Target: 47 Consecutive Years of Dividend Increases

Target (TGT) was founded in 1902, but the first discount Target store actually didn't open until 1962. Today, Target is one of America's largest retailers with annual sales of approximately $70 billion and more than 1,800 stores across the country.

Target’s stores focus on convenient one-stop shopping and competitive discount prices, offering a broad range of product categories including personal care, beauty, electronics, apparel, food, furniture, appliances, baby care, movies, and much more. Approximately 33% of Target's revenue is generated from its own private label brands (which enjoy higher margins), and groceries account for about 20% of total sales.

Target’s typical customer is 40 years old, has a median household income of $64,000, and is more likely than not college educated.

The company has increased its dividend for 47 consecutive years, making Target a dividend aristocrat and setting it up to be crowned a dividend king in 2022.

Business Analysis

Target's historical success has been fueled by providing consumers with a wide selection of quality merchandise at very affordable prices, and a convenient, predictable shopping experience thanks to the company's nationwide reach of stores and well-known brand.

As the second largest retailer in the country, Target's economies of scale enable it to negotiate more favorable supply contracts with product manufacturers, keeping its prices low. Smaller rivals are unable to match Target’s pricing, merchandise quality, and breadth of inventory. Consumers are very price conscious and have few reasons to shop at more expensive retailers offering similar merchandise.

Managing such a massive distribution network and supply chain is another major challenge new operators would need to overcome to compete with Target. The company has long-lasting relationships with suppliers that often span decades and has invested heavily in logistics to keep its shelves stocked in a timely manner with relevant products.

When combined with the company's continuous efforts to take costs out of its business, Target is not going away anytime soon. Its stores are in good and improving condition (thanks to ongoing remodeling), it sells needed merchandise across nearly every product category imaginable, and the company is investing to stay relevant in e-commerce.

While e-commerce has been growing faster than traditional retail sales for years, that doesn't mean that brick-and-mortar sales have been in decline. In fact, traditional retail sales have grown by about 2% a year since 2005, along with the U.S. economy and retail sales in general. In other words, fears of a broad-based "retail apocalypse" seem to be overstated today.

With that said, it hasn't been an easy few years for Target, which has seen its sales growth stall and even reverse thanks to some costly missteps.

For example, facing stagnant growth in America, the company launched an ambitious and costly expansion into Canada in 2013. Management pulled the plug on the project in 2015 after major supply chain problems helped generate more than $2 billion in total losses.

Meanwhile, Walmart's $3.3 billion acquisition of Jet.com in 2016, which brought with it founder Marc Lore to run Walmart's vastly expanded online division, gave the company a leg up over Target in online sales. In fact, Walmart's numerous other e-commerce acquisitions (overseen by Lore) have helped drive its own online sales up at a 40+% annualized pace in recent years.

So does that mean that Target is a washed-up has-been, with its best growth days far behind it? Not necessarily. There are still several reasons for some investors to like Target.

First, the company has been investing heavily into omnichannel ("bricks and clicks"), leveraging its U.S. stores as distribution channels for its fast-growing online business, which has increased at least 25% annually for five consecutive years. Thanks to these efforts, Target's same-store sales growth accelerated in 2018 to about 5%, which is quite solid for a traditional retailer this large.

While Target is relatively small compared to Walmart, which has about three times as many U.S. stores, the company still has one of the largest store footprints in the country and a well-developed supply and distribution chain. As previously mentioned, this helps to create economies of scale that allow Target to generate solid margins for a retailer and consistent free cash flow.

In 2017 management outlined a comprehensive $7 billion, three-year turnaround plan that should make Target even more competitive in the future. Target spent $3.5 billion of that $7 billion in 2018 alone (half into online sales expansion), helping boost same-store sales growth to a mid-single-digit pace.

However, there is plenty more work to be done as the company's new strategic plan involves six strategies. First, Target will invest $1 billion into optimizing its supply and logistics chain, which will help it achieve its overall $2 billion cost savings goal (about 2.7% of sales).

Next, the company will focus new store openings on smaller stores located in urban areas. Target had about 130 of these smaller, urban stores in early 2019. City stores in high-density areas represent solid traffic but underserved markets that Target believes represent a opportunity to expand its physical retail presence in the U.S.

Third, Target is planning on upgrading and remodeling over 1,200 stores through 2020. At the end of 2018 Target had already remodeled about one third of its store count (600 locations) in the U.S. Changes include not only focusing on a more upscale look but also initiatives like making separate entrances for shoppers who are in a rush and those who are looking for a more premium, slower shopping experience.

Target's spending on store improvements has nearly tripled from $550 million in fiscal 2015 to over $1.6 billion last year, while investments into improving the online sales platform and logistics chain have more than doubled.

These trends will likely continue as Target shifts from a strategy based on expanding its store count quickly to one that achieves sales growth via strong same-store sales growth created by a more efficient and premium shopping experience both online and in its brick-and-mortar locations.

Increase its sales of groceries and alcohol is another part of Target's turnaround strategy. These categories have proven to be a strong traffic driver in the past, and management has noted that remodeled stores with greater food and alcohol sales typically see a 2% to 4% increase in same-store sales.

Target is also following in the footsteps of Walmart and Costco by investing in higher pay and training for workers. For example, Target has announced plans to raise its minimum wage from $11 per hour in 2017 to $15 by 2020.

Walmart and Costco have both shown that rising labor costs don't necessarily lead to decreased profitability, especially if matched with stronger worker training. This is because better paid and trained workers are more efficient and quit less often, resulting in lower employee turnover and less new employee training.

Target has seen a 60% increase in worker applications since it began raising wages and improving employee training, giving it greater access to a more diverse and high-quality workforce. A better workforce also tends to result in higher customer satisfaction by creating a more pleasant shopping experience that can help build brand loyalty.

Further helping those brand loyalty efforts is the company's continued growth of its RedCard program, in which customers who obtain the company's branded credit card get a 5% discount on all purchases. RedCard currently accounts for about 20% of Target's sales, and management has found that RedCard members tend to spend about twice as much as non-members. To further boost RedCard participation Target is offering free 2-day shipping on orders over $35 for the loyalty program's participants.

Management is also doubling down on its use of private label brands that are exclusive to Target, trying to create another reason for consumers to choose it over its rivals. Essentially, Target is trying to solidify its status as a more upscale Walmart and maintain its focus on higher-margin apparel and home products.

However, the biggest and most important strategy Target has to return to growth involves its omnichannel initiatives. This means incorporating online shopping and apps into customers' experiences in order to maximize convenience and keep shoppers from choosing Amazon or Walmart.

On this front, Target launched its Cartwheel online shopping app and has a drive-up delivery option in which consumers can order online, drive up to a designated parking spot, and have an employee deliver their order without ever having to leave their vehicle. By the end of 2018 Target was offering in-store online sales pick up (which it calls Drive-Up) at over half of its total locations.

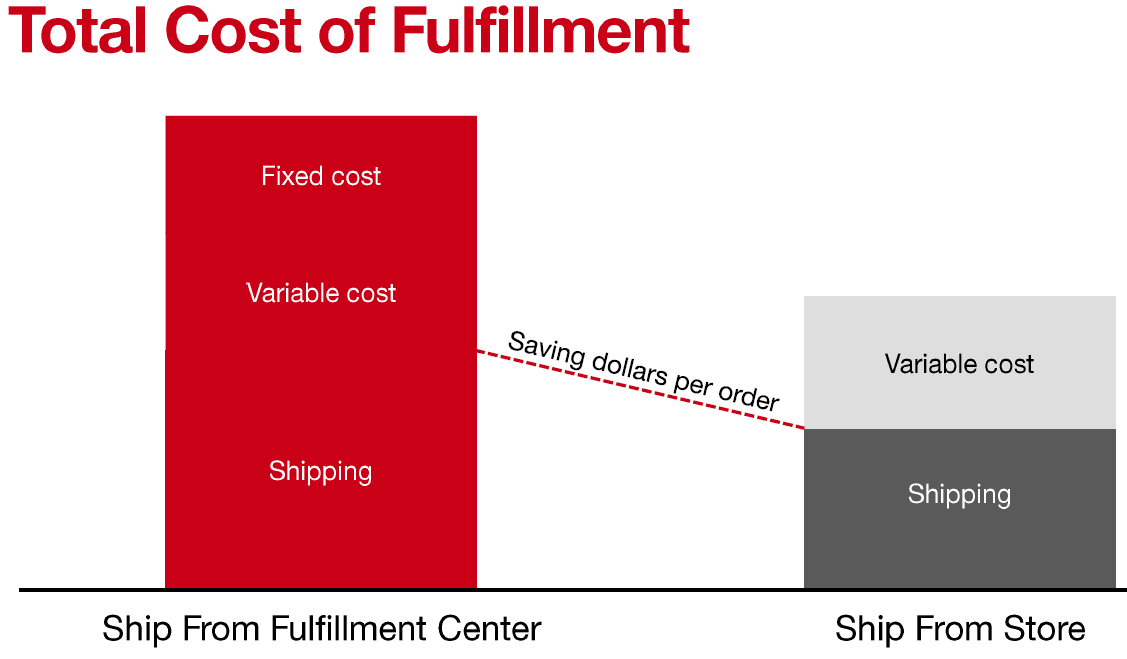

Using its U.S. store base as a hub for online sales fulfillment is crucial to management's omnichannel growth strategy. According to the company, fulfilling online sales through its stores results in about 33% lower costs than from a dedicated fulfillment center, thanks to leveraging existing assets. In addition, stores that have been adapted for online in-store pickup also need to hold less inventory, resulting in higher efficiency.

Source: Target Investor Presentation

Like Walmart, Target is also investing heavily in acquisitions to improve its chances of becoming a leading name in e-commerce for many years to come. In 2017, for example, the company acquired Grand Junction, a transportation technology company that helps Target offer local same-day delivery, which is increasingly important in e-commerce.

In December 2017 Target made an even bigger bet on omnichannel via its $550 million acquisition of Shipt. Shipt has built a nationwide network for same-day delivery of groceries, essentials, home, and electronic goods. By the end of 2018, Shipt had expanded to 250 U.S. cities covering nearly 67% of the American population.

The bottom line is that Target has been around for more than a century and has proven itself highly adaptable to changing consumer tastes and industry challenges. While it's a latecomer to the world of omnichannel, the company's turnaround plans and recent e-commerce acquisitions show potential in restoring Target's business to a path of sustainable growth.

That being said, while management is busy making moves to stay relevant, there are big challenges ahead for Target in the increasingly competitive world of retail sales.

Key Risks

Arguably the biggest risk facing Target is whether or not the company can continue generating sustainable earnings growth over the long term.

While Target is making all the right moves in terms of investing heavily into omnichannel and improving worker retention, these are not necessarily going to result in strong earnings and dividend growth. After all, Target is merely doing what all retailers must to survive in a future world that will be increasingly dominated by e-commerce.

For example, while Target's $15 per hour minimum wage target by 2020 represents a 36% increase from 2017's levels, in 2018 Walmart's average worker pay hit $14.01, and Amazon already raised its minimum pay to $15 at the end of 2018.

In other words, Target's increased investments in its workforce are simply table stakes that all smart retailers are doing, not a competitive advantage that is likely to accelerate the company's growth in the future.

That's because Target became a giant by filling the suburbs of America with 130,000 square-foot boxes. Growth in this industry is possible by adding new store locations and increasing sales at existing stores.

In the age of Amazon, it's hard to argue that America needs more big-box retailers. Target has faced reinvestment challenges over most of the last decade, as demonstrated by its lackluster pace of new store openings.

Note that the increase in store count recent years is driven by the rollout of its smaller urban stores, which don't have the same total revenue generating capacity as its large suburban stores. Target's total retail square footage has continued declining despite opening more locations.

Source: Target Annual Reports, Simply Safe Dividends

Going forward, new store openings seem unlikely to drive any significant rate of revenue growth. In other words, Target's key growth driver of the past is now likely gone for good. Instead, the firm will have to mostly drive revenue growth via strong same-store sales, led by continued success in digital sales.

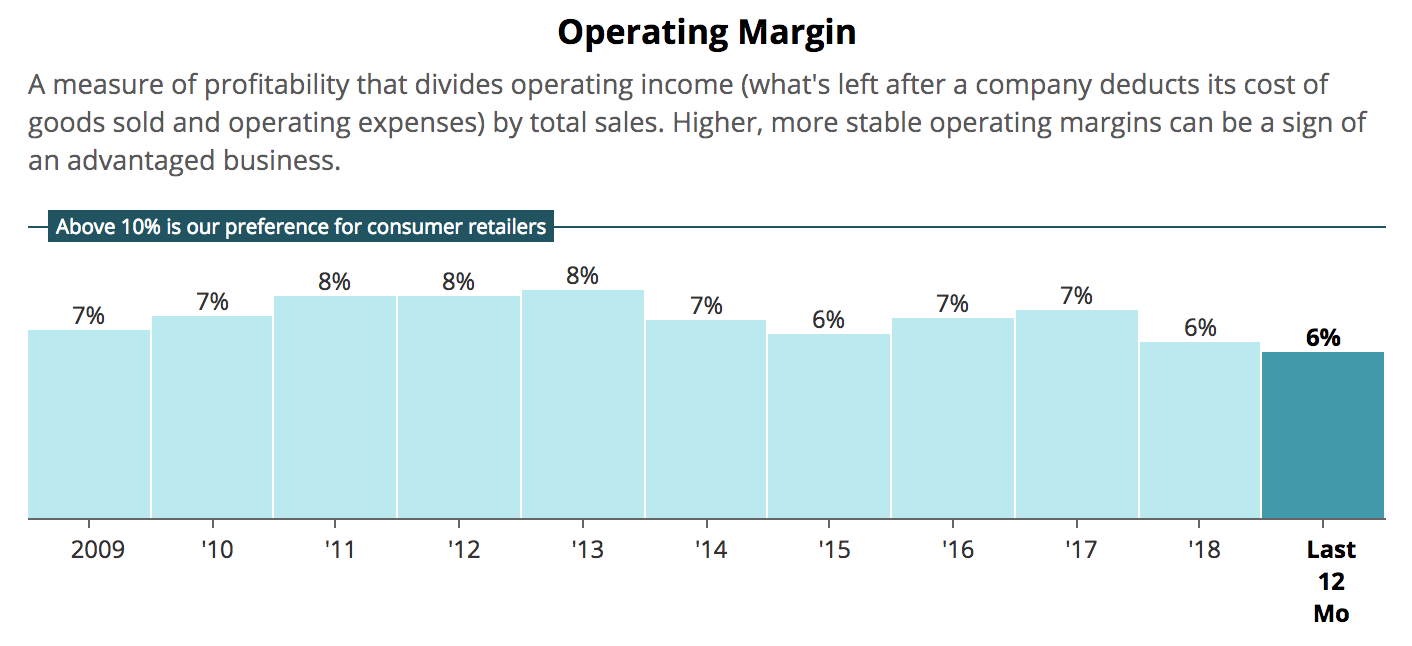

However, according to CFO Cathy Smith, Target's investments, including into a more efficient supply chain and in-store pickup and online delivery, are only going to stabilize and maintain margins over time.

Basically, Target's future online sales growth will likely continue pressuring margins in the next few years (see below), but even after those investments are complete, the boost from omnichannel will only offset the lack of strong growth from store expansions.

Source: Simply Safe Dividends

While Target's online sales growth is impressive (nearly 50% in late 2018), its revenue base still badly trails industry e-commerce giants like Amazon (over $60 billion in U.S. online sales) and Walmart (over $20 billion in online sales). As a result, it will probably take a very long time for online sales to contribute positively to Target's profitability and earnings since Walmart says it is still losing money on e-commerce sales and Target's digital sales ($4 billion in the last 12 months) are nearly six times smaller.

Target also lacks an international presence. As a result, the company's future growth potential could be more limited compared to peers like Walmart and Amazon, which have strong and fast-growing business units overseas.

Furthermore, keep in mind that Target's sales are likely to be more cyclical than its peers over a full economic cycle because it has relatively small exposure to groceries, which make up just 20% of sales. Groceries, while low margin, are usually a strong traffic driver because they allow a store to become a "one-stop shop" that allows consumers to save time by buying everything in one place.

Thanks to a relatively low grocery mix, Target's same-store sales declined about 5.5% during the Great Recession, showing that its more discretionary business model is more sensitive to the health of the U.S. economy than Walmart's. For comparison, Walmart's same-store sales grew 1.6% in 2008 and 3.5% in 2009, as groceries accounted for roughly half of its revenue at the time (and around 65% today).

Going forward, it may not be easy for Target to win market share in the grocery business, which continues to get more competitive. Not only did Amazon's purchase of Whole Foods trigger a price war with Walmart and Kroger (KR), but low-cost grocers such as Aldi and Lidl are both planning on opening more than 1,000 stores in the U.S. In fact, by 2022 Aldi plans to become the third biggest grocer in the U.S., thanks to ramping up its store count to 2,500 via a $5.3 billion investment effort.

What about Target's success in competing with Amazon Prime and Pantry? While Target is offering some of the same benefits as Prime but without an annual subscription, it's important to remember that Prime has some key advantages that Target still lacks.

For example, Target's online inventory includes "hundreds of thousands" of items, according to the company. Amazon offers about 100 million items for sale that can be delivered in as fast as an hour in certain markets. In addition, Prime has dozens of benefits (such as music streaming and Prime video) while Target's RedCard program offers nothing but free shipping and a 5% discount on Target merchandise.

Basically, while Target has made great strides in competing with Amazon, it isn't close to being a market leader in the industry, and likely never will be. Amazon's cloud business (Amazon Web Services) is an enormous, fast-growing business throwing off gobs of cash that allows that company to invest in offerings and services that Target's business model will never be able to match.

As a result, Target's earnings seem likely to grow more slowly than in the past and force management to grow the dividend at a pace that many investors might find unsuitable. For example, Target has grown its adjusted EPS by 7.2% annually over the past 20 years. Thanks to payout ratio inflation (EPS payout ratio has more than doubled over the past decade) Target was able to reward dividend investors with 14% average payout growth over the past two decades.

But that slowed to 10% annual growth over the past five years, and the most recent dividend hike was just 3%. With Target having to invest more heavily into online sales channels (not to mention higher pay, worker training, store remodels, and improving the supply chain), it's likely that the company will follow Walmart's lead and hike the dividend at a steady but slower low single-digit rate for the foreseeable future.

While Target has a great track record of adapting over the past 116 years and has earned its status as a safe dividend investment, the company has a lot to prove when it comes to its future dividend growth potential.

Closing Thoughts on Target

Target has paid uninterrupted dividends every year since it went public in late 1967, and the company's impressive payout growth streak seems very unlikely to end anytime soon.

With that said, consumer retail is one of the most challenging industries to do well in. Low margins, ferocious competition, and periodic technological disruption mean that investors need to be very selective in this space. There is a reason why we have chosen to avoid investing in almost all of the retail sector – the rapidly-changing consumer landscape is just too hard to get in front of.

Target's online sales-focused turnaround plan is certainly showing some traction. However, it will keep some pressure on short-term dividend growth as the company invests more cash flow back into these initiatives.

More importantly, it will likely take years to assess whether or not management's actions will help Target find sustainable earnings growth in a very saturated retail market, especially as it battles against e-commerce giants that benefit from lower operating costs and even larger economies of scale.

Mass merchandise stores seem likely to always be relevant for a number of consumers, but it’s hard to imagine their slow bleeding and struggle to find sustainable sources of profitable growth will cease any time soon.

We prefer to invest in companies that seem likely to become larger and more profitable over the next 5 to 10 years. Target doesn't seem to fit that mold, even despite its secure dividend and rich history. Investors considering Target should maintain a high bar given some of these long-term uncertainties and the stock's decdelerating dividend growth rate.