United Parcel Service: Uninterrupted Dividends Since 1969

Founded in 1907 by two teenagers making retail deliveries, United Parcel Service (UPS) is now the world’s largest package delivery company, serving more than 220 countries and territories.

Thanks to a global fleet of more than 120,000 vehicles, over 500 aircraft, and more than 900 distribution facilities, in 2018 UPS delivered 21 million packages per day for 10.6 million customers including 2.5 million businesses.

UPS’s business is organized into three segments:

Domestic Package (61% of revenue, 53% of operating profit): UPS is a leader in time-sensitive, small package delivery services in the U.S., offering a full spectrum of domestic guaranteed ground and air package transportation services. UPS delivers more ground packages in the U.S. than any other carrier, with average daily package volume of over 14 million, most within one to three business days.

International Package (20% of revenue, 35% of operating profit): UPS first expanded outside the U.S. more than 40 years ago. The company now offers a wide selection of guaranteed day and time-definite international shipping services across Europe, Asia, Canada, Latin America, the Middle East, and Africa. Europe accounts for about half of international revenue.

Supply Chain & Freight Operations (19% of revenue, 12% of operating profit): UPS provides freight forwarding and logistics services to help businesses outsource these non-core activities to get their goods to the right place, at the right time, at a competitive cost. Increasingly complex supply chains are creating more demand for a global offering that handles transportation, distribution, and international trade and brokerage services.

While the domestic business continues to generate the majority of revenue and operating profits, the company continues to expand overseas and diversify into supply chain & freight services.

UPS's operating profit from its U.S. operations has decreased from 88% of the total mix in 2000 to about 70% today. In 2018 the company's international and supply chain businesses made up 47% of operating profits, showing the firm's dedication to diversifying its business and grabbing a large share of the package delivering market in developing nations.

United Postal Services froze its dividend during the financial crisis but has grown it every year since then and paid stable or rising dividends since 1969.

Business Analysis Warren Buffett's Berkshire Hathaway and Bill Gates' Foundation Trust both own stakes in UPS, so it's no surprise that this business appears to have several enduring competitive advantages.

Most notably, the global delivery service business is characterized by high barriers to entry because few companies can afford to invest in all of the hard assets required to be a timely, reliable, and affordable operator in this space.

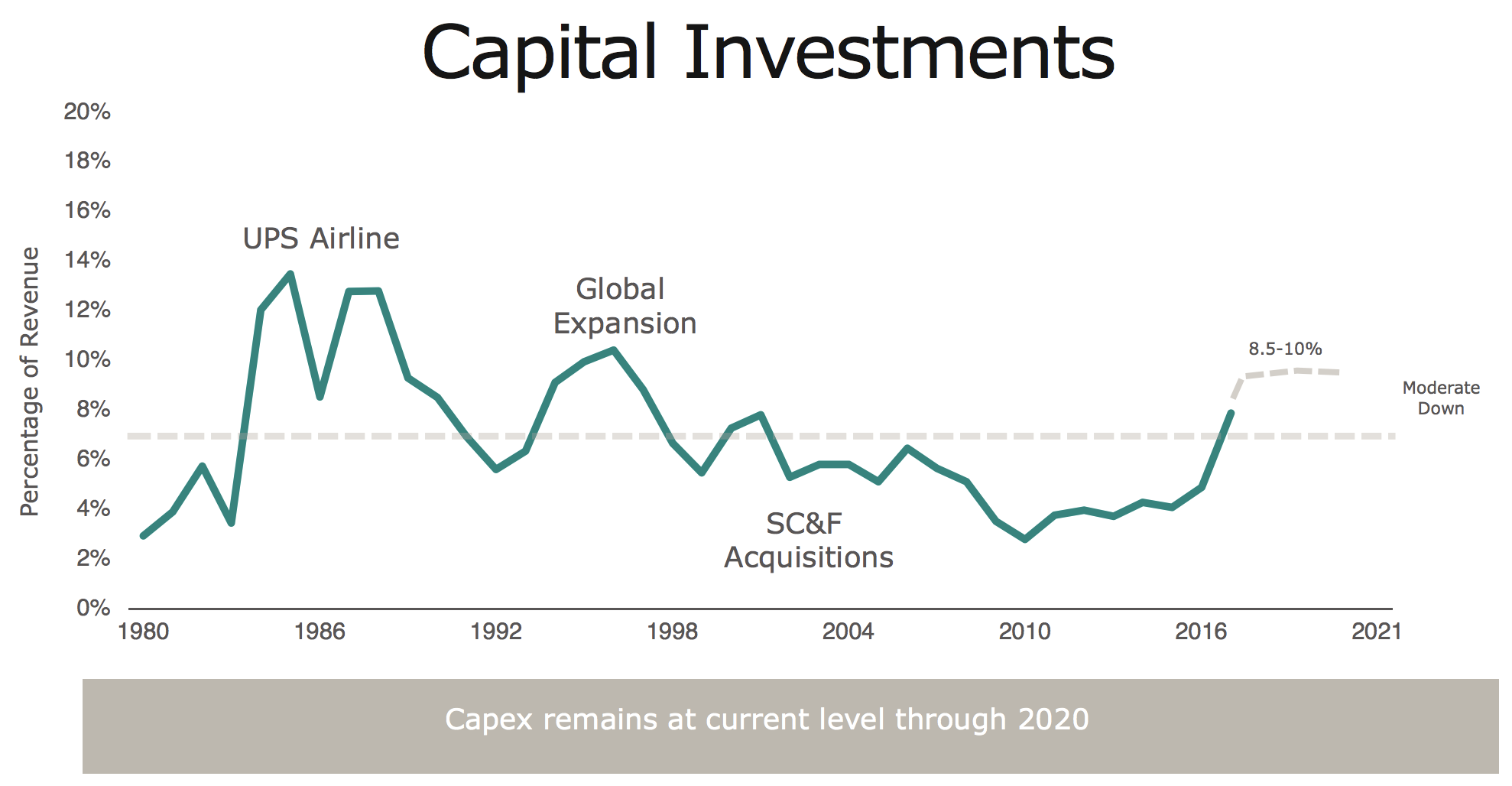

Many companies will only reinvest 2% to 4% of their annual revenue in capital expenditures (capex), such as plant, property, and equipment. However, to build out and maintain its global delivery and logistics network, you can see that UPS's capex routinely exceeds 5% of sales, and management plans on maintaining 8% to 9% capex spending for the foreseeable future.

Source: UPS Investor Presentation

The company's capex spending as a percentage of sales was even in the double-digit range throughout part of the 1980s and 1990s as UPS built out one of the largest airlines in the world and expanded its global reach via development of its Worldport hub in Kentucky, which is the largest automated package handling facility in the world.

UPS's capital expenditures have totaled almost $15 billion in just the last three years alone (plus another $2.6 billion spent on acquisitions), which has helped the company build a hard-to-replicate network of assets.

In total, UPS owns or leases:

Over 1,800 package operating facilities (88 million square feet of floor space)

More than 500 facilities supporting its freight forwarding and logistics operations

About 550 aircraft (UPS operates one of the largest airlines in the world)

Over 123,000 package cars, vans, tractors and motorcycles

45,000 containers used to transport cargo in its aircraft

More than 900 distribution centers and field stocking locations

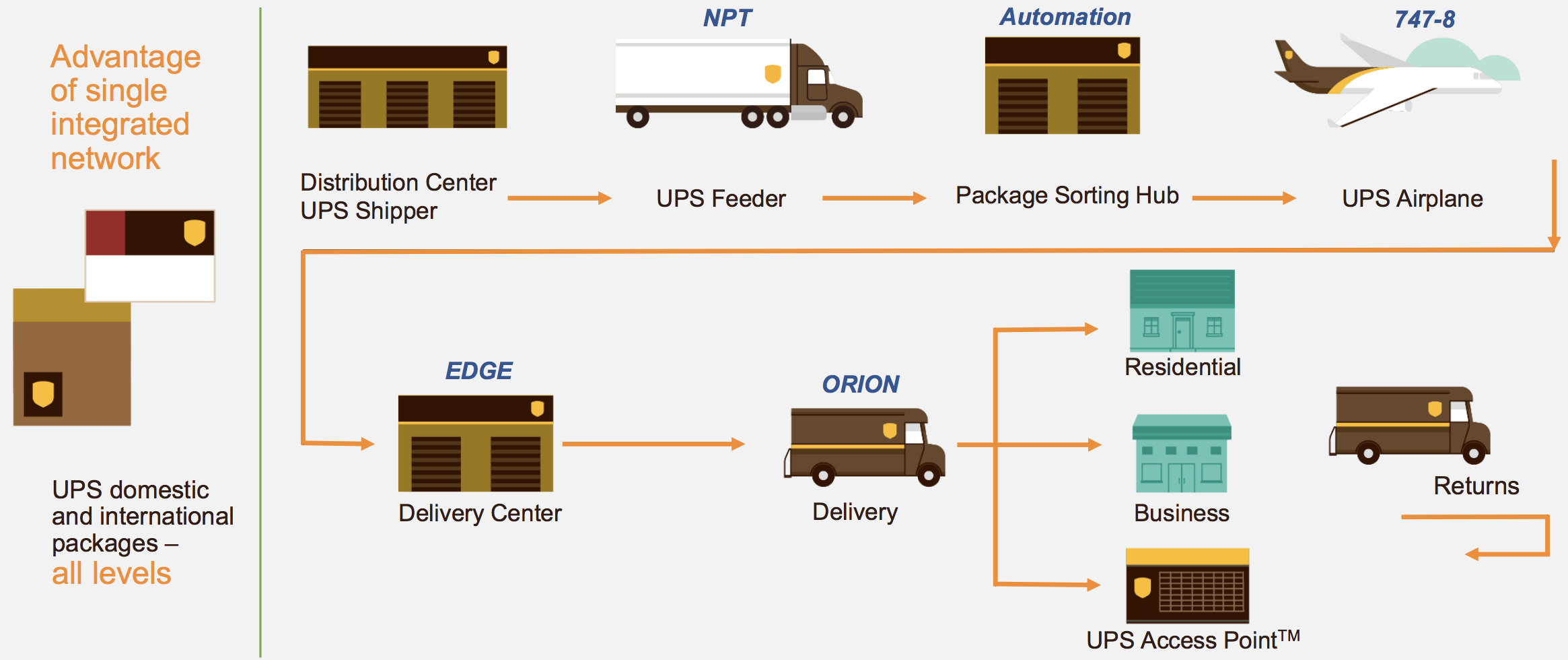

Unlike FedEx (FDX), which splits its ground and air operations into two separate networks, UPS uses only one network to provide its delivery services. This helps keep the firm's operations more efficient.

Besides its operational efficiency, global reach, and well-known brand, UPS is also a durable business because it makes the shipping process easy and convenient for consumers and businesses. The firm boasts a global network offering about 150,000 entry points where customers can tender a package to UPS at a location or time convenient to them. This network includes roughly 5,000 UPS store locations, 39,000 drop boxes, and more than 28,000 UPS Access point locations.

Given the industry's capital intensity, plus the many regulations delivery companies must comply with, it's no surprise that the U.S. market is largely dominated by UPS and FedEx today.

However, UPS has the most extensive integrated global ground and air network in the industry. The company can provide virtually all types of package services (air, ground, international, commercial, residential, etc.) through a single pickup and delivery service network.

Source: UPS Investor Presentation

Importantly, UPS gains a meaningful cost advantage as the world's largest package delivery company. As more customers use its network to move their goods around the globe, UPS can improve the utilization rates of its distribution centers, sorting hubs, airplanes, and delivery trucks.

The cost UPS pays to fly one of its planes or send out a delivery truck on a route is largely fixed, regardless of how many packages are being carried. Handling more packages over time ultimately leads to denser delivery routes (i.e. fuller planes, trucks, and distribution centers), helping UPS spread its high fixed costs over a larger number of goods to lower its per unit costs and improve profitability.

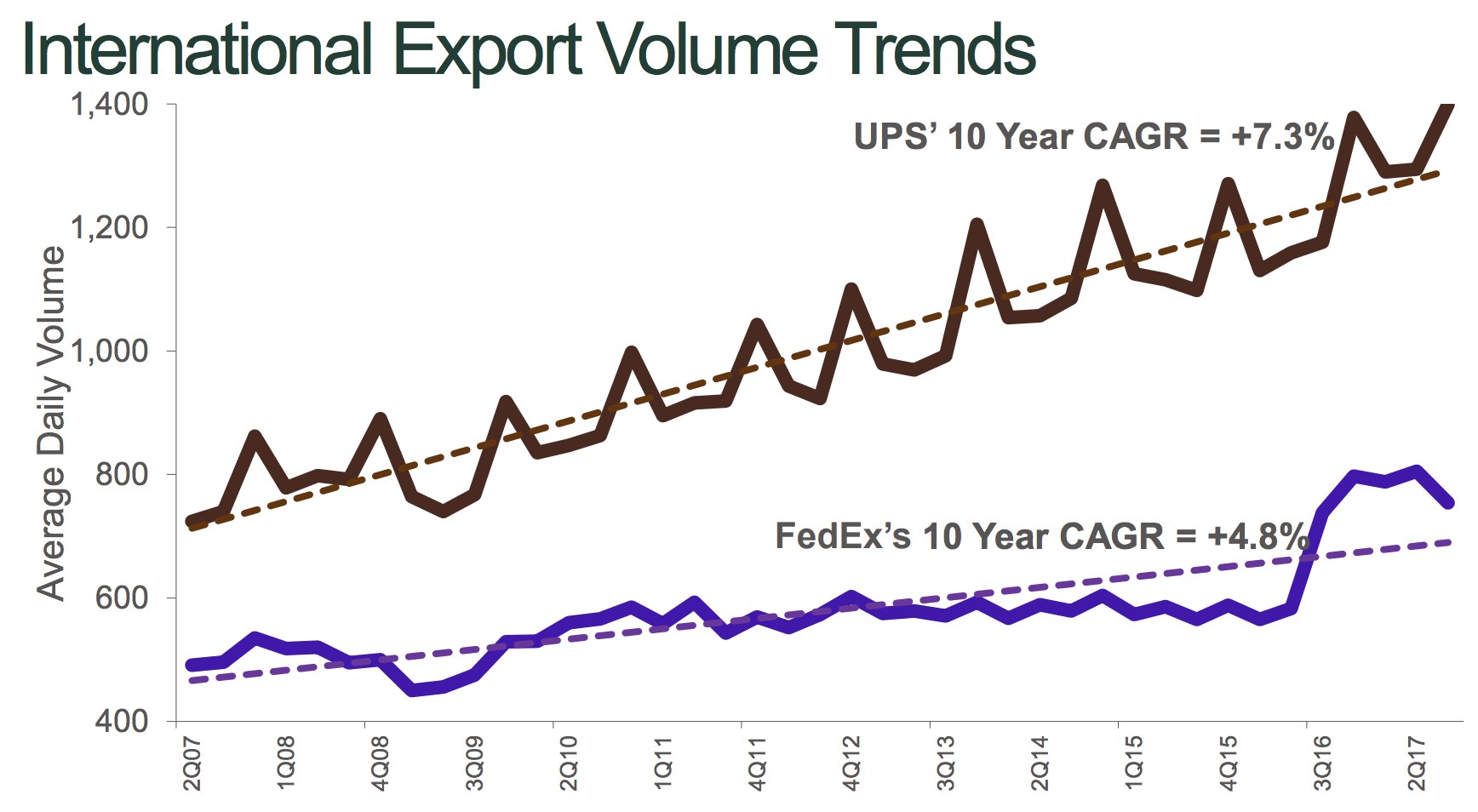

UPS has done a great job delivering more packages each year, with the company's 2018 domestic and international revenues rising about 7% each. Looking longer term, UPS's international business has demonstrated particularly impressive long-term volume growth, especially compared to rival FedEx.

Source: UPS Investor Presentation

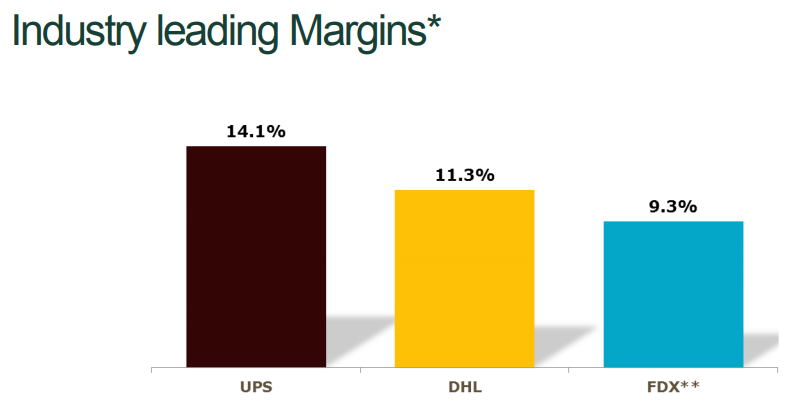

UPS's industry-leading scale and superior network efficiency have allowed it to achieve such impressive growth without sacrificing operating margins, which are higher than its main rivals.

Source: UPS Investor Presentation

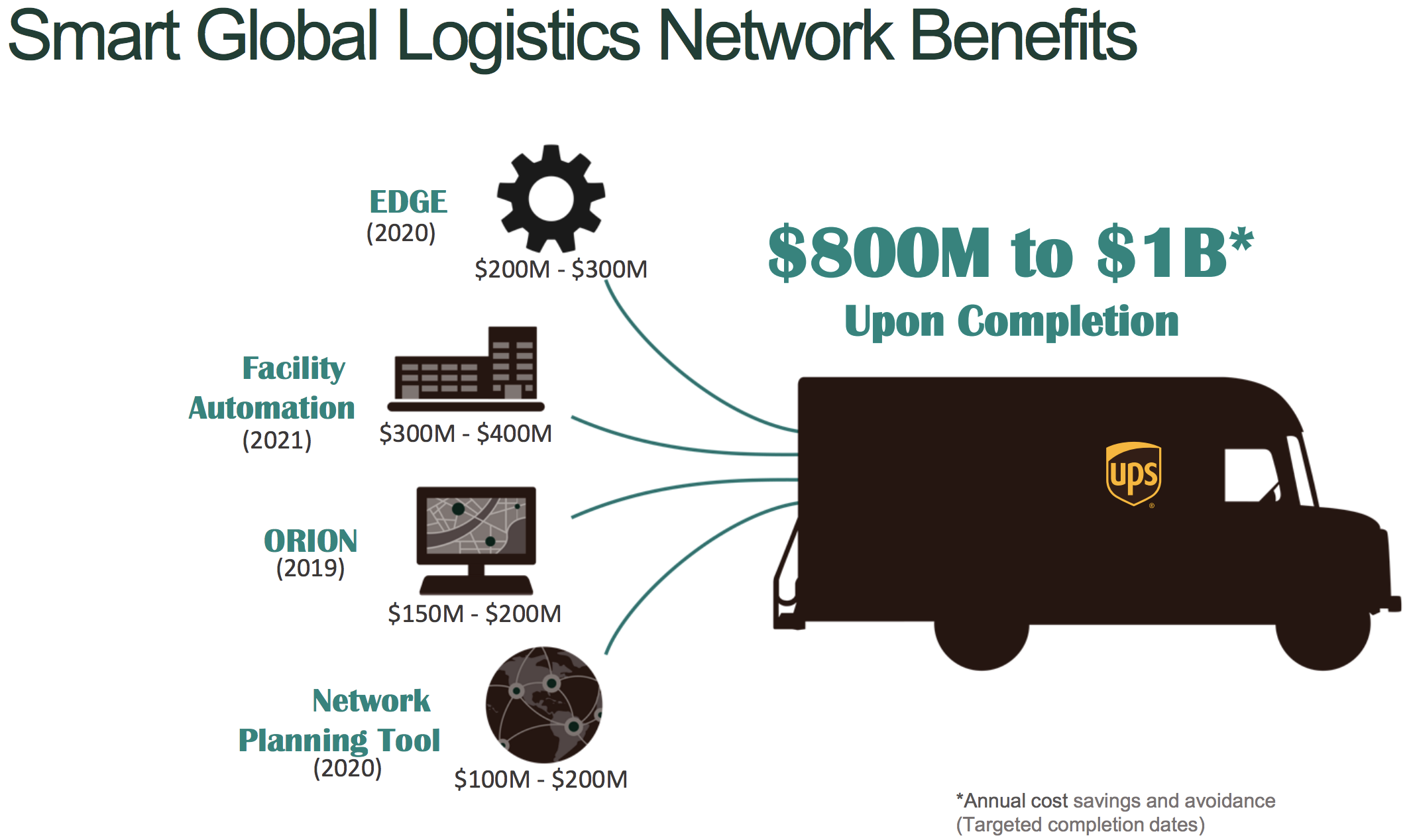

Part of the company's impressive profitability is also attributable to UPS's sharp focus on cost controls, including projects such as ORION, or On-Road Integration & Navigation, which utilizes route optimization to reduce delivery time, improve reliability, and cut fuel waste.

By continuing to invest in route optimization technologies and facility automation, UPS has consistently boosted the efficiency of its network. The company's ongoing investments are expected to generate $1 billion in annual cost savings by 2021, representing more than 1% of annual sales and boosting its free cash flow by about 20% to 25% over 2019's levels.

Source: UPS Investor Presentation

When combined with UPS's proven ability to deliver more and more packages each year, the company's primary competitive advantages (leading economies of scale, efficient transportation network, low per unit delivery costs) should continue to grow. UPS can also cross-sell its supply chain & logistics services to many of its package delivery customers to help meet more of their total transportation needs.

UPS's long-term growth is expected to come from a steady rise in the global package and logistics market, which in 2018 was already $800 billion in size (UPS has about 8% market share with room to expand).

The company estimates that between 2017 and 2022 the worldwide rise of e-commerce will mean 40% more package deliveries, a secular trend its aggressive network investments are meant to profit from. In fact, business-to-consumer shipments have already increased from just over a third of UPS's deliveries in 2009 to more than half of the firm's volume today.

UPS also plans to benefit from the rise of logistics spending in healthcare (for delivering things like medications and testing kits), which is estimated to grow from $85 billion in 2017 to $105 billion by 2021.

Overall, it's not hard to see why UPS appears to be a business that is built to last. Smaller rivals have a hard time replicating the company's convenience for customers, and their less efficient networks result in higher per unit costs on a global basis. As UPS continues taking more packages into its network, especially as e-commerce spending rises, its competitive position seems likely to strengthen.

Importantly, the business has a conservative and financially disciplined culture as well. UPS initiated an employee stock ownership tradition back in 1927 and is known for hiring its top executives from within its ranks (the current CEO has spent over 40 years with the company). In addition to the company's investment grade credit rating, these factors have all enabled UPS to pay uninterrupted dividends since 1969, an impressive 50 consecutive years.

Going forward, UPS seems likely to continue growing its earnings and dividend at a mid-single-digit rate. The path likely won't be linear due to the heavy investments the company must make to continuously improve its delivery network, but the resulting growth runway looks impressive.

Key Risks Several factors can impact UPS's short-term results and stock price performance, though they are unlikely to be concerns for long-term shareholders.

First, note that nearly 60% of the company's global workforce is unionized, with most of those employees under the Teamsters union. A new five-year contract was agreed to in October 2018 and is in the process of being ratified, so UPS doesn't face much short-term strike risk. However, the firm could in the future due to the strong power of its unionized workers to potentially disrupt its business.

UPS's business is also cyclical and tied to the health of the U.S. and global economy. During recessions, consumer spending, industrial production, and retail activity usually fall significantly, resulting in fewer delivery volumes and greater pricing pressure.

Making matters worse, the high fixed costs of UPS's business model mean that even minor revenue declines can create large swings in earnings and cash flow. In fact, during the financial crisis UPS's revenue fell 12% in 2009, but its EPS and free cash flow per share both tumbled more than 30%.

Fortunately, UPS has a very conservative management team which has been disciplined with its use of debt. As a result, the company has an A+ credit rating from Standard & Poor's and enjoys access to low-cost debt, supporting the safety of its dividend.

Besides magnifying profit growth both ways, the capital-intensive nature of the business can also create other headaches any given year. For example, here's how much UPS spent on capex (investing in its business) in the last three years:

2016: $3.0 billion

2017: $5.2 billion

2018: $6.3 billion

Three Year Total: $14.5 billion

Most of this spending was focused on increasing peak delivery capacity because the company struggled to keep up with the surge in holiday shipping volumes (a good problem to have over the long term), which ended up weighing on its profitability as it had to rent more expensive transportation assets to meet demand.

Buying dozens of airplanes, expanding the availability of its Saturday delivery service, and automating more of its facilities and transportation network all require serious cash and can hurt short-term margins, free cash flow, and leverage.

The company's strong balance sheet helps mitigate these risks as it relates to UPS's dividend safety profile, and UPS's investments are necessary for its long-term future. This spending strengthens the company's network, better positions the firm to capitalize on rising e-commerce spending and worldwide trade, and ensures customers continue receiving the convenience, timely deliveries, and reasonable prices they have come to expect.

However, while the rise in package volume is certainly a tailwind, it is also encouraging other players to enter the industry. DHL is one example. The international shipping company actually exited the U.S. delivery business in 2008, but the continued rise of online shopping has pulled its focus back to the region. Specifically, DHL launched a delivery service for online retailers in Los Angeles, New York, and Chicago in 2018.

The economics of business-to-consumer deliveries are somewhat more complicated and costly than commercial deliveries because fewer packages are dropped off at each stop. When combined with the spike in holiday volumes UPS has experienced, introducing a new rival in this part of the business could result in some pricing challenges.

While DHL is certainly a notable rival, Amazon, a UPS customer, is the giant investors worry most about. In February 2018, The Wall Street Journal reportedthat Amazon was preparing to launch its own delivery service for businesses, starting with a pilot program with its third-party sellers in Los Angeles. Naturally, Amazon is expected to undercut UPS and FedEx on pricing.

Since then Amazon has made clear that it wants to bring an increasing amount of its delivery needs in-house. FedEx even went so far as to cancel a major contract with Amazon on June 7, 2019, meaning it will no longer deliver Amazon packages (it will still handle some logistics for the company, however).

But FedEx only derives 1.3% of its revenue from Amazon, while UPS gets up to 10% of its sales from the dominant e-tailer in America, according to its latest annual report.

How big of a threat is Amazon? Amazon's air fleet, which it began building in 2015, stands at 40 today, but Morgan Stanley estimates it will grow to 100 by 2025.

Even if Morgan Stanley is right, 100 planes would be about six times less than the fleet UPS utilizes today. So Amazon isn't going to necessarily overtake UPS's air business. But according to Wolfe Research, Amazon is already handling 26% of its own online delivery orders, and Morgan Stanley's Ravi Shanker told CNBC in February 2019:

“Amazon is looking to become a logistics company in their own right...We think that Amazon will be a top logistics provider, whether it’s in trucking or in air, in the coming years. I think the question is just how quickly they will ramp that operation.”

Amazon is known for investing aggressively into its own infrastructure needs first (over the last decade Amazon's shipping/logistics costs have grown from $2 billion to $62 billion), and later monetizing that by offering it to third parties.

That's how Amazon Web Services (AWS) began, with the company first building out cloud infrastructure for its own needs, and then later becoming the world's largest cloud company by selling the same services to other firms.

With Amazon's fast-growing logistics needs requiring a lot of investments, from a company's whose AWS and advertising businesses are minting billions in free cash flow, Amazon could become a formidable rival for both FedEx and UPS at some point in the future.

Essentially, Amazon represents the one company with the resources, patience, and needs to potentially recreate the same logistics infrastructure that has supported FedEx's and UPS's moats for decades.

And unlike FedEx, who wouldn't lose much direct revenue from Amazon deciding to completely go it alone in shipping, UPS's short-term results could be significantly more impacted by the loss of Amazon's business (UPS ships most U.S. Amazon Prime 2-day deliveries, for example).

Investors will want to watch closely how Amazon's new logistics and shipping ambitions play out to make sure they don't cause UPS's long-term growth potential to decline.

However, for now, we consider Amazon to be more "headline risk" than a major threat to this company's long-term investing thesis. After all, the immense scope and growth of online retail delivery, combined with the sheer amount of time it would likely take to assemble a competitive global network, suggest that Amazon is unlikely to be an existential threat to UPS's business.

Closing Thoughts on United Parcel Service UPS represents a best-in-breed delivery company with a very shareholder-friendly management team, one that has rewarded investors with stable or higher dividends for 50 consecutive years.

The company's global scale, hard-to-replicate global transportation network, and continued investments in efficiency initiatives seem likely to keep UPS at the top of its industry and paying safe, growing dividends for many years to come.

While high capital spending needs, potential threats from Amazon, and occasional global economic turbulence can weigh on the company's short-term stock performance at times, UPS's long-term outlook seems to remain favorable.

With plenty of growth opportunities both domestically and overseas, especially with the continued rise of online retail, UPS appears to be a reasonable investment to consider for most well-diversified dividend growth portfolios.