Iron Mountain: An Interesting High-Yield Stock Facing Several Risks

Founded in 1951, Iron Mountain (IRM) is one of the oldest REITs in America, though it didn’t officially convert to a REIT structure until 2014. While the company initially started off as a paper document storage facility for New York City-based corporations, Iron Mountain has since expanded to become one of the largest data storage centers in the world.

Iron Mountain serves commercial, legal, banking, healthcare, accounting, insurance, entertainment, and government organizations around the world to meet their information storage (and sensitive information destruction) needs.

Source: Iron Mountain Investor Presentation

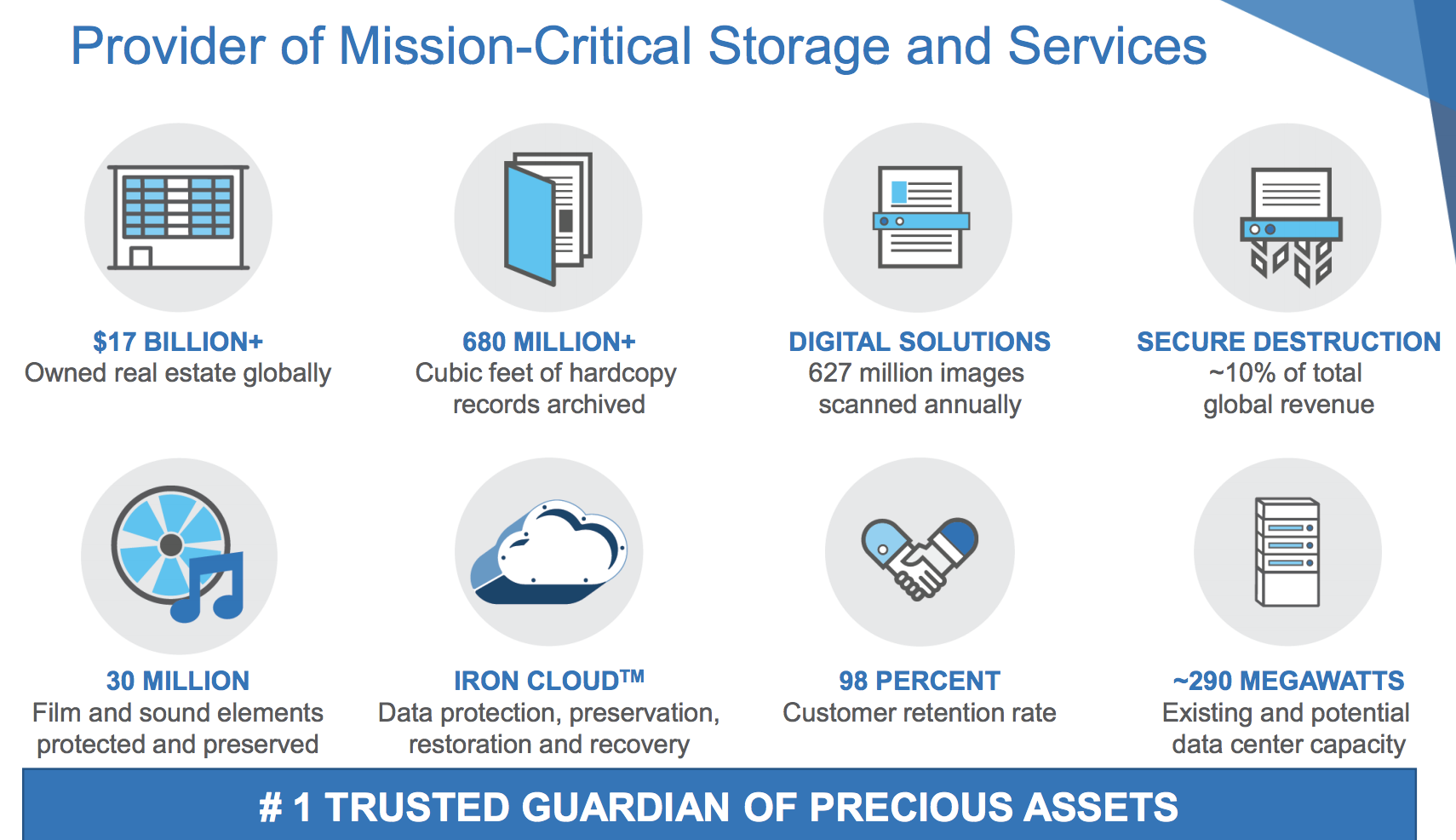

The REIT operates more than 90 million square feet of storage space in nearly 1,500 facilities located in around 50 countries. In total Iron Mountain serves more than 225,000 global customers, including 95% of the Fortune 1000.

Iron Mountain's global diversification helps offset sluggish physical storage volumes in developed markets to keep overall document volume growth steady over time.

The firm's recurring cash flow also enjoys stability thanks to Iron Mountain's customer diversification, with no client representing more than 1% of revenue and its top 20 customers generating just 6% of sales.

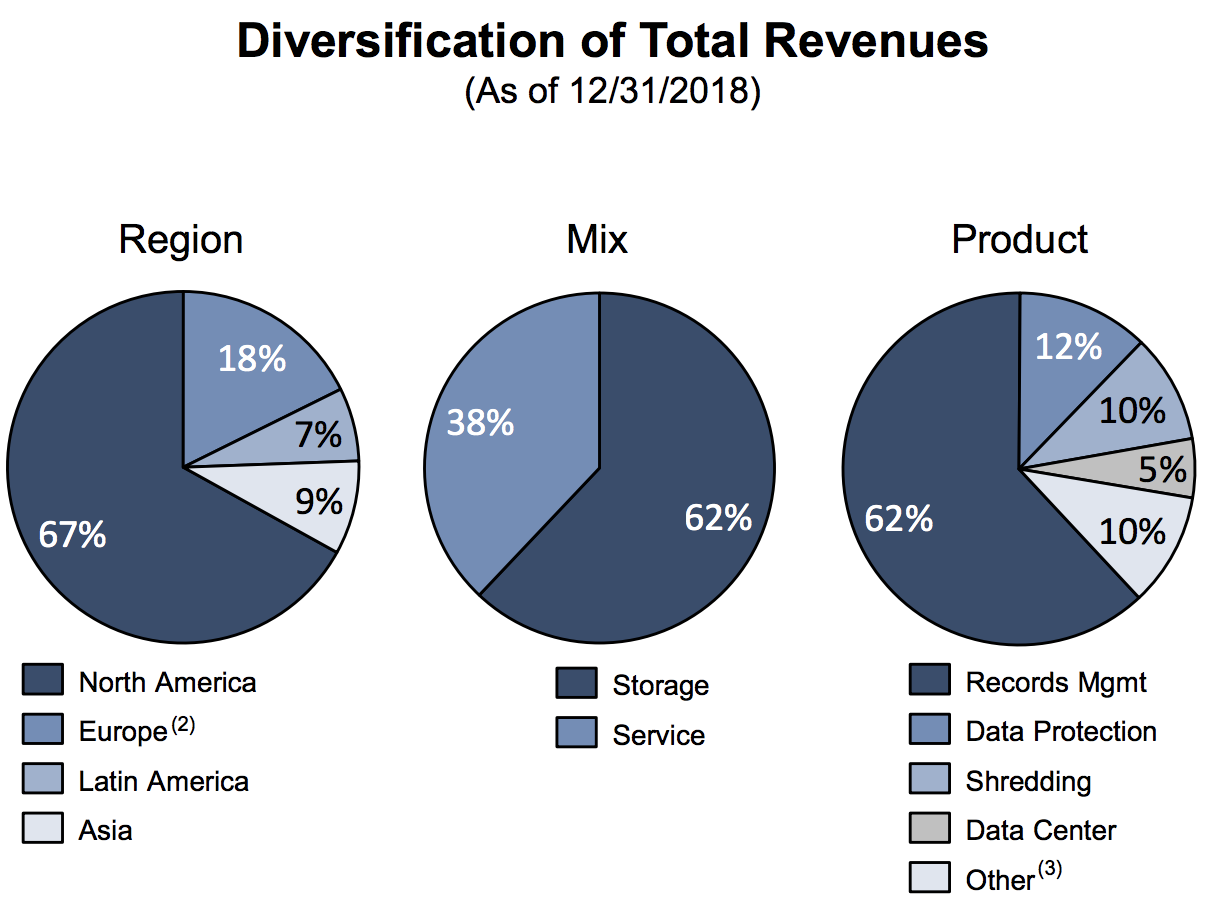

While Iron Mountain's business spans records management, data protection, data management, digital solutions, shredding, data centers, and other adjacent businesses, the company's revenues remain focused on physical document storage in developed markets, where Iron Mountain has spent over 50 years expanding its logistics base.

In fact, over 60% of the REIT's revenue and just over 80% of its gross profits are derived from its storage rental business.

Source: Iron Mountain Earnings Presentation

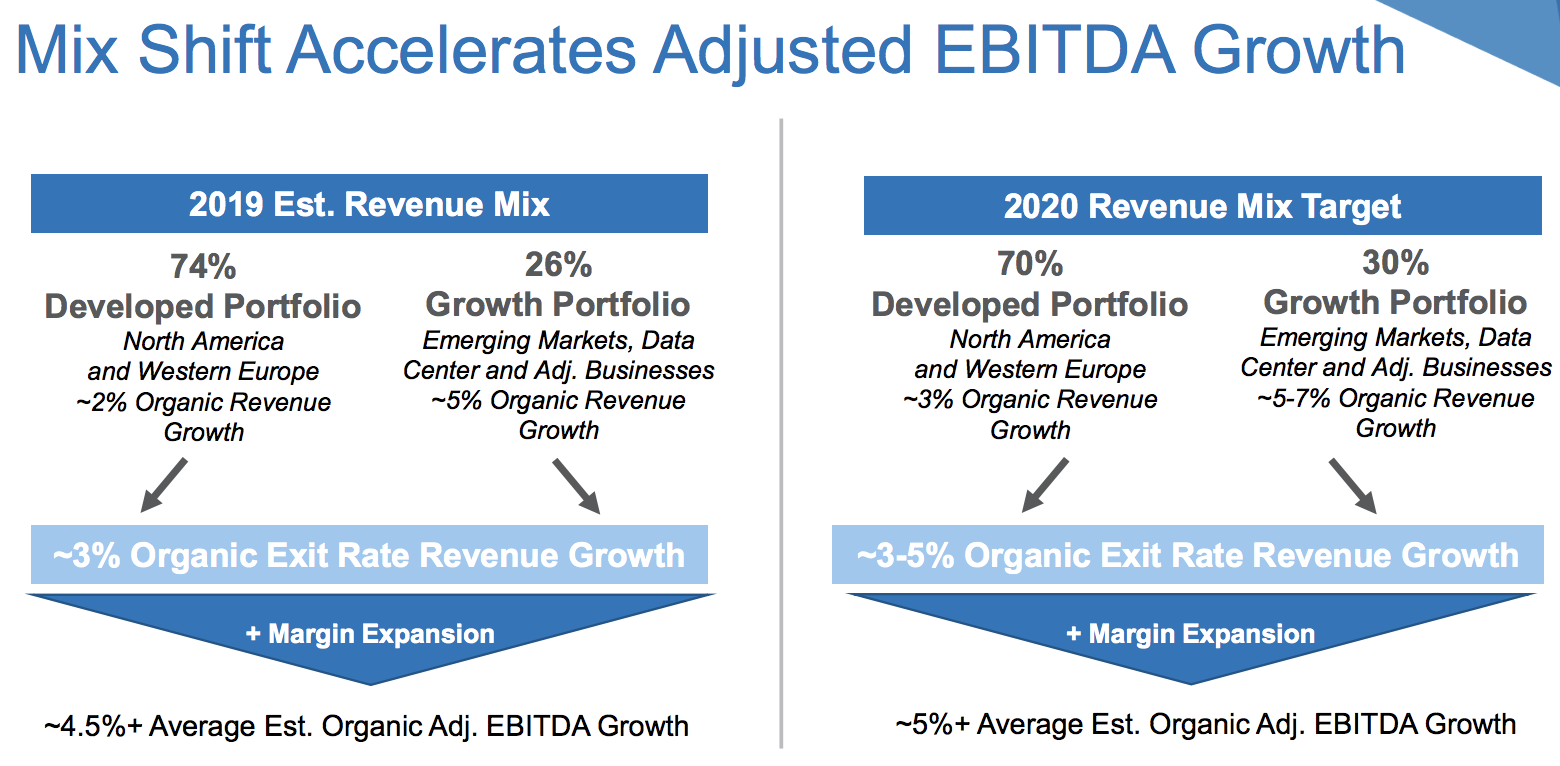

In recent years, Iron Mountain has diversified into growth markets that it expects will help accelerate its long-term cash flow growth to about 5% annually. The company is focusing on physical storage in emerging markets (such as China), increased ancillary services (such as entertainment and fine art storage), and data centers (to protect digital information and host customers’ IT infrastructures).

Prior to 2013, roughly 90% of Iron Mountain's business was in mature markets focused on document storage, with only 10% of sales generated from fast-growing segments. As you can see, management expects the firm's growth portfolio to account for 30% of revenue in 2020, driven by emerging markets and data centers.

Source: Iron Mountain Investor Presentation

Iron Mountain only began paying a dividend in 2010 but has raised its payout every year since then.

Business Analysis

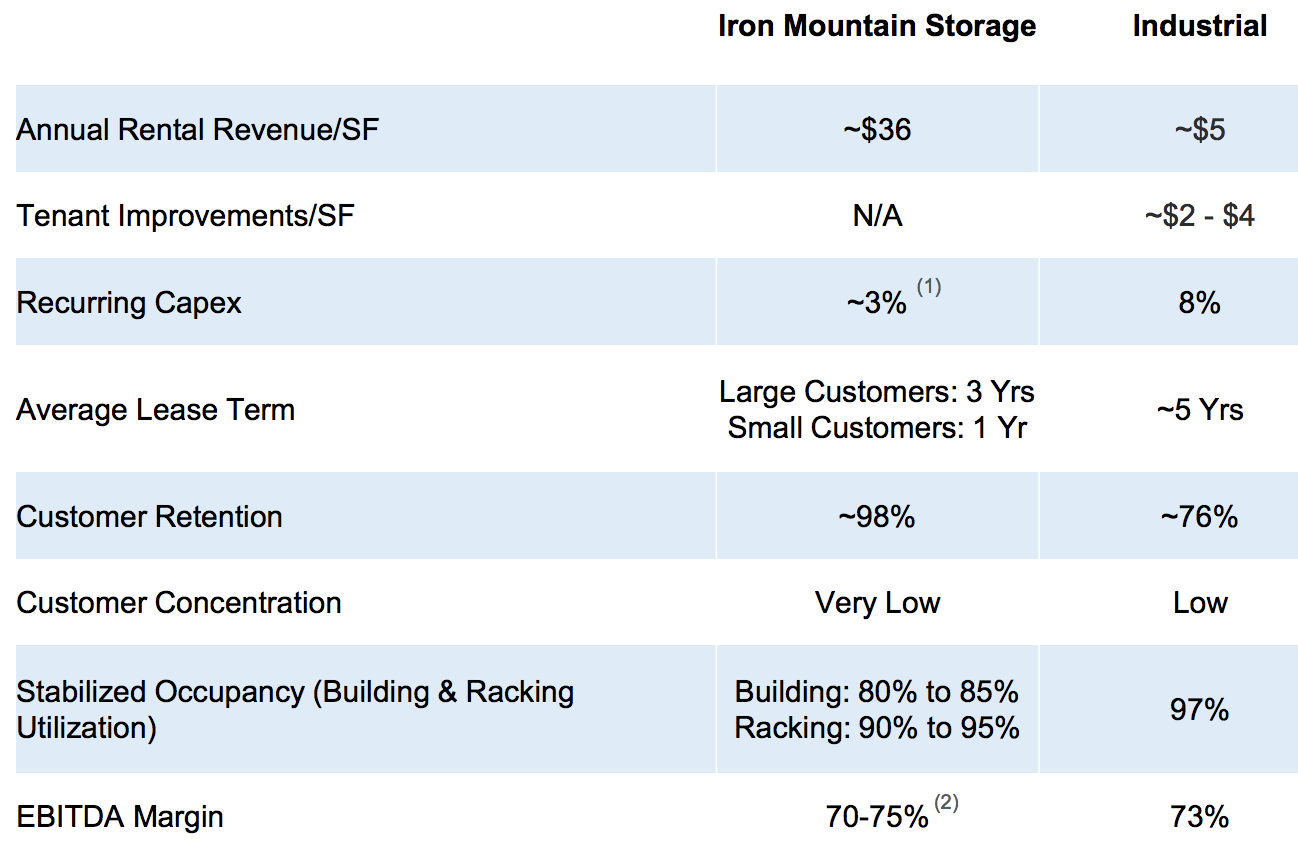

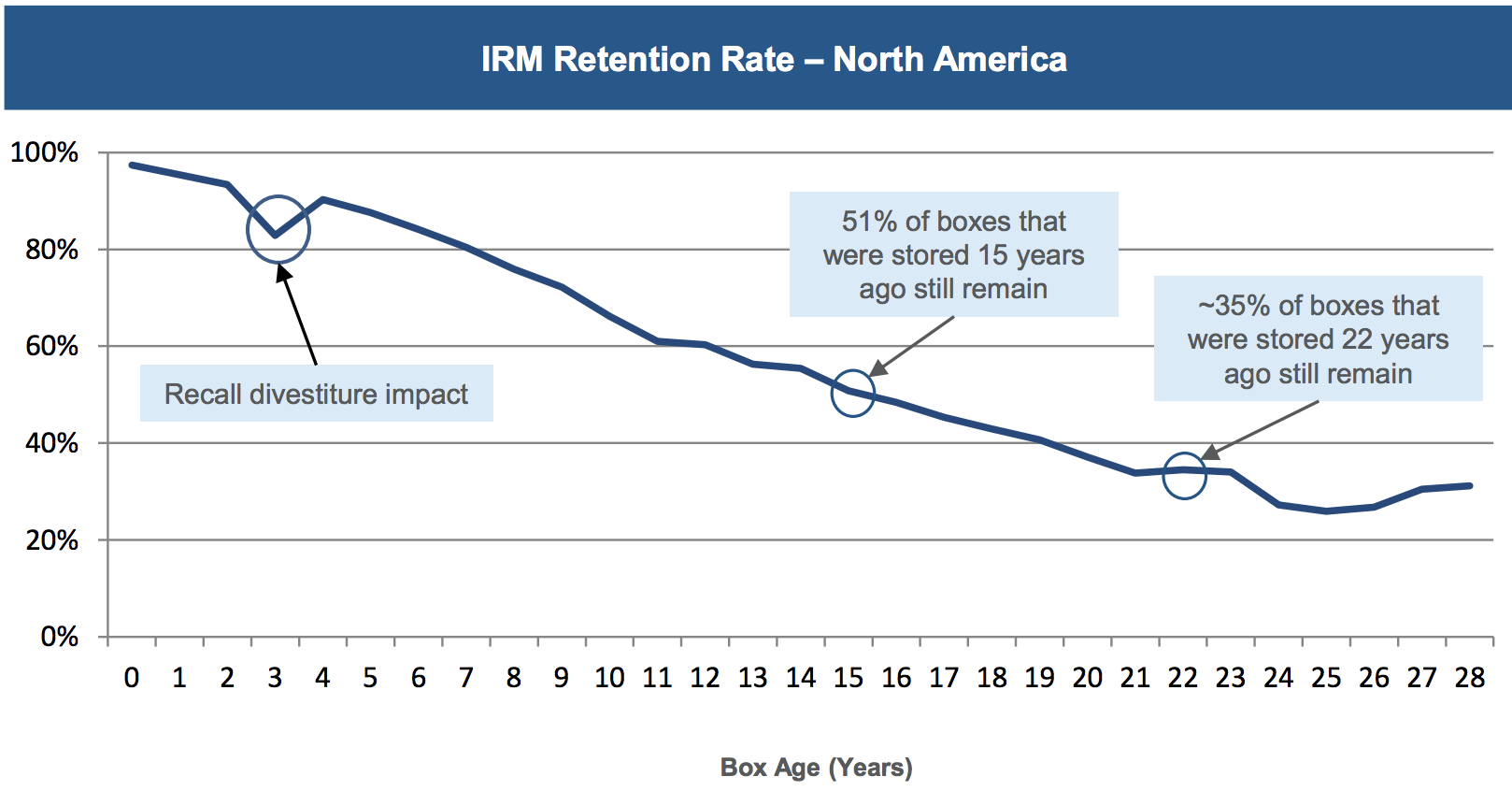

Iron Mountain is a rather unique REIT combining document storage and industrial operations. This allows the company to enjoy strong operating margins, thanks to far higher customer retention (50% of boxes stored 15 years ago remain in IRM's facilities today), low operating expenses (maintenance capex is just 3% of revenue), and healthy pricing power (high rent per square foot).

Iron Mountain stores more than 700 million boxes of physical documents for its customers. Each of those boxes on average generates 25 cents per month and remains with the company for well over a decade, demonstrating the sticky and consistent nature of the business.

When combined with the low costs required to store boxes, Iron Mountain's storage operations, which generate over 80% of its gross profits, enjoy an EBITDA margin near 75%, in-line with most industrial REITs and far higher than regular US corporations.

Source: Iron Mountain Investor Presentation

A key to Iron Mountain's historical success is its industry-leading scale. For example, the REIT has arguably the most advanced and dense logistics network in many of its core developed markets. As a result it can more efficiently collect and transport customer documents to its storage centers than smaller rivals can.

And since the cost of storage is a relatively low part of a client's operating budget, Iron Mountain is able to periodically raise its rents to help offset inflationary costs, due to its short (one- to three-year) lease terms.

When combined with the company's reputation for safety and reliability (sensitive documents are being stored or shredded), plus the cost and hassle associated with changing storage providers, Iron Mountain's clients face relatively high switching costs, which is why the REIT boasts a 98% customer retention rate.

Simply put, clients tend to store physical data and records with Iron Mountain for very long periods. For example, the company's average box age is 15 years, and 35% of its clients' boxes are have been in storage for 22 years or longer.

Source: Iron Mountain Investor Presentation

Since boxes sitting in storage require very little upkeep (unlike apartments or malls), Iron Mountain is able to earn a solid return on capital above 10% in its core North American physical storage business.

Going forward, the REIT plans to continue growing in this important market by continuing to consolidate the industry, which has over 700 million cubic feet of un-vended storage that needs to be served in North America alone. That's compared to Iron Mountain's 680 million cubic feet of North America storage capacity, meaning there seems to be a reasonably long growth runway in the company's most profitable market.

However, Iron Mountain's management is known for its long-term focus and disciplined growth strategy, which has big ambitions beyond North America and developed market document storage.

Iron Mountain has two key growth avenues it's pursuing. The first is international expansion, including in fast-growing emerging markets. Margins in many of these regions are actually higher due to lower construction and acquisition costs. These markets also enjoy a high single-digit organic growth rate, driven by their faster GDP growth and their earlier position in the storage outsourcing game.

However, the biggest and potentially most important growth driver for the REIT is in data centers, which account for 7% of Iron Mountain's total EBITDA today but are expected to generate 10% of the firm's EBITDA by 2020. Iron Mountain made several major data center acquisitions in recent years to continue building a foundation in this space.

The first deal was for Fortrust, in which Iron Mountain paid $138 million for 210,000 square feet of data center facilities in Denver. In 2018 Iron Mountain announced a $1.3 billion purchase of IO Data Centers LLC. This deal included four state-of-the-art data centers in Phoenix, Scottsdale, New Jersey, and Ohio, with average lease lengths of 3.1 years and 98% customer retention rates. The REIT also purchased two data centers serving Credit Suisse's Singapore and London offices, each with 10-year inflation-adjusted leases.

All told, Iron Mountain now has 13 data centers and a presence in nine of the top 10 markets in the U.S. and three of the top 10 international markets. Over time the company plans to continue expanding until it has a strong position in all ten of the top U.S. and global data center markets via bolt-on acquisitions as it's been doing since 2017.

Iron Mountain also plans to invest heavily in the coming years, nearly tripling its overall data center storage capacity organically. In 2019 alone the firm plans to spend $250 million to grow its data center business (for perspective, the firm's annual maintenance expenditures total around $150 million).

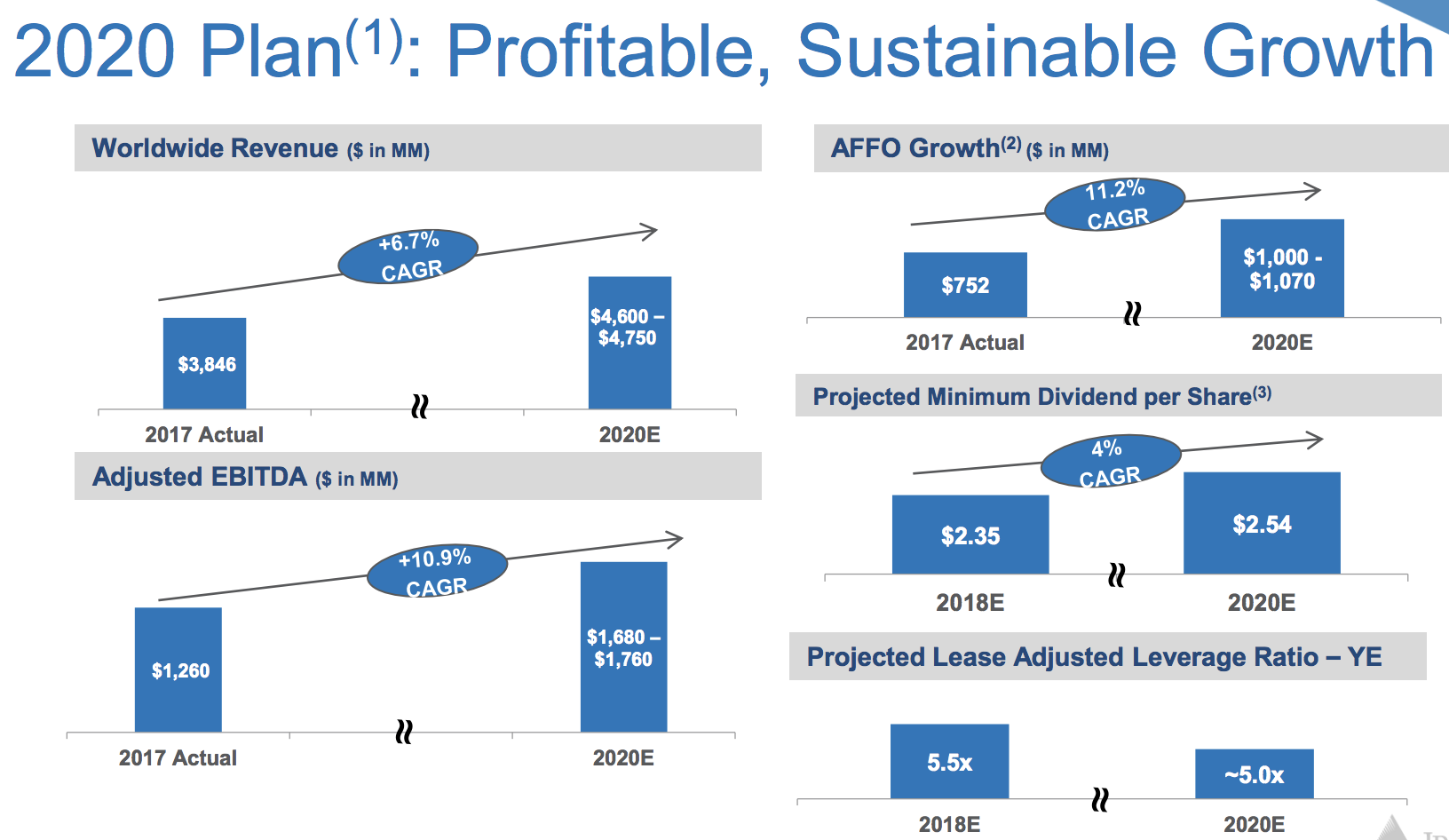

Management believes continued North American storage consolidation, emerging markets growth, and data center expansion will combine to drive double-digit EBITDA growth and about 4% annual dividend growth through 2020.

Source: Iron Mountain Investor Presentation

During this time, management also expects to deleverage the company's balance sheet and hopefully earn Iron Mountain a credit rating upgrade that would lower its future borrowing costs.

By the end of 2020, the REIT wants to hit a leverage ratio of 5.0 and eventually get that down to about 4.75. For now, however, the company's leverage profile is riskier than the average REIT's, earning Iron Mountain a junk credit rating of BB- from Standard & Poor's.

Overall, while Iron Mountain's business may not be the most exciting operation in the real estate sector, its impressive scale, geographic diversification, and sticky storage division appear to make it a predictable source of cash flow that can support a generous and reasonably secure dividend as management invests for faster organic growth.

That being said, like all stocks, Iron Mountain has its fair share of challenges it will have to deal with in the coming years.

Key Risks

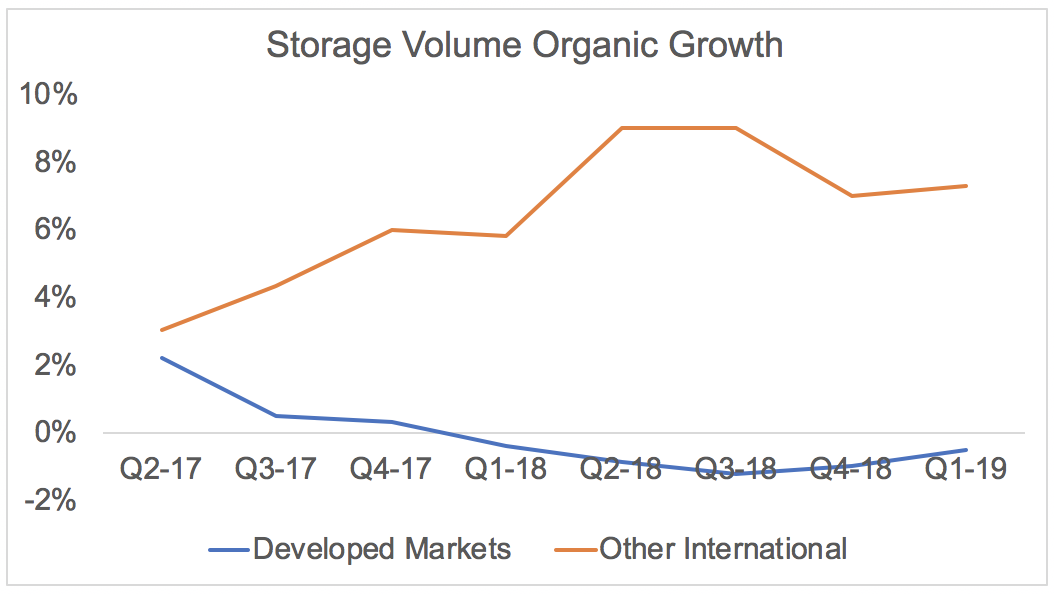

Iron Mountain has become the dominant global player in its core market of physical document storage. However, in developed markets, such as North America and Europe, this is a very slow-growing business that's actually been in decline over the past year.

Source: Iron Mountain, Simply Safe Dividends

Although acquisitions still provide somewhat of a growth runway in developed markets, there is a limit to how much expansion can ultimately be achieved from this profitable core business, especially as more companies move to paperless (i.e. digital) documents.

In other words, Iron Mountain will likely have to depend even more on emerging markets, where its storage volumes continue to rise around 5% to 9% per year and have thus far more than offset the decline in developed markets.

Source: Iron Mountain Supplemental Financial Information

However, eventually, the same switch away from paper might occur in these growth markets as well, putting increased pressure on management to deliver on its data center growth strategy.

The trouble is that Iron Mountain, while having decades-long relationships with the largest companies in the world, is still a relatively new player to data centers. This business competes against industry giants with far more scale and expertise such as Digital Realty Trust (DLR) and Equinix (EQIX). For example, Digital Realty has over 200 data centers compared to Iron Mountain's 13.

Those data center REITs enjoy much lower costs of capital, both due to their more premium stock valuations (higher price-to-cash flow multiples lower their cost of issuing equity) and investment grade credit ratings.

Meanwhile, Iron Mountain's junk bond credit rating means its borrowing costs are higher, raising its cost of capital and making profitable growth more difficult.

While the REIT does not have any meaningful debt maturing until 2023, approximately 31% of its debt has floating floating rates. In other words, Iron Mountain faces higher interest rate risk compared to its peers who mostly issue fixed-rate bonds.

This is one reason why management says deleveraging is a top priority. The REIT wants to minimize its long-term reliance on fickle and volatile equity markets to raise growth capital, while also minimizing the risk of having to refinance debt at potentially higher interest rates or during an economic downturn.

Between 2017 and 2019 management expects to issue 41 million new shares representing about 17% shareholder dilution. While almost all REITs naturally grow their share count over time (due to the requirement of paying out 90% of taxable income as dividends) this can create significant growth headwinds on a cash flow per share (AFFO per share) basis.

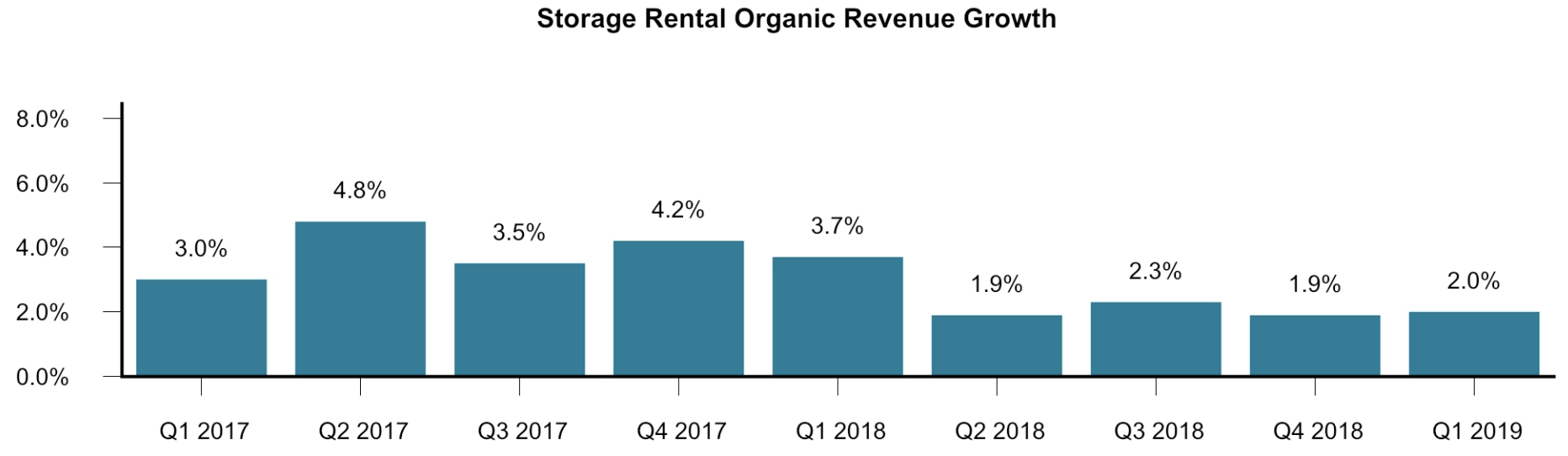

Iron Mountain's first-quarter 2019 earnings report saw the REIT reiterate its 2019 guidance, which calls for just 1 million new shares issued this year (less dilution) but also very modest AFFO per share growth of 2.6% (compared to 8.2% in 2018).

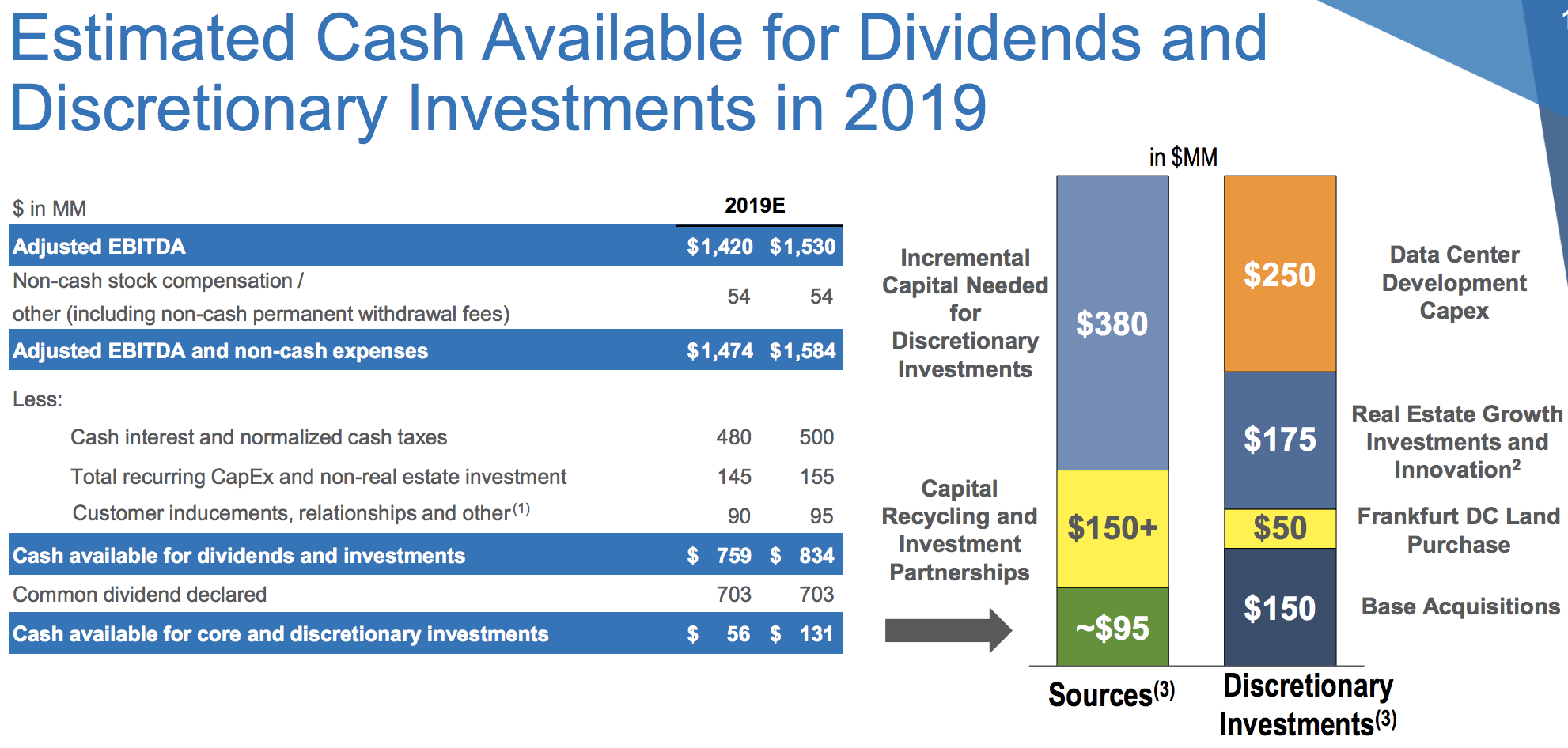

While the firm's AFFO payout ratio is expected to sit near 80%, a reasonably safe level in most cases, that only leaves around $95 million in retained cash flow to fund the REIT's growth plans in 2019, which total $625 million thanks largely to data center investments and acquisitions.

Source: Iron Mountain Investor Presentation

In other words, Iron Mountain is going to have to finance the majority of its growth spending with debt, which makes it harder to hit its long-term deleveraging goals.

In fact, between the third quarter of 2018 and the first quarter of 2019 the REIT's leverage ratio rose from 5.6 to 5.8. While that's not a major increase, it is a step in the wrong direction, which is a concern if it continues.

If management runs into any challenges on execution, then Iron Mountain's dividend may not grow at 4% as planned, in order to lower the payout ratio more quickly and allow management to fund more growth with retained cash flow while minimizing further use of debt.

In fact, in March 2019 Standard & Poor's revised its outlook on the company to stable from negative but stated a rating upgrade was unlikely due in part to Iron Mountain's generous dividend, which limits the firm's financial flexibility:

"We view an upgrade of IRM as unlikely given the company's dividend payout requirements, which reduce its financial flexibility and capital to fund its growth. Issuing equity to reduce its lease-adjusted leverage and demonstrating a commitment to sustaining leverage of comfortably below 5x is the most likely path to an upgrade. Alternatively, we could raise our rating if the company significantly increases the revenue and earnings contribution from its non-paper and tape storage businesses such that it improves our view of IRM's product mix or if it increases its owned real estate value to debt ratio."

The good news for Iron Mountain is that Standard & Poor's raised its adjusted debt to EBITDA leverage ratio threshold for a downgrade to 6.0 from the low-5.0 area. That gives management a little more breathing room as the firm executes on its growth plan, but the stakes are still high.

If its leverage keeps creeping up, perhaps due to growth investments that fail to deliver their expected returns, then Iron Mountain could find itself under greater pressure to protect its credit rating and keep its borrowing costs down.

Reducing the dividend would be one lever management could pull, but for now Iron Mountain seems far away from facing such a situation. Its investments and long-term diversification plan need more time to play out.

With that said, many investors have some concerns about the substantial cash Iron Mountain is pouring into its data center business, which has more challenging economics compared to physical document storage.

Specifically, data centers typically cost far more to purchase, meaning lower cash yields on acquired properties. For instance, Iron Mountain anticipates that it will be able to generate about 11.5% returns on capital from data centers compared to 12% to 14% for its physical storage business. Data center EBITDA margins are also just 50% compared to 70% to 75% in Iron Mountain's storage business.

Due to lower cash yields on acquired new data centers, Iron Mountain may have to rely more on organic investments (building data centers from scratch), which could put it at a disadvantage to its larger competitors. As previously discussed, many of these REITs enjoy lower costs of capital due to their premium share prices and lower borrowing costs.

Basically, the risk is that Iron Mountain will fail to achieve the scale and competitive advantages in data centers that it has in physical storage, dampening its long-term growth outlook (especially if the rise of digital documents starts weighing more on document storage demand its in most profitable developed markets).

While Iron Mountain has a solid core business that produces reliable cash flow, the REIT's sub-investment grade credit rating, high cost of capital, and lack of significant retained cash flow relative to its growth budget reduce its margin for error.

For example, due to its more limited financial flexibility, in 2019 Iron Mountain expects to fund 24% of its growth budget with property sales. However, should an economic downturn occur, impacting the prices Iron Mountain could fetch for its properties, then the firm's long-term growth plans could be disrupted.

Until the company has improved its leverage profile, conservative income investors may want to look elsewhere for yield, sticking with dividend payers which possess stronger balance sheets and better control over their long-term growth plans.

Closing Thoughts on Iron Mountain

Iron Mountain represents a unique investment prospect, a hybrid industrial/storage/data center REIT whose competitive advantages in its core business result in the stable cash flows needed to support a generous dividend.

While there are certainly risks to management's long-term growth and diversification plans, Iron Mountain has adapted to changing industry conditions over the course of many decades. The company has also shown a balanced but shareholder-friendly dedication to conservative payout increases.

Should Iron Mountain make progress deleveraging its balance sheet and see its continued investments in emerging markets, adjacent business opportunities, and data centers bear fruit over the coming years, the company's profile should become more appealing for conservative income investors.

However, dividend investors need to make sure that management executes well, especially in continuing to generate steady cash flow from the firm's core storage business while balancing growth investments with deleveraging. Until Iron Mountain improves its financial flexibility, its margin for error remains lower than many other higher-quality REITs.

While Iron Mountain is not for everyone given its junk bond credit rating and evolving business model, it does appear to be one of the more interesting true high-yielding stocks for investors who are comfortable with its risk profile.