Thoughts on Smucker's Tough Year and Dividend Appeal

Consumer staples companies like J.M. Smucker (SJM) are often owned for their recession-resistant qualities and safe dividends. Food and beverage makers tend to be low volatility stocks that serve as defensive holdings in conservative dividend growth portfolios.

But Smucker has had a challenging year, down 24% in 2018 and off 40% from its mid-2016 high. That's driven the stock's dividend yield to over 3.5%, its highest level since the Financial Crisis.

Let's take a look at why investors are so bearish on the company and whether this food giant's long-term dividend growth thesis remains intact.

Why Smucker has Underperformed Many large consumer packaged goods companies have struggled with sluggish organic growth in recent years due to changing consumer tastes for healthier, fresher foods.

Smucker has been more proactive than many of its rivals in attempting to adapt its product offerings and focus on faster-growing markets outside of packaged food. For example, in 2011 the firm bought Sara Lee's coffee division for $400 million, and then in 2015 Smucker paid $5.8 billion to acquire Big Heart Pet Brands.

Most recently, in April 2018 management acquired Ainsworth Pet Nutrition for $1.9 billion. And later that summer the firm decided to sell all of its U.S. baking businesses (including Pillsbury and Hungry Jack) to a private equity firm for $375 million, including debt assumption.

Like many food makers, Smucker made these moves in an effort to diversify into larger markets with better growth potential. In fact, management claims that the size of categories Smucker now participates in has increased 25% compared to five years ago.

Consumers are increasingly willing to pay premium prices for healthier offerings that Smucker has targeted, including for products like dog food (pets are seen as members of the family).

As you can see below, over the last five years the company's portfolio has reduced its exposure to troubled areas, such as baking products and shortening & oils, while branching into the pet food market in a big way.

Source: Smucker Investor Presentation

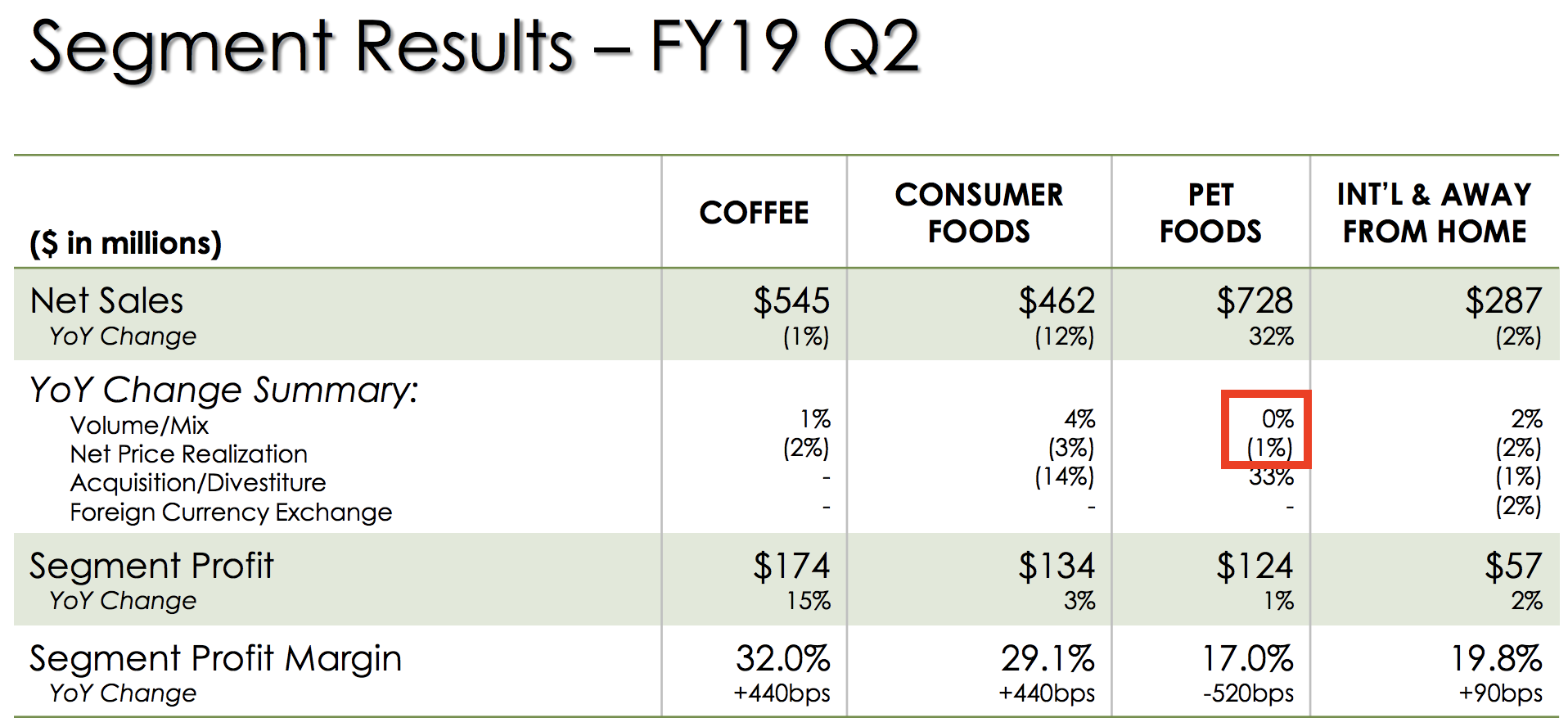

According to analyst firm Euromonitor, pet food is a $30 billion market in the U.S. With 3.6% growth in 2017, the pet food category is growing three times faster than overall packaged foods (1.2%). But factoring out the recent Ainsworth acquisition, even Smucker's pet food organic sales were down 1% last quarter (due largely to the discontinuation of several product lines).

Source: Smucker Investor Presentation

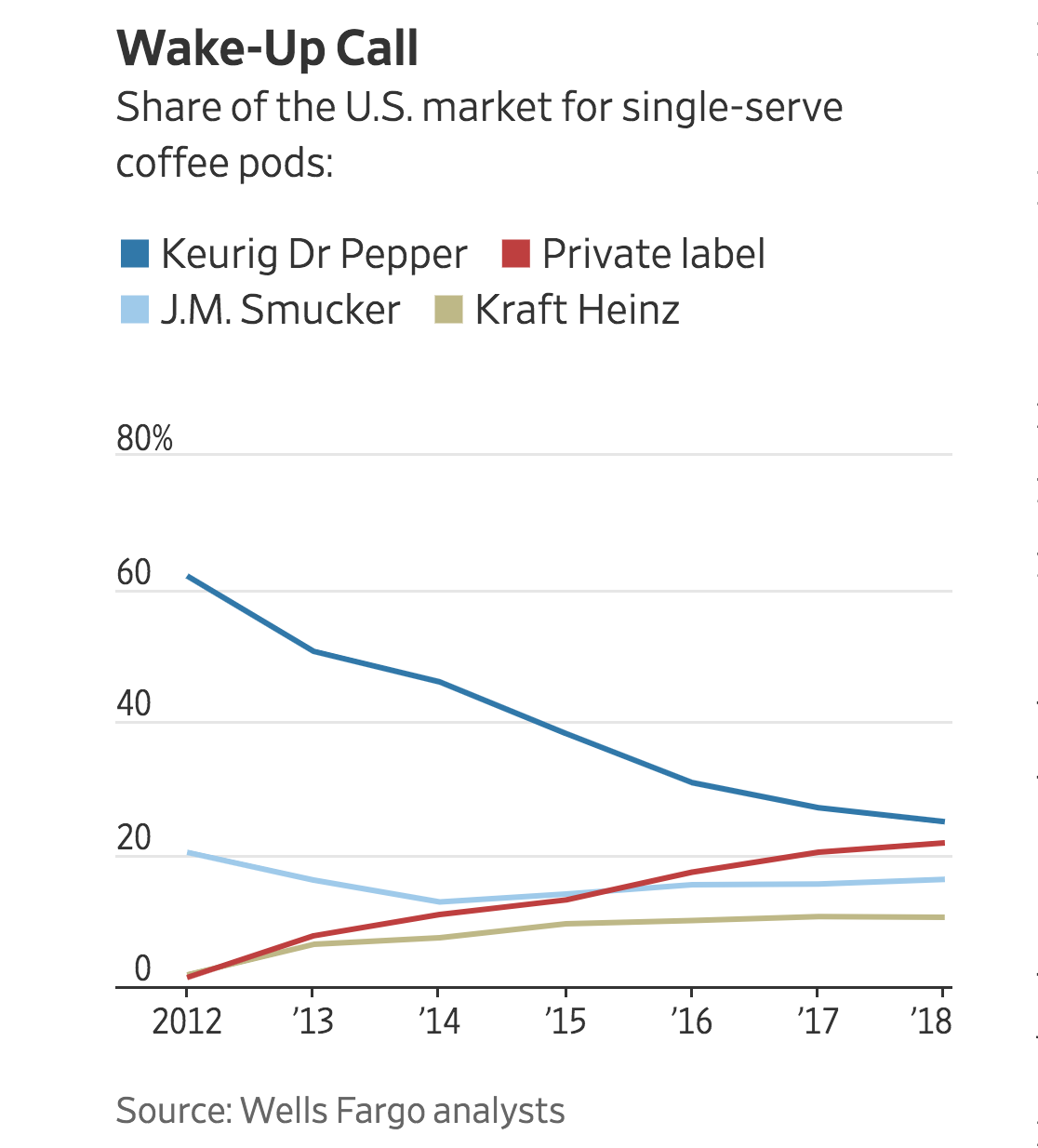

And in the coffee market, which Smucker became a dominant player in with its $3.8 billion acquisition of Folgers in 2008, the company has seen recent sales weakness (2% decline in pricing) due to rising competition.

The Wall Street Journal recently published an insightful article on the U.S. coffee market, noting that "big brands are losing share to smaller upstarts." Private label continues taking share and putting downward pressure on prices.

Source: The Wall Street Journal

Simply put, the trouble for Smucker, and the key reason why investors are frustrated with the business, is that its core food products (the firm is the seventh largest shelf-stable food and beverage manufacturer) are struggling.

Company-wide organic sales slumped 1% last quarter, suggesting that Smucker's efforts to adapt its portfolio to new consumer tastes isn't going as well as management had hoped.

Meanwhile, as if poor organic growth wasn't bad enough, higher raw material and freight costs (something bedeviling all consumer staples companies recently) pushed down the firm's gross margin by 60 basis points.

One reason investors are worried about falling margins is that, theoretically, consumer staples giants like Smucker have strong brands that should provide good pricing power. In other words, they should be able to pass on higher costs to consumers without losing market share.

Thus far in 2018 that hasn't been the case. In fact, in the second quarter of fiscal 2019 Smucker reported weaker realized pricing on coffee, peanut butter, pet food, and pet snacks. That continues a yearlong trend (last quarter pricing on these product lines also fell, resulting in -1% organic revenue growth).

Finally, management revised down its full-year 2019 fiscal guidance (2018 was also a year that saw several downward guidance revisions) to $7.9 billion in revenue (4% sales growth), but just 2% adjusted EPS growth. Most importantly, the midpoint of free cash flow guidance was revised to $725 million from $795 million.

This guidance implies that management is expecting another weak year of organic growth (sales growth was mostly driven by acquisitions) and falling margins, calling into question the idea that Smucker's current brand portfolio is the right fit for driving future growth.

Some analysts expect the company to continue to sell off struggling brands in the future, which could weigh further on its growth rates. In fact, analysts are currently expecting just 4% long-term annual EPS growth from Smucker, which is a less than half its historical earnings growth rate of about 9%.

Is Smucker's Long-term Dividend Growth Thesis Intact? Management's plans for returning Smucker to stronger sales and earnings growth involves investing more aggressively in new product offerings, including premium products like its recently launched 1850 premium coffee brand, which joins its other two strong coffee brands Dunkin’ Donuts and Cafe Bustelo.

The company will also have to contend with faster rates of change across the food and beverage industry. Naturally, management is confident it can do so:

"Let me reiterate that we are taking and will continue to evaluate appropriate actions that support our consumer-led strategy to be a food and beverage leader focused on high-growth on-trend categories. Whether through innovation, acquisitions, divestitures or improving capabilities and execution in key areas, these actions are indicative of the fast pace of change within our company." - Mark Smucker, CEO

Smucker is led by CEO Mark Smucker, who is the great-great-grandson of company founder Jerome Smucker. He's been with the company for 19 years and remains confident that the firm will be able to adapt with new product offerings that are "on trend" with today's more health-conscious consumers.

Such products account for around 26% of Smucker's overall sales today and are expected to grow at a high single-digit pace in the years ahead, helping offset declines in more challenged areas of the business.

Source: Smucker Investor Presentation

While portfolio reshuffling and acquisitions are far from easy, Smucker appears to be well on its way to focusing on the strongest growth opportunities of the future (coffee and pet food).

In fact, in 2019 70% of Smucker's sales will come from coffee and pet food, and the company's focus on premium products (upmarket shift) should help support long-term profitability.

Classic brands like Jif peanut butter are also now being transitioned to new product lines such as snack bars, to capitalize on the popularity of protein bars and convenient on-the-go meal offerings.

In addition to better product offerings and on-trend brands, Smucker has been seeing success in online sales, including 71% e-commerce growth in 2018 (64% for pet food and 154% for coffee).

Meanwhile, the company plans to double down on its economies of scale through cost-cutting, including $80 million in incremental savings in 2019 and $70 million targeted in 2020.

That might not sound like much, but for a company with $7.6 billion in annual revenue, it represents upwards of 100 basis points of annual profit margin improvement to help boost earnings and free cash flow.

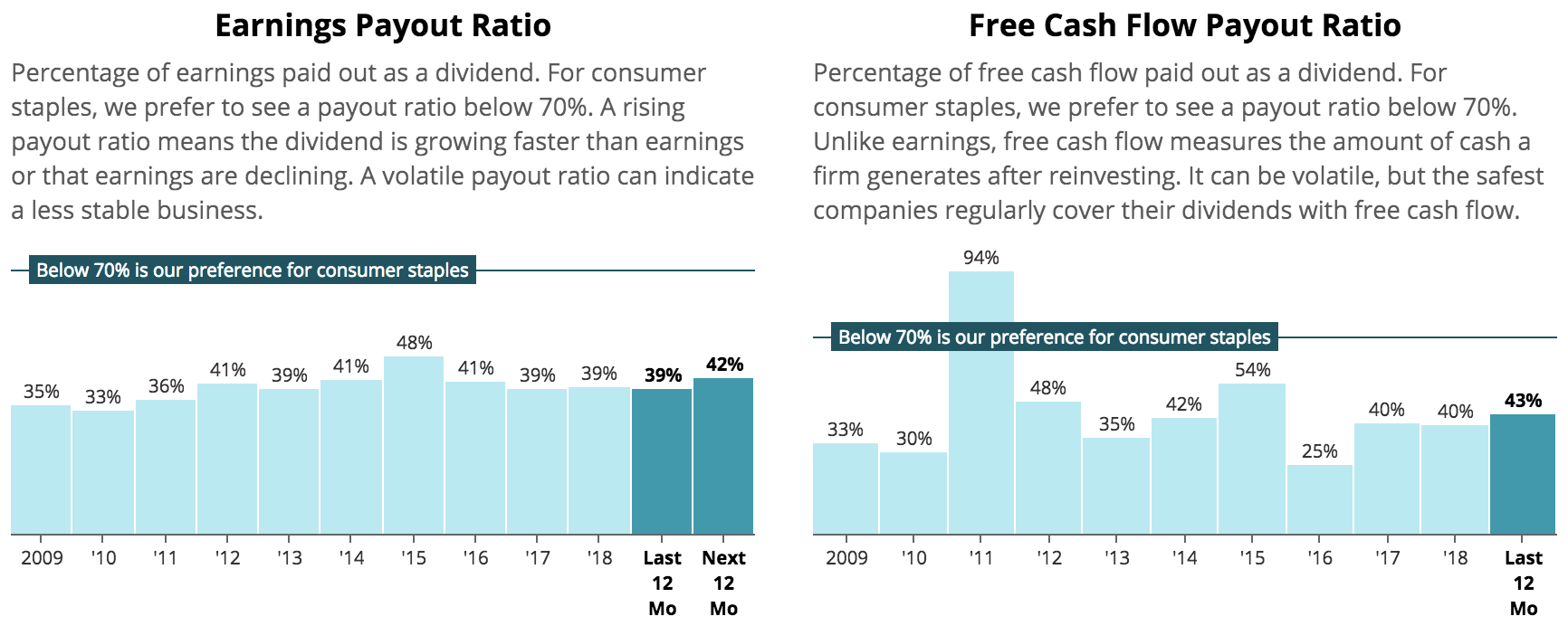

What about Smucker's dividend safety? Conservative payout ratios and a strong balance sheet are important pillars for a safe dividend.

Fortunately, Smucker's earnings and free cash flow payout ratios both sit below 45%, which is a very reasonable level for this recession-resistant industry. You can also see that the firm's latest payout ratio values are quite consistent with its long-term history, suggesting management is comfortable with these levels.

Source: Simply Safe Dividends

However, Smucker's debt levels are somewhat elevated compared to its past. In 2015 the firm's leverage jumped significantly thanks to the $5.8 billion acquisition of Big Hearts Pet Brands (maker of Meow-Mix and Milk Bone).

Like Smucker's large acquisition of Folger's in 2008, this was a transformational acquisition that put the company into an entirely brand new market, one that it sees as key to driving its future growth.

Source: Simply Safe Dividends

The good news is that CFO Mark Belgya told analysts on the last conference call that deleveraging is a key priority for the company, which should allow it to retain its investment grade credit rating of BBB.

However, deleveraging also means that Smucker might have to be more conservative with its dividend increases in the future, since it will need most of its retained free cash flow to pay down debt it has taken on in recent years (including to buy Ainsworth).

With management forecasting $725 million in free cash flow this fiscal year, the company should have around $355 million of cash flow available to continue deleveraging efforts after paying dividends ($370 million). Compared to Smucker's total debt load of $6.3 billion, that seems like a healthy amount of retained cash flow to protect the company's balance sheet and credit rating.

With $171 million in cash on hand, plus an unsecured revolving credit facility with $1.4 billion available, Smucker's appears to have solid liquidity to continue turning around its business, paying dividends, and managing its balance sheet.

Overall, Smucker's long-term dividend growth thesis, while somewhat weakened by its recent struggles, appears to remain intact. However, until the balance sheet is in better shape and organic sales have returned to profitable growth, Smucker's pace of dividend growth seems likely to decelerate into the low to mid-single-digits.

Concluding Thoughts Smucker has been around for more than 120 years. Over that time the firm has proven itself to be a dependable long-term investment thanks to its ability to adapt to changing consumer tastes. Today Smucker is once more in a strategic turnaround, refocusing its portfolio on premium pet food and coffee.

This ongoing pivot might take several years to play out, and it could continue requiring some reshuffling of its existing businesses through acquisitions and divestitures. The good news is that, with the exception of a high but not alarming debt load, Smucker's dividend appears safe and likely to continue growing slowly but steadily for the foreseeable future.

With seemingly low expectations baked into the stock (forward P/E ratio of 11.6 and the highest dividend yield in a decade), Smucker could be an interesting idea for contrarian income investors who are willing to stay patient and bet on the company's eventual turnaround.