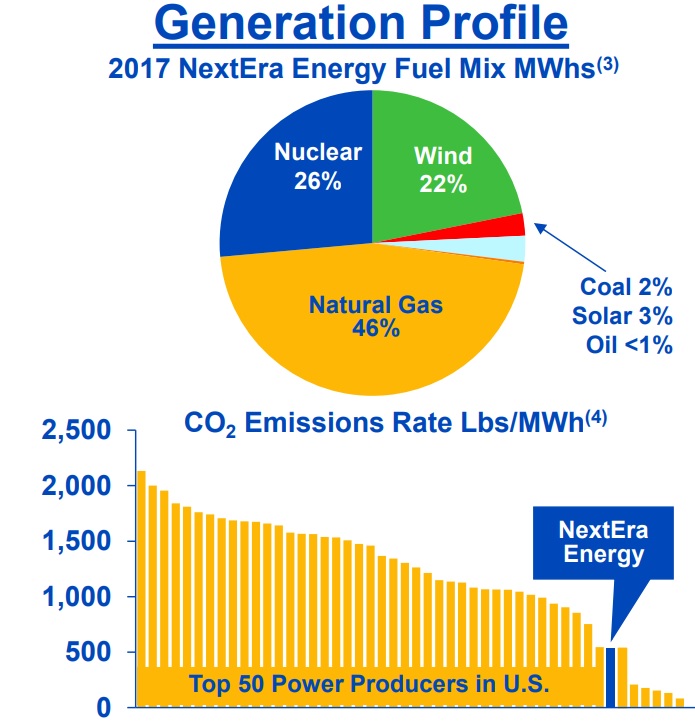

Thanks to its large focus on renewable power, NextEra Energy has one of the cleanest power generation mixes in the industry, and one of the lowest carbon footprints.

Source: NextEra Energy Investor Presentation

Business Analysis

The regulated electric utility industry enjoys numerous advantages that tend to result in predictable earnings and dividends. Businesses in this sector are essentially government-sanctioned monopolies since they are granted exclusive territorial rights to provide electricity to customers.

Regulated utilities earn a guaranteed rate of return on the capital they invest, but their allowed return on equity is capped in order to provide customers with fair prices while still encouraging the utility to invest in the reliability of its network. The end result is usually an extremely steady and profitable stream of cash flow.

NextEra Energy has benefitted from the favorable regulatory environment in Florida, which is one of the fastest-growing states in America and thus has enormous energy infrastructure needs.

Specifically, the U.S. Census Bureau expects the states population to grow 2.3% annually from 21.3 million people in 2017 to 28.7 million in 2030. That's about in line with the state's retail sales growth over the past decade.

Source: Bloomberg

Florida Light & Power mostly serves the faster-growing coastal parts of the state. This is where the need for new energy infrastructure is greatest, so regulators allow the utility an average return on equity of 10.55%. That's about 1% higher than the average return on equity allowed for U.S. electric utilities.

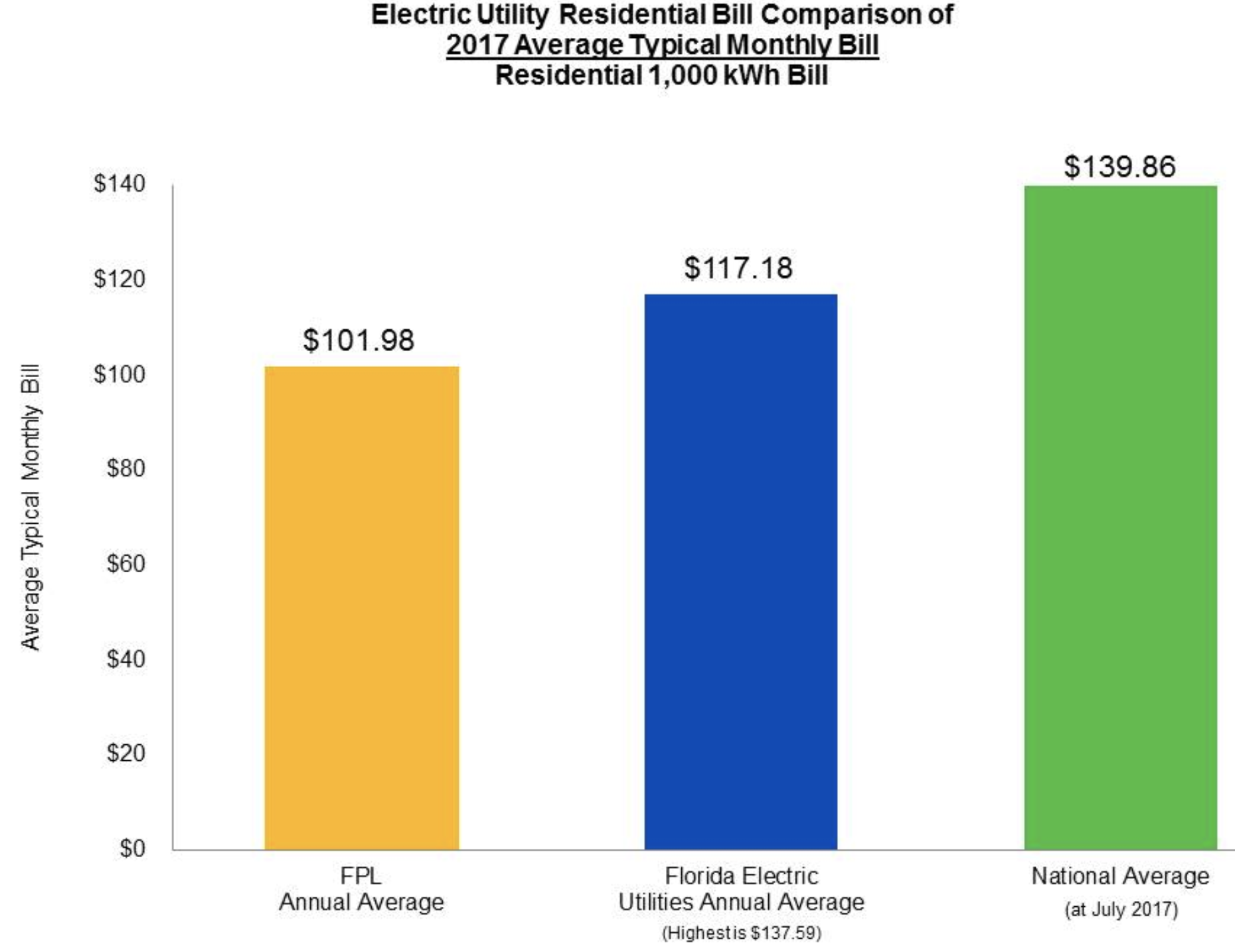

This preferential treatment from regulators is largely due to the fact that NextEra's efficient operations (courtesy of economics of scale and newer assets that require less maintenance spending) result in operating costs per MwH of just $13 compared to $29 for most U.S. electric utilities.

As a result, Florida Light & Power is charging its customers very reasonable rates despite the company's solid profitability. As you can see below, the price Florida Light & Power charges a residential customer for 1,000 kWh of consumption per month is well below the average of utilities within the state and across the country.

Source: NextEra Energy Annual Report

Essentially, NextEra Energy's operational leverage is so great that it can afford to invest very profitably without charging rates that anger consumers and put pressure on regulators to lower its allowed return on equity.

Regulators have therefore felt comfortable signing off on massive investment projects granting NextEra Energy favorable returns that should allow for some of the fastest growth in the industry.

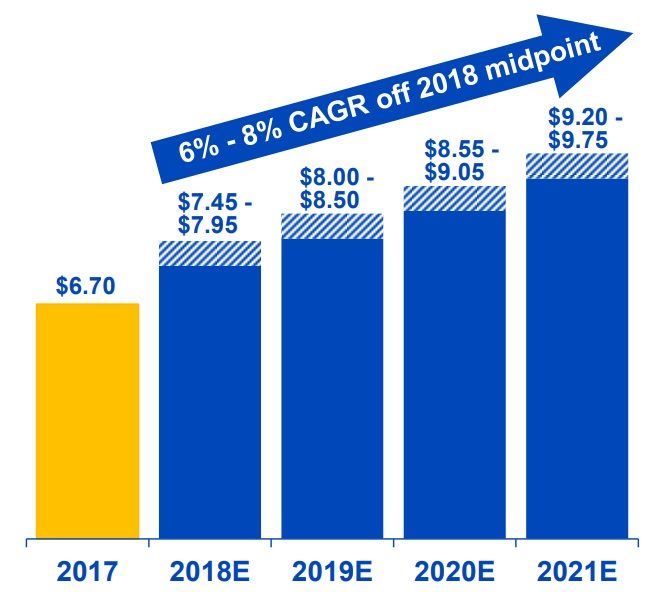

For example, Florida Power & Light expects to invest about $18.5 billion into expanding its assets and services in the state between 2017 and 2020. This is likely to generate 6% to 8% annual growth in adjusted EPS through 2021 and will moderately increase NextEra Energy's mix of cash flow from regulated activities.

Source: NextEra Energy Partners

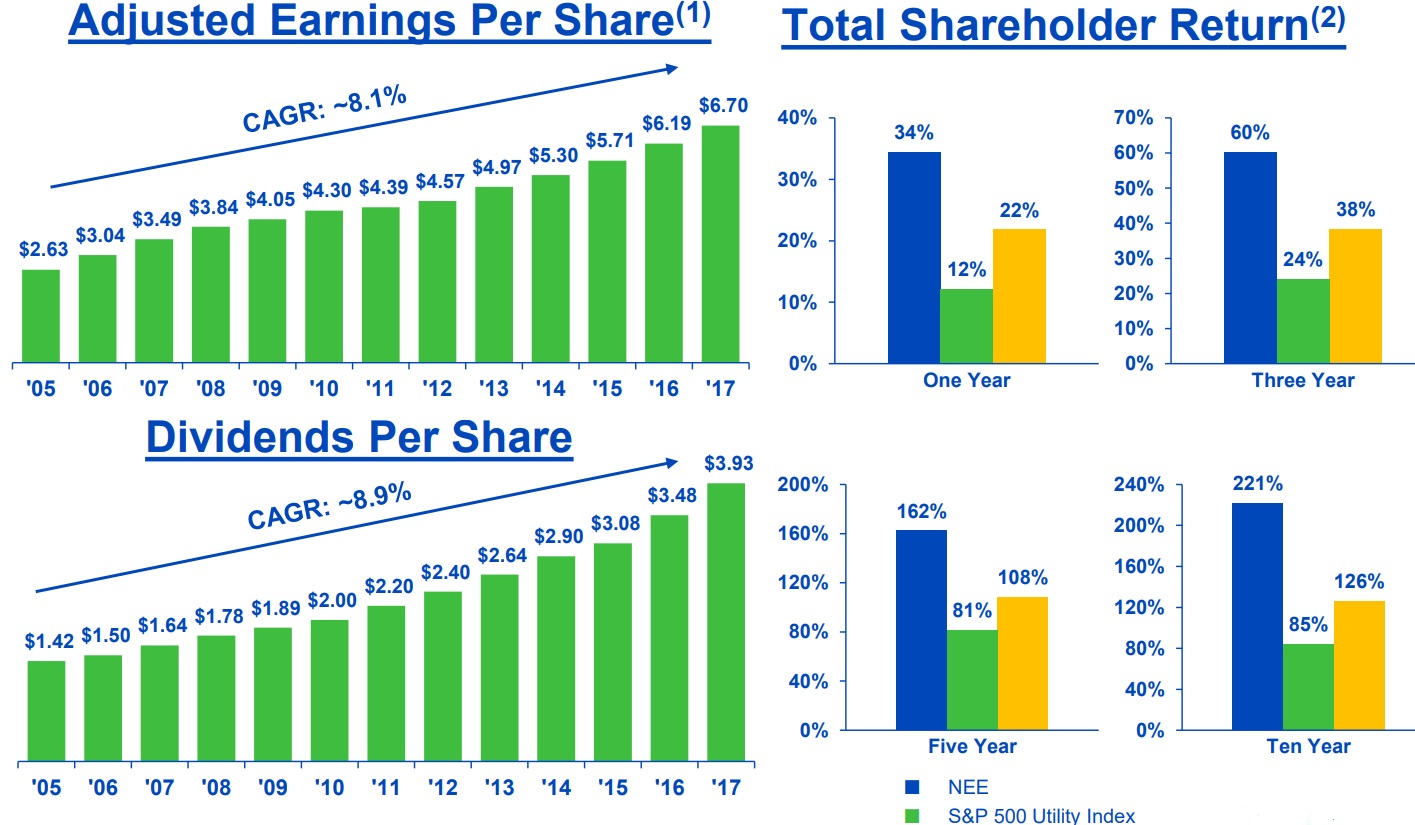

Management plans to use this fast growth rate to fuel even higher dividend growth of 12% to 14% a year through the end of 2020. This continues a tradition of industry-leading EPS and payout growth that has allowed NextEra Energy to be the top-performing regulated utility in America over the past 10 years.

Source: NextEra Energy Partners

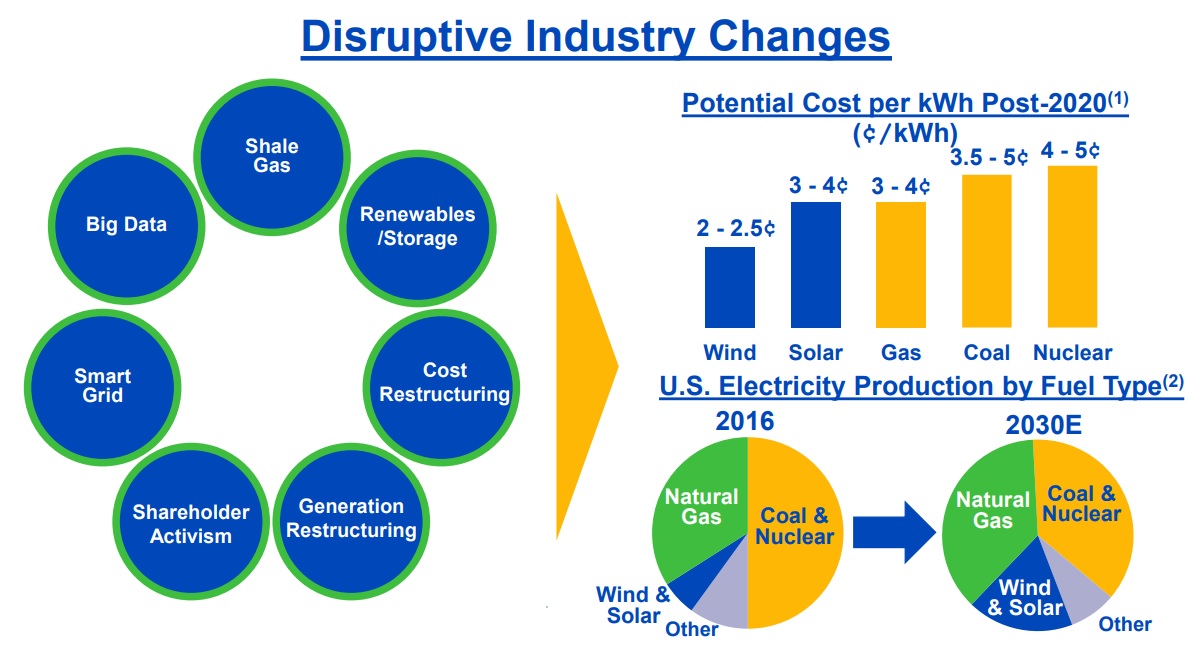

However, the biggest growth driver for the company isn't the Florida market, but rather its shift into the future of U.S. electric power in general. As you can see below, natural gas, wind and solar are expected to significantly increase their share of U.S. electricity production.

Source: NextEra Energy Investor Presentation

NextEra Energy is arguably the best positioned U.S. electric utility when it comes to the future of clean energy. That's thanks to the company's large focus on low-cost natural gas generation (with cheap inputs courtesy of the U.S. fracking boom), and also renewable energy like solar and wind.

In fact, the cost of solar and wind has declined by over 70% in the last few years and is expected to continue falling. By 2020, even without U.S. tax credits, the variable cost per kWh of solar and wind is expected to be equal to or less than gas, coal and nuclear.

Of course, these energy sources are highly variable and will require storage (such as batteries) to allow them to serve as base load power sources. Fortunately, the cost of Lithium Ion batteries has fallen more than 80% since 2010 and is expected to decline even further in the future (from $1,000 per kWh to $100 by 2030).

The company has already begun incorporating cheap storage into its renewable projects and expects to continue doing so in the future. This is because management expects that U.S. demand for solar and wind power will increase by 60 GW through 2020.

NextEra Energy Resources (NEER) is the company's non-regulated subsidiary tasked with exploiting this potential growth market and has a few key advantages.

First, because it is not regulated, this business actually benefits from the recent tax reform. Regulated utilities are legally required to pass on all tax savings in the form of lower rates. NextEra Energy Resources, on the other hand, is allowed to keep its approximate $1.9 billion in tax savings.

More importantly, NEER has its own subsidiary, NextEra Energy Partners (NEP). This is a yieldCO, which is similar to a master limited partnership, or MLP.

NEER is the general partner and sponsor, owning 65% of NextEra Energy Partners units (the equivalent of shares), and its incentive distribution rights, or IDRs. These incentivize NextEra Energy to grow NEP's distribution quickly, because 25% of all increases pass directly through to the parent company. That's in addition to the regular payouts on its 65% ownership stake.

NEER created this YieldCo because it is a tax-efficient way of funding NextEra's renewable energy ambitions. NextEra Energy Partners raises external debt and equity capital from investors to buy NextEra's renewable projects, thus allowing the parent company to recoup development expenses quickly.

In exchange, the YieldCo gains a cash flow producing asset, with revenues locked in under 20-year purchase power agreements with other large utilities in dozens of states and Canadian provinces.

Management expects NextEra Energy Partners to grow its distribution at 12% to 15% a year through the end of 2022, driven by the enormous amount of solar and wind projects it plans to sell it.

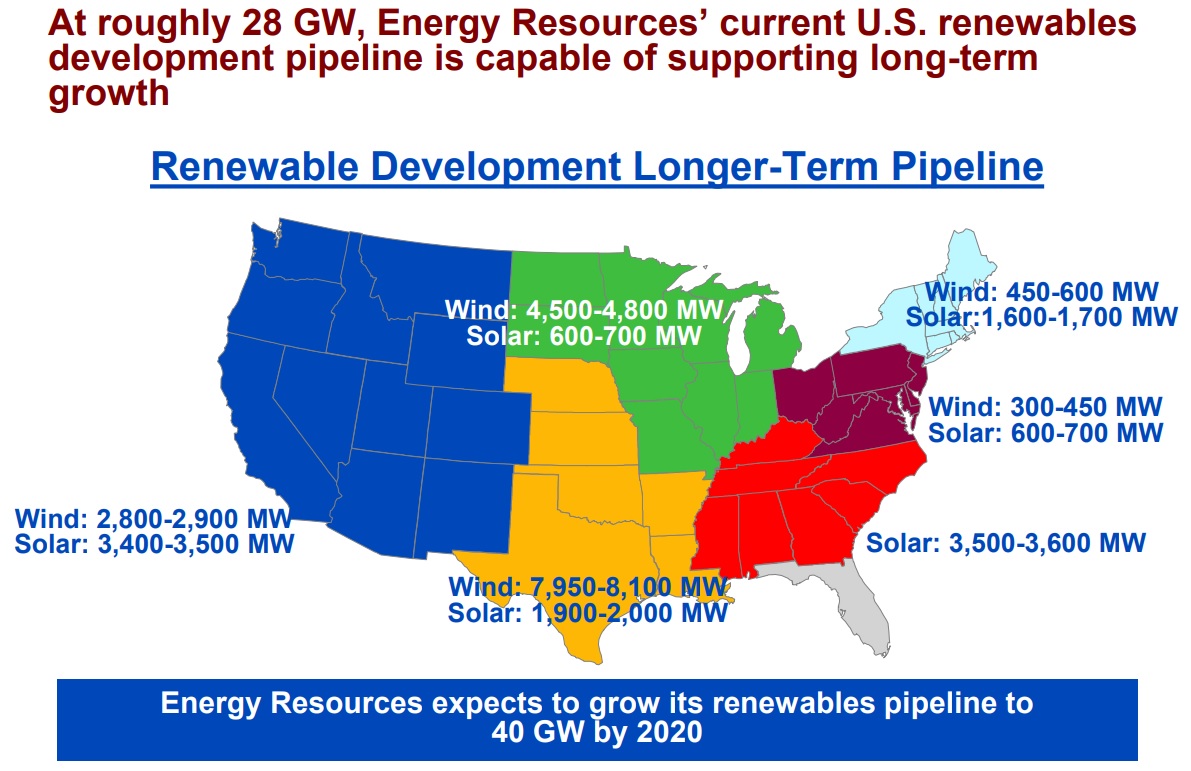

How big is the growth potential for NextEra in renewable power? Management currently has a long-term growth pipeline of 28GW.

To put that in perspective, NextEra Energy Partners currently owns 3.7 GW of renewable capacity, and NEER has about 20 GW. In other words, the company's base of clean energy assets, which is already the largest in the world, could still more than double over the next decade.

Source: NextEra Energy Investor Presentation

Overall, NextEra Energy appears to represent one of the fastest-growing electric utilities in America. The company's unique blend of regulated electric operations and clean energy provides a nice balance of predictable earnings, growth, cash flow diversification for a renewable energy future.

Key Risks

Florida Light & Power still represents the majority of NextEra's business and thus it has significant exposure to severe weather. For example, Hurricane Irma resulted in $1.3 billion in damage.

NextEra Energy is using its tax savings to fund these repairs in order to avoid passing these costs onto customers and potentially threatening its excellent relationship with state regulators.

However, because Florida Light & Power is a regulated utility, it will always face some regulatory risk. Despite its impressive abilities to grow quickly and profitably over time while charging low rates, the utility still relies on the above-average allowed return on equity that is granted by political appointees.

It's always possible (although very unlikely in this case) that populist political pressure could lead to regulators lowering its allowed return and thus reducing the utility's adjusted EPS and dividend growth rate.

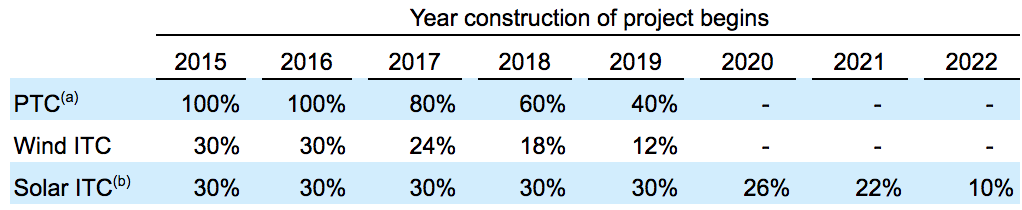

Perhaps the biggest growth risk is on the renewable energy side of the business. In the U.S., production tax credits (PTCs) for wind and solar power are scheduled to be phased out by the end of 2019 and 2022, respectively.

Tax credits for qualifying wind and solar projects are subject to the following phase-down schedule:

Source: NextEra Energy Annual Report

NextEra Energy has been able to use these tax incentives to provide a lot of tax equity financing, including $1 billion in 2017. As these credits expire and fall, the company will need to replace this source of growth capital, likely in the form of new debt and NextEra Energy Partners' equity.

However, interest rates are likely to rise in the future, meaning that the profitability of such projects might not be as high as in the past. The good news is that NextEra Energy has a strong balance sheet, which has earned the company an "A-" credit rating from S&P and should still allow it to borrow cheaply even in a rising rate environment.

However, NextEra Energy Partners has far more debt due to its YieldCo business model, although most of this debt is at the project level (non-recourse loans). The YieldCo has a sub-investment grade credit rating (junk bond status), which means that its borrowing costs are likely to rise much faster than the parent company.

In addition, NextEra Energy Partners is only retaining around 20% of its cash flow (the rest is distributed to unitholders), which means that it frequently has to sell new units to fund its renewable drop downs.

In other words, the YieldCo's ability to purchase NextEra's solar and wind projects is somewhat at the mercy of fickle equity markets. Should the unit price of NextEra Energy Partners decline significantly (such as in a bear market), then it might not be able to finance all of the parent company's massive renewable power growth ambitions.

Finally, it's worth mentioning that NextEra Energy has struck out on a couple of large acquisition attempts in recent years. In July 2016, the company ended its $4 billion bid for Hawaiian Electric after state regulators nixed the deal. In 2017, NextEra's $18 billion bid for Texas utility Oncor Electric Delivery was blocked by regulators.

It's a little surprising that a relatively fast-growing utility like NextEra Energy would be so interested in pursuing acquisitions. One reason could be that management wants to maintain a high mix of earnings from regulated activities, which are viewed more favorably by the credit rating agencies and therefore influence the firm's cost of debt.

As NextEra's renewables projects continue to grow significantly over the next decade and beyond, more of the firm's profits could be driven by unregulated activities, which are inherently riskier despite their long-term electricity supply contracts.

Management says the company has $5 billion to $7 billion of balance sheet capacity today due to its current credit ratings, so it's possible NextEra pursues another large deal for a regulated utility.

For now, management deserves the benefit of the doubt and seems very unlikely to take any drastic actions that could jeopardize the company's streak of paying uninterrupted dividends for more than 20 consecutive years.

Closing Thoughts on NextEra Energy

Regulated electric utilities can be a source of generous, secure, and growing dividend income. That's why they are often a staple in the portfolios of low-risk investors.

NextEra Energy does not offer as high of a yield as most of its peers, but its long-term dividend growth rate is two to three times as fast. The company's hybrid exposure to predictable regulated activities and the booming renewable energy space should help fuel solid income growth over the years ahead.

While there are some long-term uncertainties with clean energy (and unregulated activities in general), NextEra Energy is a standout utility. The company's diversified mix of cash flow, constructive regulatory relationships (which drive the majority of its profits today), and impressive balance sheet should help it continue evolving with the times and paying a predictable dividend.