Founded in 1947 in New York City, Franklin Resources (BEN) is the 34th largest asset manager in the world. The firm's 9,000 employees (including about 650 investment professionals) manage over $730 billion in assets for a client base located in more than 170 nations around the globe.

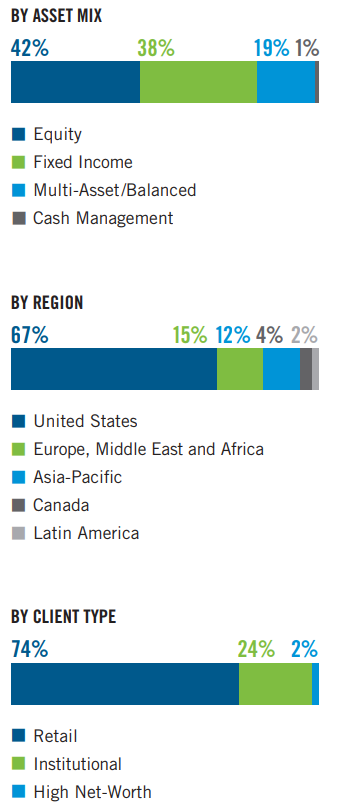

Franklin Resources is almost a pure play active management firm, with about two thirds of its business coming from the U.S. and a primary focus on providing equity funds (42% of assets under management):

Source: Franklin Resources Investor Presentation

The vast majority of its business is with retail investors, specifically through their 401Ks and IRAs. Only 26% of Franklin’s clients are institutional (pensions, insurance companies, endowments, sovereign wealth funds) or high-net worth individuals who are utilizing its alternative asset management (hedge fund) services.

Business Analysis

Theoretically, asset management is the perfect business model for dividend growth investors.

After all, it’s a capital light industry that is highly scalable. Relatively small fixed overhead costs can be amortized over vast asset bases, resulting in very fat margins as an asset manager’s business expands.

For example, asset managers spend almost nothing on capital expenditures with Franklin spending just $75 million in fiscal 2017 (1.2% of revenue). Instead, these companies manage investments for others and charge fees as a percentage of assets under management. Franklin's average fund fee ranges from 0.15% for cash management to 0.5% for global equity mutual funds. In 2017, about 69% of the firm's revenue was generated from such fees.

Another benefit for asset managers is that the stock market historically rises over time (9.2% per year since 1871). As a result, investment managers enjoy a natural catalyst to grow assets under management and thus increase their fees over time.

In addition, while the mutual fund industry is a fairly easy one to break into (there are thousands of funds in the U.S. alone), fund assets have historically been quite sticky. For example, over the last 30 years approximately 70% of a fund's assets have remained parked in a fund over time. This is because investors are usually not very interested in changing funds unless performance drastically deteriorates over a prolonged period of time.

Meanwhile, the number of new employees needed to manage new assets grows much slower than the assets themselves, meaning that investment managers can have very high profitability as they increase their scale. For instance, Franklin currently enjoys a free cash flow margin north of 20%.

In terms of competitive advantages, the asset management business is built around trust, reputation, and strong distribution networks. Franklin Resources, having been around for over 70 years (and led by the son of the founder), has established itself with three major fund lines: Franklin, Templeton, and Mutual Shares. The firm has also developed good relationships with financial advisors, who drive clients and their assets into Franklin's funds.

Scale is another important factor in this industry. That's because in order to grow its geographic and product reach, Franklin must investing substantially in human capital, specifically researchers, analysts, and portfolio managers.

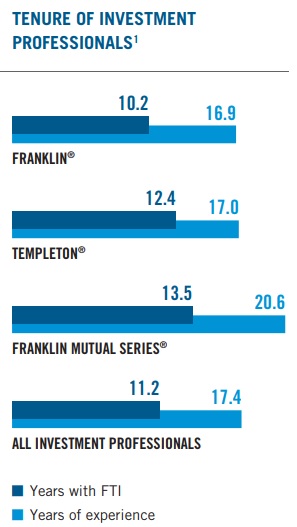

Franklin has the large scale necessary to hire and retain some of the top talent on Wall Street and around the world. This is why its average fund manager has over 10 years of experience with the company and nearly 20 years in the industry. Meanwhile, top executives at the company have between 25 and 30 years of industry experience.

Going forward, the company is focused on two major growth avenues. The first is ETFs, or passively managed investments. In 2016, Franklin jumped on the ETF bandwagon and now has38 ETFs under the LibertyShares brand name. It has also launched several smart beta ETFs, which track proprietary indexes based on factors that have historically proven to generate market beating returns such as: value, dividend growth, smaller size, low volatility, and higher than average returns on capital. BlackRock expects smart beta ETFs to represent a $1 trillion industry by 2020.

The other major growth catalyst lies overseas, where the company has been expanding its operations and advisor distribution network in countries like South Korea. International markets, especially emerging markets such as China and India, have enormous populations, fast-growing economies, and enormous potential as their large middle classes become richer and need a trusted company to manage their wealth. For instance, in 2020 it's estimated that China's middle class will number 600 million, or nearly double the entire population of the U.S.

However, despite all the theoretical positives facing this industry, analysts expect Franklin to have pretty much flat revenue growth over the next few years. In other words, Franklin's strong track record of fast dividend growth could be coming to an end as the company faces numerous structural industry trends and challenges that might mean it's not necessarily a good long-term investment.

Key Risks

While Franklin's business model makes it a great dividend growth stock in theory, the reality is not nearly so sunny. That's because the industry is monstrously competitive with over 11,000 mutual funds in the U.S., and more than 110,000 operating overseas. This high level of competition has resulted in two major problems for Franklin in recent years.

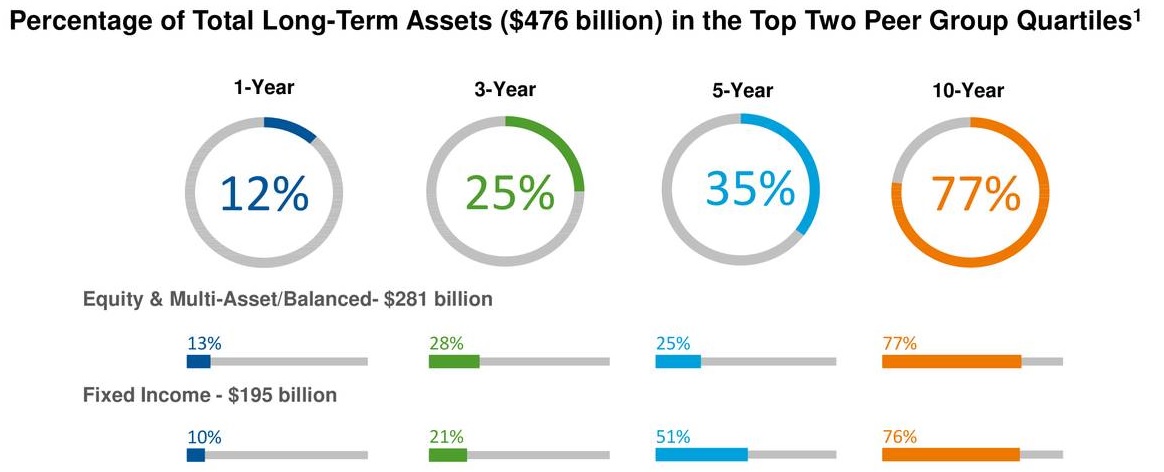

First, the firm's own funds, which have historically delivered above average performance, have struggled in a world awash in cheap capital, making it harder to outperform the army of rivals it faces both in the U.S. and abroad.

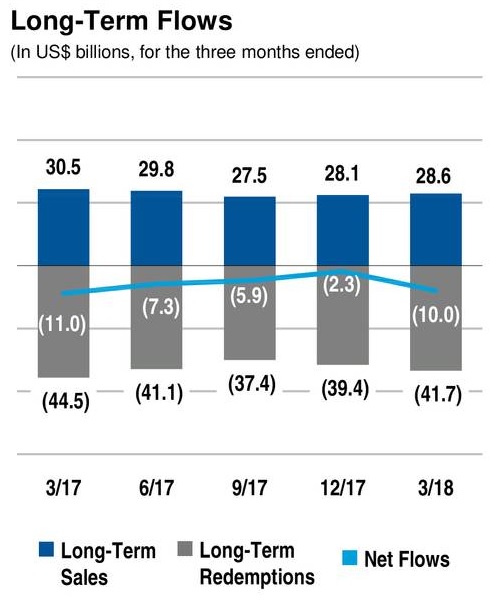

For example, 75% of the company's funds had performance in the top 50% of their respective fund types (stocks, bonds, etc) over the last 10 years. However, in recent years that figure has collapsed, with just 13% of Franklin's equity funds beating most of its peers in the last year, and just 10% of its bond funds doing the same. This has resulted in a continued flight of assets under management as more investors move their money to other funds.

Source: Franklin Resources Earnings Presentation

Those outflows are being seen in every fund type: equities, bonds, U.S., International, and institutional.

Source: Franklin Resources Earnings Presentation

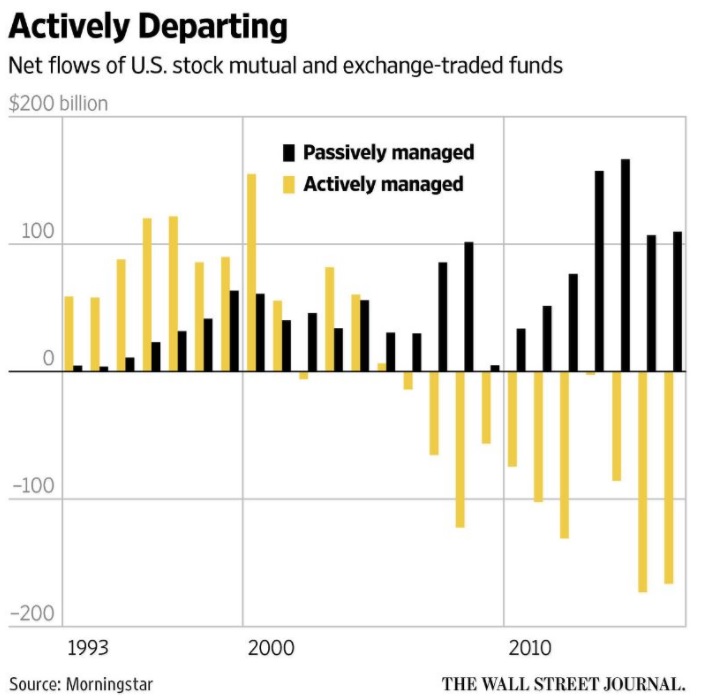

The other major risk to Franklin has been the major secular shift away from active funds to passive ones, such as index mutual funds and ETFs. Starting around 2005, investors began to stampede to passively managed funds as they increasingly realized that low costs are the best way to maximize long-term returns.

This has hurt Franklin in two ways. First, the company has historically been mostly focused on active mutual funds, which are now out of favor. And while the firm has been attempting to launch its own passive ETFs, here too it faces enormous competition. For example, in mid-2017 there were 1,756 ETFs in the U.S., and 5,024 around the world, according to research firm ETFGI.

Worse still, the industry is dominated by just a few large first movers, with the top 20 ETFs claiming 51% of total net industry inflows in 2017. Passive asset management is dominated by Vanguard and BlackRock (BLK), which run the best known and largest ETFs (BlackRock runs iShares ETFs).

Blackrock, the world's largest asset manager with $6.3 trillion in AUM, commands 37% of the $4.6 trillion ETF market. And the top three and five names in the space command 70% and 90% of the market, respectively. The passive fund world is dominated by highly commoditized products that pretty much all track the same indexes, meaning that they compete on price.

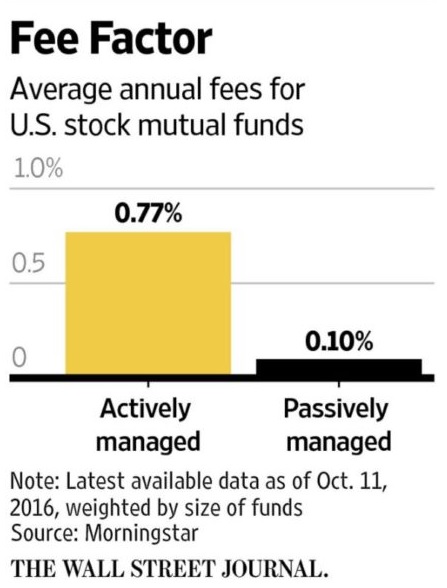

While Franklin is a strong player in active funds, it simply lacks the scale and brand power to compete against rivals who are offering passive investments with expense ratios below 0.05% in some cases. Which brings us to another major problem for Franklin.

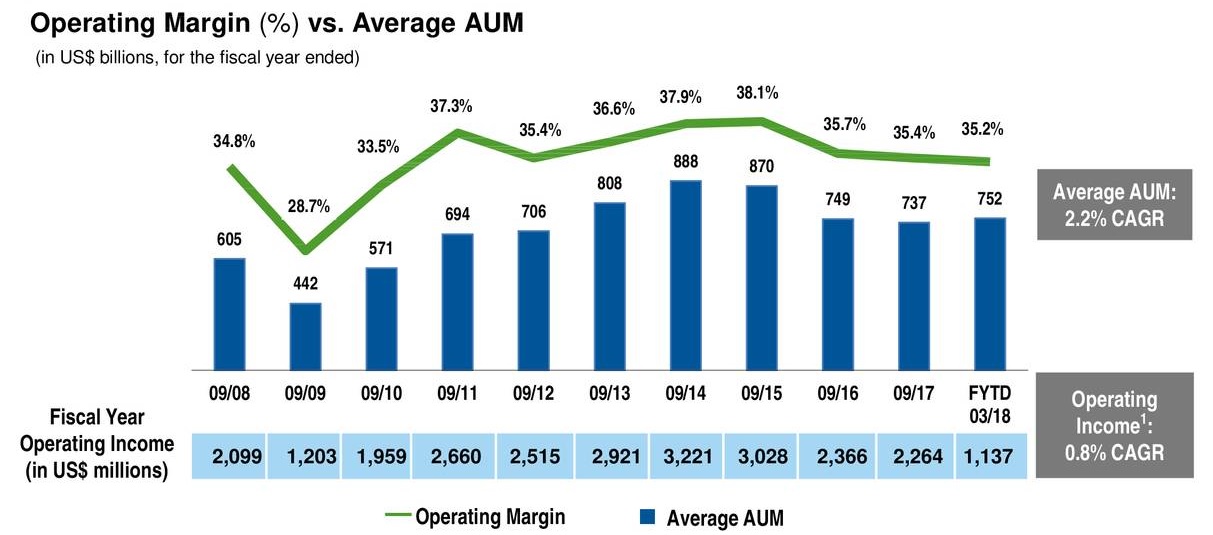

Despite the stock market experiencing the second longest and strongest bull market of all time since the financial crisis ended in 2009 (S&P 500 up nearly 300%), Franklin's assets under management have grown at a paltry 2.2% over that time. The company has seen a continuous stream of net outflows since 2014 that have caused its asset base to actually shrink by 15% since then.

Source: Franklin Resources Earnings Presentation

To help slow the bleeding, Franklin has been cutting the expense ratios on its funds while simultaneously investing in new products (passive and smart beta ETFs), international funds, and improved data analysis (for research staff).

However, because of the turmoil in the industry, Franklin has also been forced to pay more to its top analysts to keep them from jumping ship to rival firms (compensation costs up 7% in the past year). Meanwhile, IT spending is up 6% in the past year. All told, Franklin's operating margin has been declining since 2015. And given that the secular trend of increasing passive investment popularity and falling active fund fees is unlikely to stop anytime soon, there is little hope that Franklin can see its profitability improve in the short term.

In fact, analysts expect Franklin's entrance into new markets (international, ETF, smart beta funds) to merely allow its revenues to remain flat over the coming years. Long-term earnings growth is expected to mostly come from high levels of share buybacks.

Overall, Franklin's biggest risk is that its fundamental business model (active mutual funds) has been permanently disrupted, and so far it has shown itself to be unable to break into the future of the industry (passive funds) in any meaningful and profitable way.

Closing Thoughts on Franklin Resources

Franklin Resources has an impressive pedigree and track record as a dividend aristocrat. Over the past decades, the firm has generated safe and growing dividends in all manner of economic and industry conditions. Thanks to a low payout ratio and cash flow-rich business model, this is likely to continue for the next few years at least.

That being said, Franklin Resources has achieved its previous success by becoming one of the largest and most trusted names in active mutual funds, an industry that is currently in turmoil. The secular trend away from higher cost (and usually underperforming) active funds means that Franklin's sales and margins are likely to continue to struggle for the foreseeable future.

Therefore, while Franklin Resources continues to pay a safe dividend, its future payout growth potential has been deeply impaired. For investors looking to cash in on the attractive economics of the asset management industry, actively managed funds with superior performance track records (e.g. T. Rowe Price) or companies focused on passive ETFs (e.g. Blackrock) may be better options.