Founded in 1909, ABM Industries (ABM) employs over 130,000 people who serve more than 20,000 corporate clients across the U.S. and in more than 20 international locations.

Source: ABM Investor Presentation

Essentially, ABM is a kind of corporate “handy man,” providing outsourced and integrated solutions to a variety of logistical and mechanical engineering needs including: energy solutions, HVAC (air conditioning), electrical systems, lighting, general maintenance and repair, as well as lawn care, janitorial, and parking services.

ABM provides its custom facility solutions in urban, suburban, and rural areas to properties of all sizes - from schools and commercial buildings to hospitals, data centers, manufacturing plants, and airports.

Source: ABM Investor Presentation

The company is currently undergoing its largest-ever corporate restructuring that will result in six main business units organized around ABM's major end markets. Management estimates the firm has a combined potential addressable market of about $310 billion per year in global revenue, which far surpasses ABM's current revenue base of about $6 billion.

Business & Industry (46% of revenue): janitorial and facilities maintenance, parking services.

Technology & Manufacturing (14% of revenue): advanced janitorial services for data centers and factories (clean rooms).

Education (13% of revenue): janitorial and grounds maintenance, staffing solutions.

Technical Solutions (7% of revenue): electrical and HVAC maintenance and repair.

Healthcare (15% of sales): laundry, parking, facilities management for hospitals.

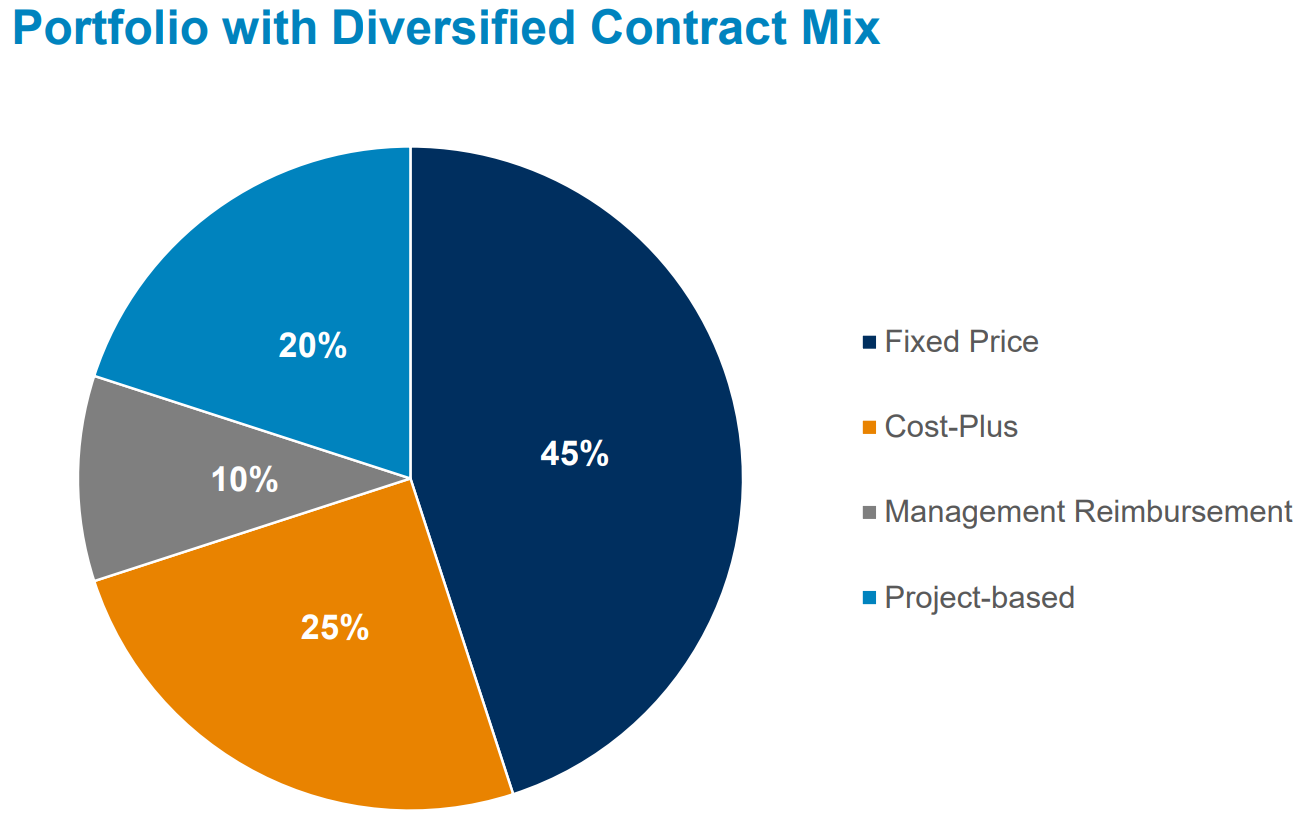

Approximately 70% of the company's revenue is fairly predictable in nature since it is derived from fixed-price or cost-plus contracts. And while the company operates in over 20 countries, 94% of its revenue in 2017 was generated in the U.S.

Source: ABM Investor Presentation

With 50 consecutive years of annual dividend growth, ABM is a dividend king.

Business Analysis

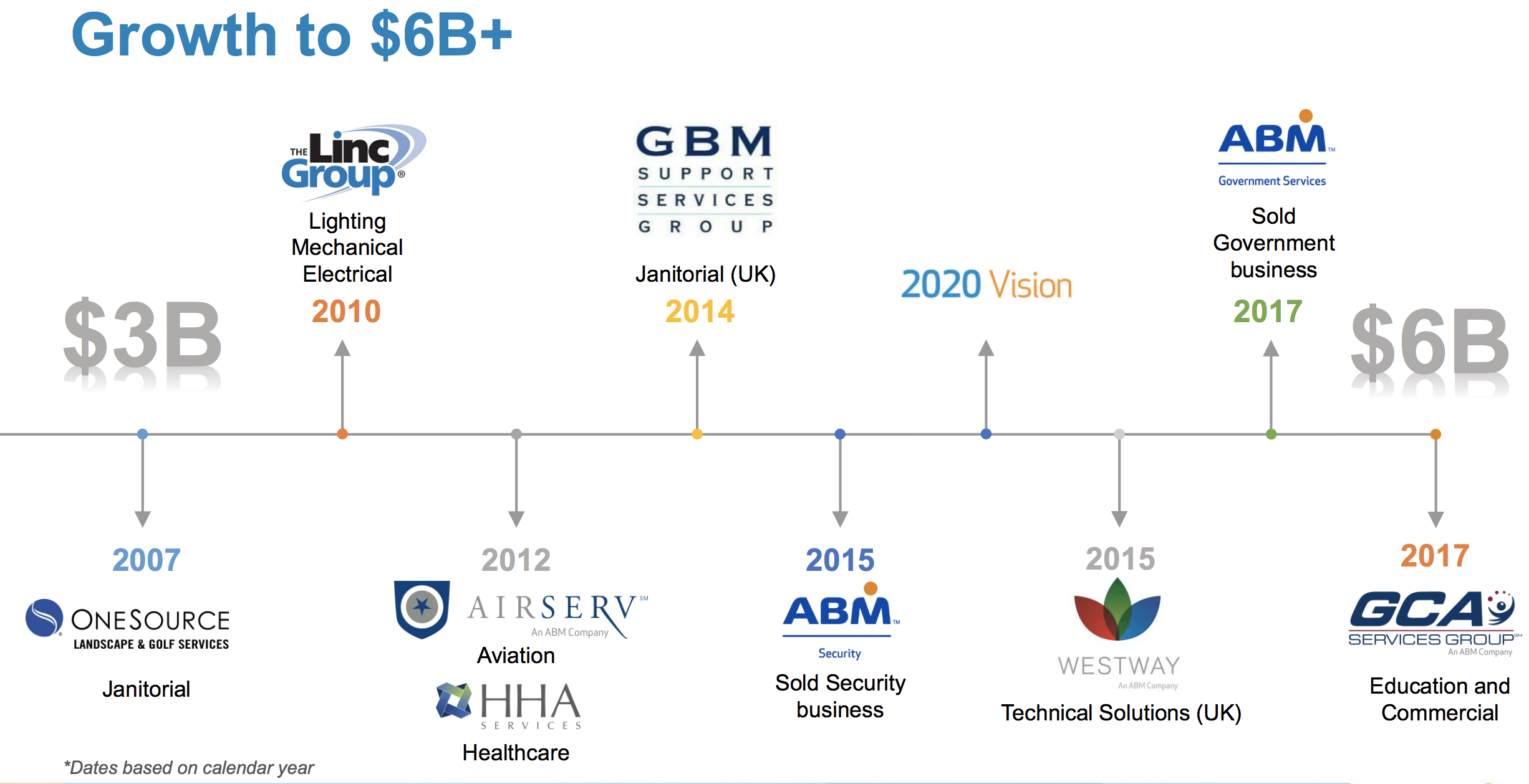

Any company that can deliver 50 straight years of dividend growth needs to be able to generate stable revenue, earnings, and cash flow over time. Thanks to numerous acquisitions over the years, ABM's sales have grown at a rate of about 7% annually over the past decade to double from $3 billion to $6 billion.

Source: ABM Investor Presentation

However, ABM's revenue expansion has not translated into nearly as strong growth in its bottom line. The problem is that the industries in which ABM operates are highly competitive and commoditized, resulting in very low operating margins (the firm's EBITDA margin remained stagnant near 4% during this time).

Simply put, many of the companies ABM acquired over the past few decades turned out to have poor moats and no pricing power. In addition, the company was inefficiently organized with:

14 separate accounting centers

No central procurement (supply chain) structure, including highly inefficient HR policies (caused higher labor costs)

Non-integrated IT departments (from previous acquisitions)

Very poor operating leverage (economies of scale)

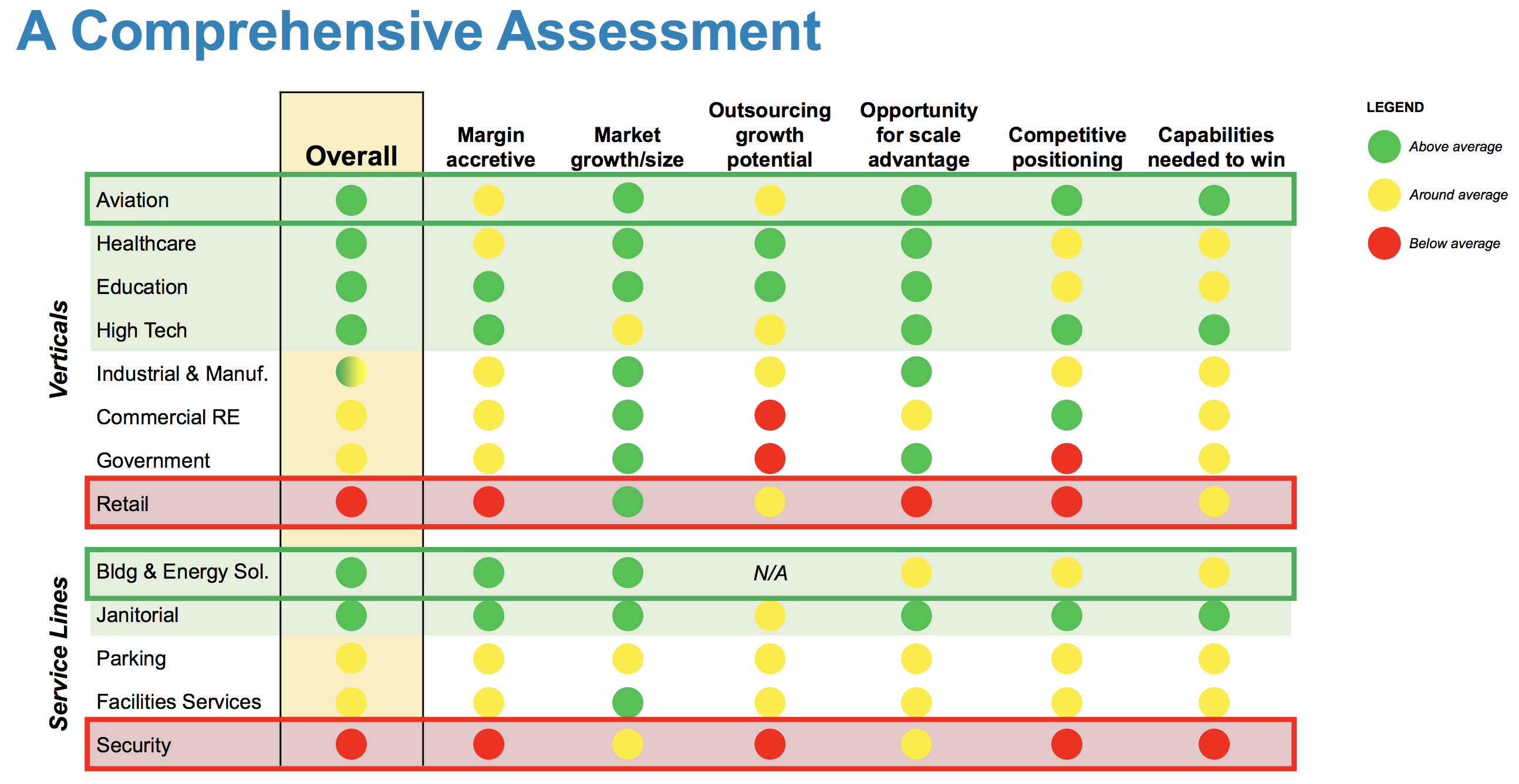

This is why ABM announced the company's largest restructuring ever in 2015, which it calls its Vision 2020 plan. The restructuring plan had three parts. Phase one (completed November 2016) was a careful assessment of the company's businesses, including the numerous bolt-on acquisitions it had made over the past decades.

Specifically, ABM analyzed: the potential market size of each unit, its market share (and pricing power), existing margins, and what its future margins could potentially be. This review led ABM to shut down or sell its security, retail, and government services businesses.

Source: ABM Investor Presentation

Phase two is currently underway and involves an extensive review of the company's operating practices. ABM wants to streamline its supply chain, maximize the productivity of its enormous labor force, and outsource as much of its back office logistics as possible. This involves several strategies:

Accounting consolidated to one center in Houston

One centralized procurement division

Investments in cloud-based IT, including advanced data analytics to streamline cost savings and optimize margins

Revised best practices (new standard operating procedures), including for standardized employee hiring and training

Phase three involves maximizing investments in organic growth initiatives (optimizing marketing) as well as strategic acquisitions to boost the company's market share in the fastest-growing and highest-margin industries in which it operates.

ABM hopes its significant restructuring activities will lift its profitability, which has struggled for many years.

The need for the restructuring is becauseABM has been struggling with its profitability for years. For example, ABM's segment operating margins range from 2.1% for Aviation to 7.0% for Technical Solutions. Ironically, the Government Service business had the highest operating margins at 25.2%. However, due to the highly variable nature of those margins (in 2016 government service operating margin was -20%), ABM sold this unit in 2017.

Management believes that the combined efforts of phase one and two (ongoing) should help stabilize and slightly boost the operating margins of each business segment for 2018. However, note that the company's operating margin guidance for most of its businesses remains below the industry average of 6%.

Source: ABM Earnings Presentation

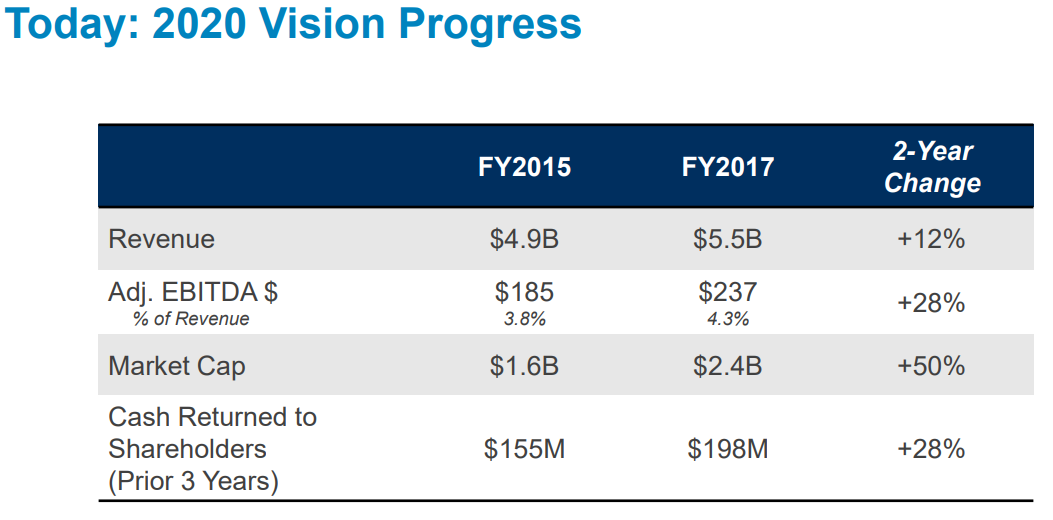

The good news is that while ABM's restructuring progress is slow, the company has been able to steadily move towards its long-term goals. That includes steady growth in its revenue (organic growth guidance for 4.5% in 2018), as well as boost its adjusted EBITDA margin (its preferred profitability metric) by 50 basis points from 3.8% to 4.3% in the last two years.

Source: ABM Investor Presentation

By the time Vision 2020 is complete in three years, management expects to have boosted ABM's adjusted EBITDA margin significantly higher. In fact, thanks to tax reform, management now believes that the firm might achieve a 5.5% adjusted EBITDA margin in 2018 and around 6.5% by 2020, up from 4% in 2015. That would represent about a 70% increase in profitability over a five-year period.

In 2017, as part of phase three of the turnaround plan, ABM bought GCA Services for $1.3 billion. GCA is a provider of maintenance, janitorial services, and grounds management to 3,200 K-12 schools, 80 colleges, and 1,000 commercial clients in 46 states, DC and Puerto Rico.

This was the largest acquisition in the company's history and makes ABM the industry leader in providing facility solutions to the education market. Management expects to see a total of $1.1 billion in additional revenue due to this needle-moving purchase. By 2019 ABM estimates that it will also achieve $20 million to $30 million in cost synergies. That might not sound like much, but for a company that generated operating income of just $110 million in 2017, it is a significant sum.

However, ABM took on $1.3 billion in debt to fund the GCA acquisition, meaning it now has a very leveraged balance sheet. Management expects the leverage ratio (debt / EBITDA) to fall from 5.7 times to 3.8 times by the end of the first full year due to the large increase in cash flow that GCA is bringing.

In the coming years, ABM says that deleveraging via retained free cash flow (free cash flow minus dividends) is its second highest priority, on par with dividend growth. ABM thinks it can bring its debt / EBITDA ratio down to about 2.75 times by 2020 as it executes on its plans. And given the firm's ambitious plans to expand its market share in such large industries, this is a smart long-term strategy.

However, acquisitions and subsequent deleveraging will likely keep dividend growth at anemic levels for the foreseeable future.

Source: ABM Investor Presentation

Overall, it's not hard to see why ABM has been around for so long. The company is larger in size than most of its rivals and can offer customers a wider array of services to win their business. Most of the firm's services are non-discretionary in nature, non-core to clients' core business focus (making them necessary to outsource), and have no viable substitutes.

With a focus on acquisitions, ABM has expanded its range of services, geographical reach, and types of clients over the years, providing a number of growth opportunities.

However, at the end of the day, contracts are usually awarded based on price because the services provided are undifferentiated and commoditized. This will always be a business that generates fairly low margins, despite its longevity and decent cash flow.

Key Risks

First, it's important to understand that ABM operates a very labor-intensive business model (130,000 employees generate $6 billion in sales, which works out to less than $50,000 in revenue per employee). About a thirdof the company's workforce is also unionized, which means there are limits to how much it can reduce its labor expenses.

For instance, the company participates in several multi-employer pension funds that required $63.1 million in contributions in 2017. ABM's pension costs are rising by about 5% per year and could be a drain on its cash flow given the company's extremely thin margins.

And speaking of margins, even if the company manages to boost margins to its 2020 goals, than its profitability will look approximately like this:

Operating margin: 5% (up from 3.2%)

Net margin: 2.5% (up from 1.7%)

Free cash flow margin: 3% (up from 0.7%)

Free cash flow is what's left over after running the company and investing in future growth. It funds buybacks, dividends, and pays down debt. Management expects to grow ABM's revenues to roughly $7 billion by 2020, indicating that it will be generating approximately $210 million in annual free cash flow.

Even though that free cash flow would cover the dividend very well (about a 25% payout ratio assuming 3% dividend growth), ABM is still only going to be retaining about $160 million per year in free cash flow.

This small absolute amount means that ABM likely won't be able to build up significant cash reserves with which to fund medium to large acquisitions. As a result, the company will require large amounts of debt and equity to execute its growth strategy.

And speaking of acquisitions, integrating its largest-ever acquisition (GCA) during the largest restructuring in its history creates execution risks. While GCA provided about 20% growth in revenue, now management will need to ensure it can combined the two large company's separate corporate cultures into one shared vision. In addition, it needs to achieve strong cost synergies if ABM's low profitability is going to improve.

The $1.3 billion in debt ABM took on to purchase GCA also stretched its balance sheet to the limit, so management will need to aggressively deleverage in order to ensure good financial flexibility going forward. As a result, ABM's long-term dividend growth potential will require it to successfully execute on its Vision 2020 restructuring plan.

Specifically, slashing its per unit operating costs, boosting its free cash flow margin significantly, and using all of its retained cash flow to pay down debt very quickly. This means that ABM's dividend growth rate is likely to continue growing at its weak recent figure of 3% for several more years.

In fact, even after the restructuring and GCA integration is complete, it is possible that ABM is going to continue its slow current dividend growth rate indefinitely. That's because ABM's small size means that in addition to debt, it often uses equity (new shares) to fund its acquisitions.

In the last five years, the company's share count has risen an average of 5.6% per year. Each share issued represents an increase in the dividend cost, so if ABM were to continue funding growth through equity at this pace, its dividend costs would rise 5.6% annually even with no increases.

Not surprisingly, management is planning on higher buyback spending in future years. However, it's clear that most of this spending will merely go to offsetting recent dilution, which limits how much money ABM can put towards higher dividend payouts in the short term.

ABM's problem is that it is a small player in highly competitive, fragmented, and commoditized markets. As a result, even if it can achieve far larger economies of scale, the firm will alway struggle to generate sufficient free cash flow to fund its growth organically. In other words, investors are potentially facing an endless stream of large debt issuances, ongoing dilution, increased share repurchases, and slow dividend growth.

Closing Thoughts on ABM Industries

ABM's dividend track record is impressive to be sure. However, ultimately the company is a tiny player in numerous commoditized, no-moat industries. Even if management executes perfectly on its Vision 2020 plan, the most impressive thing about this small dividend king will remain its dividend growth streak and not its growth rate.

With a yield near 2%, ABM is not suitable for those needing immediate income. And with long-term dividend growth potential of just 3% to 6% per year, ABM is also a lackluster income growth stock.

With other industrial dividend kings like 3M (MMM) likely to generate double-digit dividend growth and currently offering a higher yield, there are better alternatives for income investors to consider than ABM.