Reviewing IFF's $7 Billion Acquisition of Frutarom

Many companies grow through acquisitions, but Wall Street is often skeptical of big deals given the risks involved.

In May 2018, International Flavors & Fragrances (IFF) announced it was buying rival Frutarom in a $7.1 billion cash-and-stock deal. Given that IFF's market cap at the time was just over $12 billion, this qualified as a big acquisition.

Investors didn't like it. IFF's share price fell over 10% on the news, causing some dividend growth investors to worry about what this merger might mean for the company's long-term outlook.

The acquisition will finally be reflected on IFF's books when it reports earnings later this week, so let's take a look at whether or not this deal seems to makes sense for IFF and how it affects the firm's dividend safety and growth profiles.

Why IFF Bought Frutarom

Even before buying Frutarom (the deal closed in October 2018) IFF was an industry heavyweight, selling over 40,000 flavors and fragrances used in beverages, baked goods, prepared foods, oral care products, soaps, detergents, lotions, lipsticks, deodorants, perfumes, and more.

IFF sold to 3,000 customers in 162 countries and was one of the top four companies in its industry. Buying Frutarom makes IFF the second biggest company in its industry.

Source: IFF Merger Presentation

IFF's CEO Andreas Fibig explained the acquisition saying:

"Together, IFF and Frutarom will have a broader customer base, more diversified product offerings and an increased market penetration. We will instantly become a leader in natural solutions. We will also strengthen our exposure to fast-growing small and mid-sized customer accounts, gain new opportunities in attractive and fast-growing adjacencies and enhance our global reach.

We also anticipate cost synergies through raw material harmonization, footprint optimization and streamlining overhead expenses. Additional cross-selling opportunities and integrated solutions are expected to provide revenue synergies to our shareholders over time."

Two of the most compelling parts of this deal are Frutarom's focus on healthier ingredients and smaller customers. About half of IFF's revenue is generated from large multinationals such as Nestle and General Mills. In recent years, many of these large consumer staples companies have encountered growth challenges as their customers opted for healthier, more natural offerings rather than processed foods with artificial flavors, colors, preservatives, and sweeteners.

IFF previously stated that over half of all new flavor briefs it worked on called for natural solutions and that it has a higher win rate in this area, so the company appeared to be adapting its portfolio for this trend. Buying Frutarom helps solidify IFF's future in these critical growth areas of the future.

Frutarom has a leading natural ingredient portfolio, which accounts for 75% of its revenue. Natural colors, natural food protection, natural savory solutions, and health ingredients are all part of its business. As you can see, these "on trend" areas are growing twice as fast as IFF's core fragrance and flavors markets.

Source: IFF Merger Presentation

With Frutarom under its wings, IFF can offer an even more comprehensive portfolio of solutions, hopefully increasing its win rate and the average amount of business it does with each customer.

Speaking of customers, IFF's customer base also expanded from about 3,000 companies to more than 30,000 as a result of this deal. In business since 1933, Frutarom has developed relationships with many small, mid-sized, and private label companies, which generate 70% of its revenue.

Source: IFF Merger Presentation

These local and regional firms are the companies causing the most headaches for many global food and beverage manufacturers. Their upstart brands, simpler ingredients, and nimbler operations are helping them take share across many food and beverage categories, benefiting Frutarom's business.

By purchasing Frutarom, IFF further diversified its customer base by increasing its focus on these faster-growing customers. And like IFF, Frutarom also conducts a lot of business in emerging markets, which accounted for 43% of its overall sales.

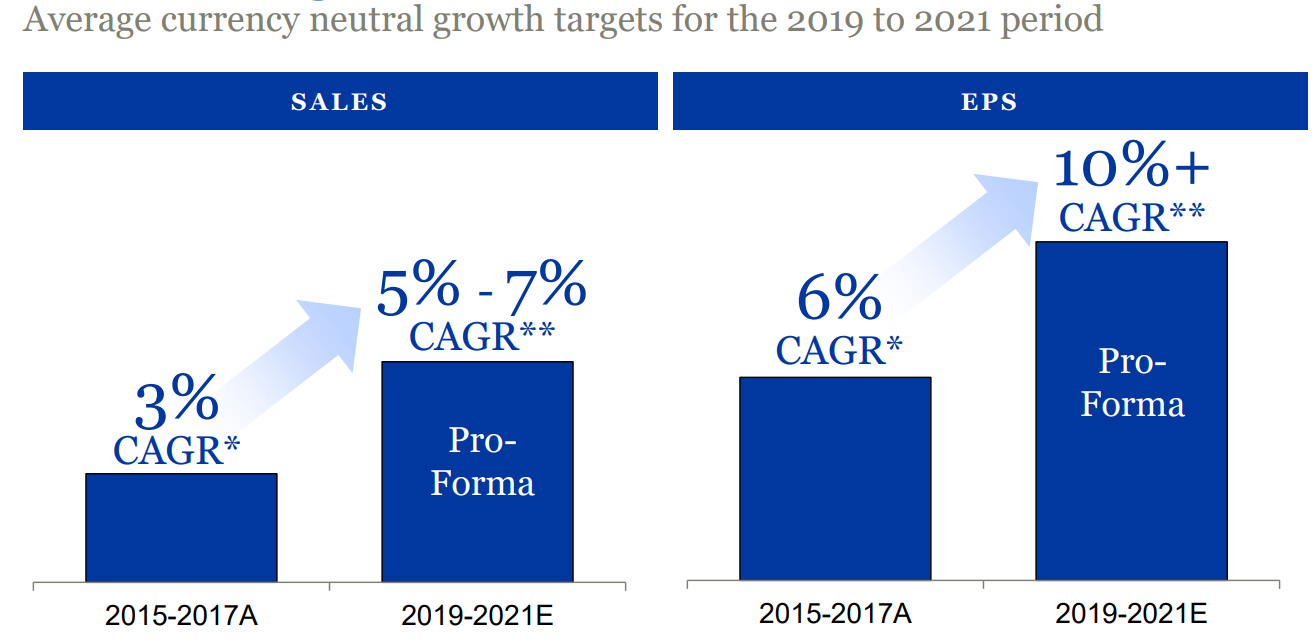

Going forward, management is optimistic that the faster-growing Frutarom, which accounts for 32% of the combined company's revenue, will help IFF improve its sales and earnings growth rates in the years ahead.

Source: IFF Merger Presentation

So if this deal has solid strategic appeal, then why did Wall Street react so negatively when it was announced? As with all major acquisitions, IFF faces several risks related to its purchase.

Risks With The Deal And What They Mean For Dividend Investors

No matter how great a company might be, paying too high a price is never a good idea. IFF paid steep valuation multiples of 5.2 and 26.5 times Frutarom's 2017 revenue and adjusted EBITDA, respectively, indicating it may have overpaid for the largest deal in its history.

Furthermore, between 2002 and 2013 IFF focused on organic growth with no acquisitions at all, and since 2014 it's only made small bolt-on deals. In other words, this mega-deal marks a major departure from management's long-term strategy, which could further increase the risk of something going wrong.

For example, IFF may fail to realize the expected $145 million of annual cost savings the combined company targets. Given the high price management paid for Frutarom, management is banking on meaningful cost synergies and cross-selling, but it will take several years to gauge traction. After all, combining two large companies' manufacturing bases can be a costly and time-consuming endeavor.

Source: IFF Merger Presentation

Importantly, an acquisition of this magnitude usually means a lot more debt on the books, which can decrease a company's dividend safety and future growth rate. IFF took on $3.1 billion of new debt financing to pay for Frutarom, nearly tripling its debt load.

IFF now prioritizes deleveraging over all other uses of capital with the dividend the lowest priority. "Maintain dividend status" likely means a dividend freeze, which will break the firm's 16-year dividend growth streak.

Source: IFF Merger Presentation

IFF's payout ratio has increased over the last decade, driven by fairly aggressive dividend hikes (14% average annual growth over the last five years). Holding the dividend steady and suspending share repurchases maximizes the amount of retained cash flow management will have available to pay down debt.

Source: Simply Safe Dividends

IFF's higher leverage caused by the Frutarom acquisition resulted in S&P downgrading the company's credit rating one notch and Moody's by two notches. IFF's credit rating is currently BBB with a stable outlook stable from S&P and the equivalent of BBB- from Moody's. BBB- is the lowest a rating can fall and still be considered investment grade.

"The downgrade reflects the substantial increase in leverage and subsequent weaker credit metrics following the expected close of the transaction as well as the challenges of integrating a large-scale transformative acquisition...The stable outlook recognizes the strategic rationale for the acquisition as well as the publicly stated commitment from management to maintain an investment-grade rating and restore credit metrics to more appropriate levels for the Baa3 rating over the next 18-24 months."

Moody's estimates the company's debt/EBITDA ratio will jump from 2.6 to 4.7 and that management will get that ratio down to 3.0 or less within 18 to 24 months.

However, even with much higher sales and aggressive cost-cutting planned, all of the company's retained free cash flow will have to go to paying down debt in order to maintain IFF's investment grade credit rating.

Ultimately, IFF's dividend is likely to remain safe but grow much slower (or be frozen) for at least the next two or three years. The Frutarom acquisition will appear on IFF's books when it reports fourth-quarter earnings on February 13. Due to the anticipated increase in financial leverage, IFF's Dividend Safety Score was downgraded from the 90s (Very Safe) to 65 (Safe).

The firm's Dividend Safety Score will improve as management makes progress on its deleveraging efforts. However, if IFF experiences any headwinds that pressure its cash flow and ability to quickly deleverage, its dividend could find itself in the crosshairs if more drastic actions are needed to maintain the company's investment grade credit rating. For now, that seems unlikely, and management deserves the benefit of the doubt.

Closing Thoughts on IFF's Acquisition of Frutarom

IFF's purchase of Frutarom looks attractive from a strategic sense, but management appears to have paid a steep price for future growth. As a result, the company's dividend seems likely to remain safe, but it will probably be frozen for a few years until IFF can pay off the high amounts of debt it used to fund this deal.

How quickly IFF can return to dividend growth will depend on management executing well on integrating Frutarom and realizing the deal's expected cost and revenue synergies.

Investors will want to watch the company's debt level and cash flow generation closely in the coming years, but ultimately the larger and faster-growing IFF has good potential to be an even stronger dividend growth stock in the future.