Altria's Two Major Investments and Updated Dividend Safety

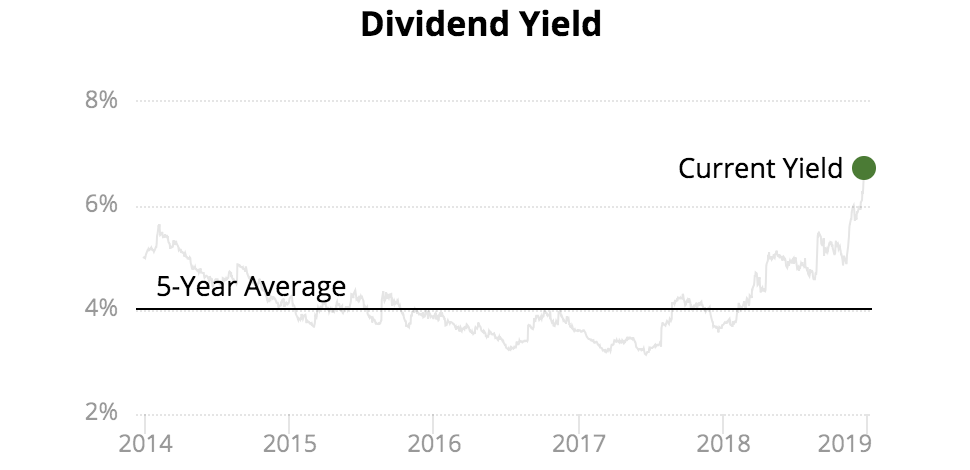

Altria's (MO) share price has slumped over 30% this year, making it one of the worst in history for the cigarette maker's shareholders. Altria's dividend yield now sits at 6.7%, its highest level since the Financial Crisis.

Source: Simply Safe Dividends

A number of factors are behind Altria's rough year, including various negative regulatory announcements from the FDA, slightly larger volume declines in cigarettes, and two market corrections.

However, now Altria appears to be sliding due to the company's recently announced $14.6 billion investments into cannabis company Cronos (CRON) and privately held vaping giant Juul Labs.

With such a scary price decline this year, mounting headwinds for cigarettes, and now worries that Altria is making large but potentially unwise investments, let's take a closer look at these deals to see whether they damage Altria's dividend safety and long-term outlook.

Why Altria is Buying Big Stakes in Cronos and Juul On December 7, Altria announced it was buying a 45% stake in global cannabis company Cronos for $1.8 billion along with the right to acquire (via warrants) another 10% of the company in the future for $1 billion.

Then, on December 20, Altria announced its much larger investment, 35% of privately held Juul Labs, for which it's paying $12.8 billion.

That investment comes after 14 months of negotiations to hammer out some rather unique financial deals including a "standstill" agreement in which Altria won't be allowed to increase its equity stake for six years following the deal's closing. However, Altria was able to obtain an agreement that Juul would not allow any other major tobacco company to invest in it either.

According to Altria's CEO Howard Miller, "These investments complement our very strong core tobacco businesses and provide exciting opportunities for future growth."

According to Arcview Market Research and BDS Analytics, in 2017 global legal cannabis sales were $9.5 billion, a figure that is set to explode now that Canada has legalized the recreational use of cannabis (next year legal sales are expected to hit $5 billion in Canada alone).

Cronos allows Altria to participate in the fast-growing legal cannabis market without running afoul of money laundering laws in the U.S. (cannabis is still illegal at the Federal level).

With more and more countries (and states) legalizing cannabis, the legal market is expected to grow to $32 billion by 2022, and by 2025 analyst firm Grand View research expects global legal cannabis sales to reach $146 billion. That figure may end up being optimistic (this is a very new and uncertain market), but even more conservative estimates place legal worldwide cannabis sales at $75 billion by 2030 (according to analyst firm Cowen).

For perspective, the U.S. tobacco market is currently about $85 billion and U.S. soda sales are just north of $75 billion. This shows why even companies like Coca-Cola (KO) are interested in rolling out cannabis-infused drinks, because cannabis has the potential to move the needle and provide tobacco companies an important secular growth market to counter decades of declining cigarette volumes.

Meanwhile, Altria's Juul Labs investment was to take advantage of the upstart's impressive cornering of the U.S. vaping (e-cigarette) market. According to Nielsen, in October Juul commanded 75% of the U.S. vaping market, compared to just 22% for the combined offerings of Altria, British American Tobacco (BTI), and Imperial Tobacco (IMBBY).

Juul is predominantly selling in the U.S. today, but in June 2018 raised $1.2 billion (valuing it at a $15 billion valuation) in order to accelerate overseas expansion. Today Juul is in seven countries but hopes to recreate its U.S. success around the world, where vaping is already a $23 billion market.

Altria plans to accelerate Juul's U.S. growth by providing it with access to its massive distribution network, which consists of shelf space in approximately 230,000 stores. Altria can also help Juul handle the regulatory approval process involved with the FDA. However, the company will continue to operate independently.

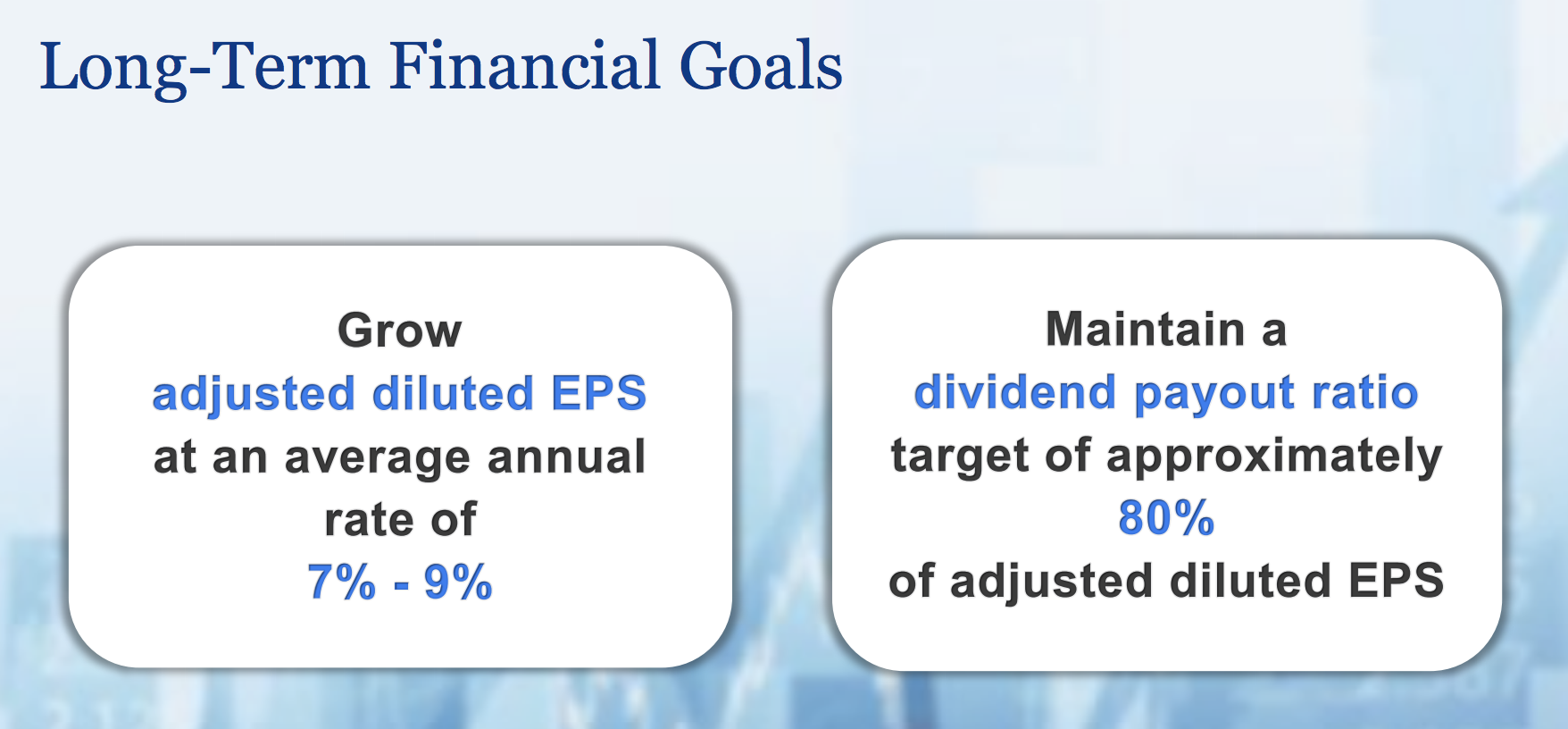

Ultimately, Altria believes that its investments in Cronos and Juul will help it to achieve its long-term goals of 7% to 9% adjusted EPS growth, which with a stable 80% dividend payout ratio should, in theory, allow for dividend growth along the same levels.

Source: Altria Investor Presentation

But if cannabis and vaping are such booming businesses and represent attractive long-term growth opportunities for Altria, then why are analysts, investors, and credit rating agencies (S&P and Fitch just downgraded Altria two notches to BBB and Moody's downgraded it to a negative outlook) so skeptical?

Why the Market is Skeptical of These Deals There are two main reasons why Altria is taking such immense flack for these two investments right now. The first is valuation. Morningstar's analyst Philip Gorhamm, CFA, FRM, put it very simply that he considers this a smart strategic move but that Altria is buying the right assets at the "wrong price at the wrong time". That's because, according to Pitchbook, Juul's most recent reported sales and EBITDA were $950 million and $253 million, respectively.

Altria's investment represents a valuation of $38 billion, which is 2.5 times Juul's most recent capital raise earlier this summer, and 40 and 150 times sales and EBITDA, respectively. In other words, Juul's growth will need to be tremendous for Altria's investment to pay off.

In fairness to Altria, Juul is a rapidly growing company. According to insiders, the firm's most recent annualized revenue was $1.5 billion, and other sources indicate it may be as high as $2 billion.

However, even if these unsubstantiated claims are true (private companies don't report financials very frequently), then Altria is still paying between 19 to 25 times sales for Juul. That's a valuation you most often see with fast-growing tech companies which have far less regulatory uncertainty than what Juul faces.

What about Cronos? Well, Altria is valuing that small and still unprofitable company at $4 billion today, and with its warrants, if exercised (to give it 55% of the shares and control of the company), at $10 billion. As S&P explains in its credit ratings downgrade note, “We view both investments as long-term plays that will not provide meaningful returns in the next couple of years.”

During the firm's conference call, management said that Juul isn't expected to start paying any dividends to Altria (increasing the company's cash flow) for at least one or two years. However, at least on an equity accounting basis (Altria records its share of Juul's profits regardless of whether they are retained or paid out as dividends), management expects that the deals will start to be accretive to Altria's adjusted EPS within two years of closing.

However, Juul's future is somewhat clouded. In November 2018, the FDA releasednew findings from the National Youth Tobacco Survey which showed that "more than 3.6 million middle and high school students were current (past 30 day) e-cigarette users in 2018, a dramatic increase of more than 1.5 million students since last year."

With the spike in teenage vaping, the FDA is now cracking down on e-cigarettes, especially some of the most popular flavors and distribution channels (like convenience stores).

Thus the risk is that Juul's rapid growth in the U.S. (which is largely credited with Altria's cigarette volume declines accelerating to 4.5%, up from 3% to 4% in recent years), may be set to slow.

What about overseas expansion? Well, Juul won't be competing with Altria's core cigarette business (85% of current EBITDA) there, but other countries have far less favorable regulatory environments. For example, in Japan e-liquids are regulated as pharmaceuticals which is why heat-not-burn products like Philip Morris' (PM) iQOS have been so successful.

And as for cannabis and Cronos, while the legal cannabis market seems likely to indeed grow fast and become even more meaningful in size, there is no certainty that Cronos will be able to actually become a dominant global name (the company ultimately sells a commoditized product where strong brands have yet to become established and might never be).

Simply put, Altria is paying a very rich price for both Cronos and Juul, in order to access the potential for large future growth to offset steady declines in cigarette volumes, which are likely to continue forever. While the upside to these investments is still a question mark, the high cost and large amount of debt Altria is taking on are very real and objective risks.

Which brings us to the most important issue of all for Altria investors, what do these investments mean for Altria's dividend safety and growth?

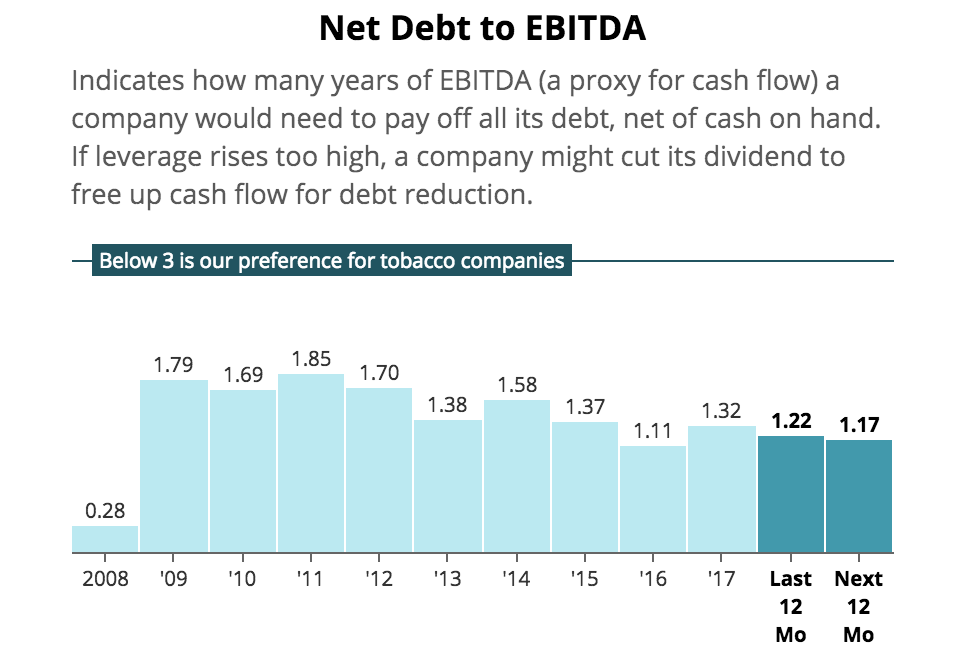

Altria's Dividend Remains Safe, but Deals Somewhat Weaken Overall Profile One of the big reasons that Altria's dividend has been so safe over the years is its strong balance sheet. Not only does the recession-resistant nature of its cash flow make servicing its debt reasonable with a high payout ratio (near 80%), but the firm's net leverage ratio (net debt/EBITDA) has remained low over time. That's largely why Altria previously enjoyed an A- credit rating and low borrowing costs.

Source: Simply Safe Dividends

Modest debt service costs are what allowed the company to use the $1 billion to $1.5 billion it retained in cash flow after paying dividends and reinvesting back into the business to pay down debt and repurchase shares. In fact, share buybacks have driven about 15% of the company's EPS growth over the last five years.

Altria is planning to essentially fund these investments entirely with debt, initially obtained under a short-term credit facility at a cost of LIBOR + 1% (about 3.5% at current interest rates). Eventually, management wants to fix those rates by issuing long-term bonds to repay the facility.

However, these debt-funded deals will result in about $600 million in increased interest costs, which is why management is now warning that 2019's EPS growth will come in below its 7% to 9% guidance range.

And with a credit rating downgrade to BBB (a rating management plans to maintain going forward), the firm's that interest cost rise once Altria converts that short-term debt into long-term bonds.

According to management, Altria's leverage ratio will now climb to 2.6, more than doubling its previous level. However, the firm's leverage should still remain below the 3.0 threshold we prefer to see for this industry.

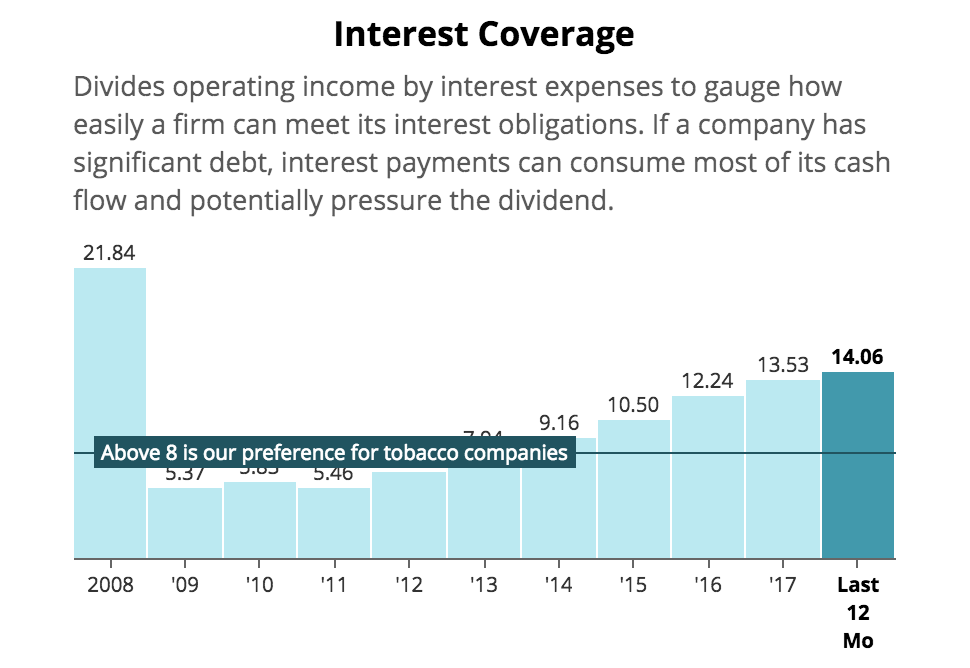

And because neither investment is expected to contribute to Altria's cash flow in the next few years, the company's interest coverage ratio is likely to drop to close to 8 in 2019. That's a large decline from the 14.1 it's been over the past year, but again is not unsafe for a tobacco company.

Source: Simply Safe Dividends

How does management plan to deal with this much higher debt level and interest expense? On the conference call discussing these investments, management revealed that it was planning to reduce annual expenses by $500 million to $600 million per year by the end of 2019, mostly counteracting the higher interest costs.

Some of the targeted cost savings will come from shutting down Altria's existing vaping business and ending its ongoing R&D program. Going forward, Altria's only exposure to U.S. vaping will be through Juul. The rest of the cost reductions will come from streamlining the companies other business operations.

And with about $1.25 billion available in retained cash flow each year after paying for capital expenditures and dividends, management says it will still have the flexibility to either pay down debt over time or repurchase shares.

So what does all this actually mean for Altria's dividend safety?

Due to the increased financial leverage that will occur once these deals are reflected on the firm's balance sheet next quarter, Altria's Dividend Safety Score has been reduced from 85 to 65, still a "safe" level.

Put simply, the company's 49-year dividend growth streak (factoring in spin-offs) appears likely to remain secure; Altria's higher debt and interest costs should not pressure the dividend based on what we know today.

However, because buybacks are likely to be constrained by the need to prioritize debt repayment in the coming years, Altria may struggle to achieve its 7% to 9% long-term EPS growth target.

Management says that the firm's dividend payout policy (80% of adjusted EPS) remains the same. However, since Altria will be using equity accounting to report Cronos and Juul earnings in the future, it's not necessarily certain that Altria's dividend will grow at the same rate as earnings.

That's because dividends are actually paid out of free cash flow. Since Cronos and Juul won't actually be paying any cash to Altria for several years at least, the company's dividend growth in the future may come in at a slower pace (4% to 6%) compared to history.

In other words, Altria's strategic gambles on Juul and Cronos do not appear to break the company's investment thesis, but they introduce additional risks and uncertainties (weaker balance sheet, possibly overpaying, FDA regulatory changes) that could decrease the company's attractiveness to conservative income investors in the future.

Concluding Thoughts Despite nearly 60 years of declining smoking rates in the America, Altria has delivered as an excellent long-term dividend growth investment. Management's ability to adapt to the various challenges that have faced the tobacco industry, along with Altria's portfolio of premium cigarette brands, have allowed the company to raise prices fast enough to offset volume declines and keep its bottom line (and dividend) growing.

Altria's $14.6 billion investments in Cronos and Juul Labs mark the company's latest effort to adapt to a future where cigarette smoking rates will continue falling, perhaps at an accelerated rate as cannabis and vaping grow.

However, the company is paying a rich price for these debt-funded investments, neither of which is certain to pay off. Altria was late to the scene to capitalize on these trends in a meaningful way, forcing management to pay dearly for what could ultimately prove to be necessary long-term product diversification.

Altria's resulting balance sheet hit will reduce its future financial flexibility and somewhat lowers its Dividend Safety Score (from 85 to 65), although its payout still looks safe. However, the company's pace of dividend growth could slow for the next few years.

Overall, Altria still appears to be a reasonable long-term income investment as part of a well-diversified portfolio. However, the company's risk profile has become more complex. Investors need to continue monitoring regulatory developments and U.S. cigarette volume declines, which remain the most important drivers behind Altria's core business and dividend safety profile for at least the next few years.