EPR Properties (EPR)

EPR Properties (EPR) is an internally managed REIT that was formed in 1997 and specializes in entertainment and experiential commercial real estate properties. EPR Properties own about $6.2 billion in assets spread across four business segments:

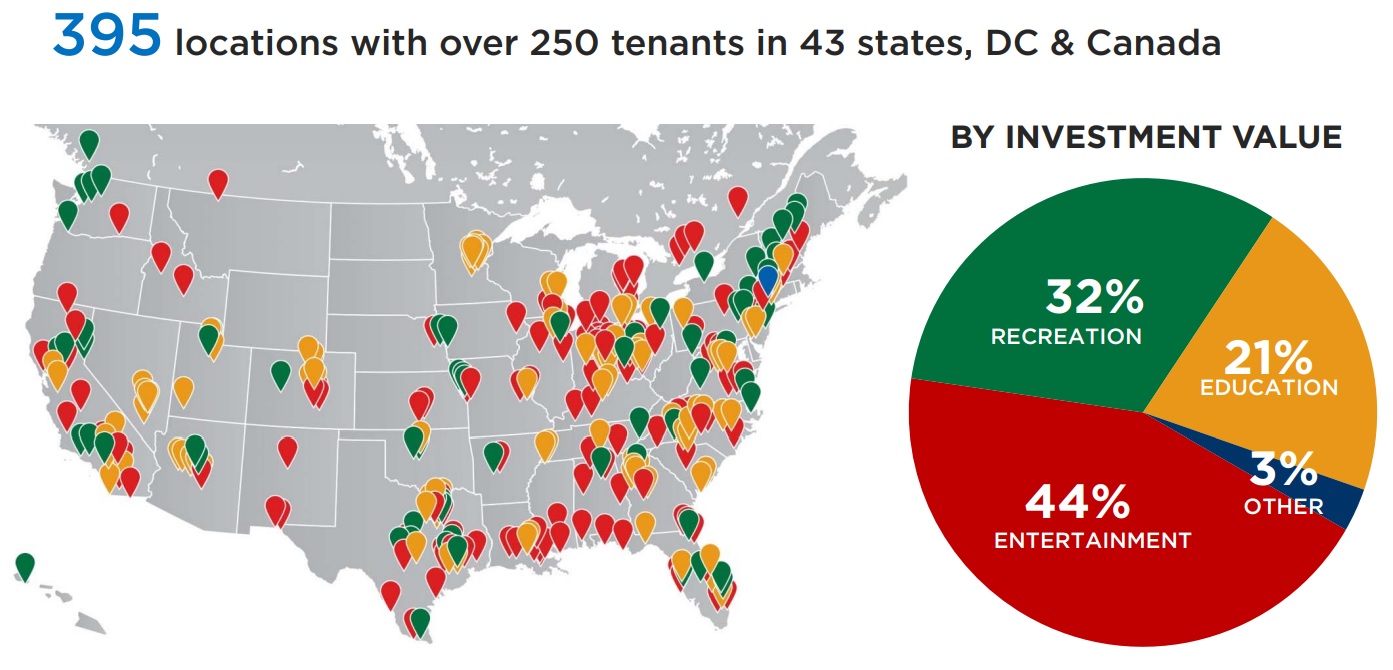

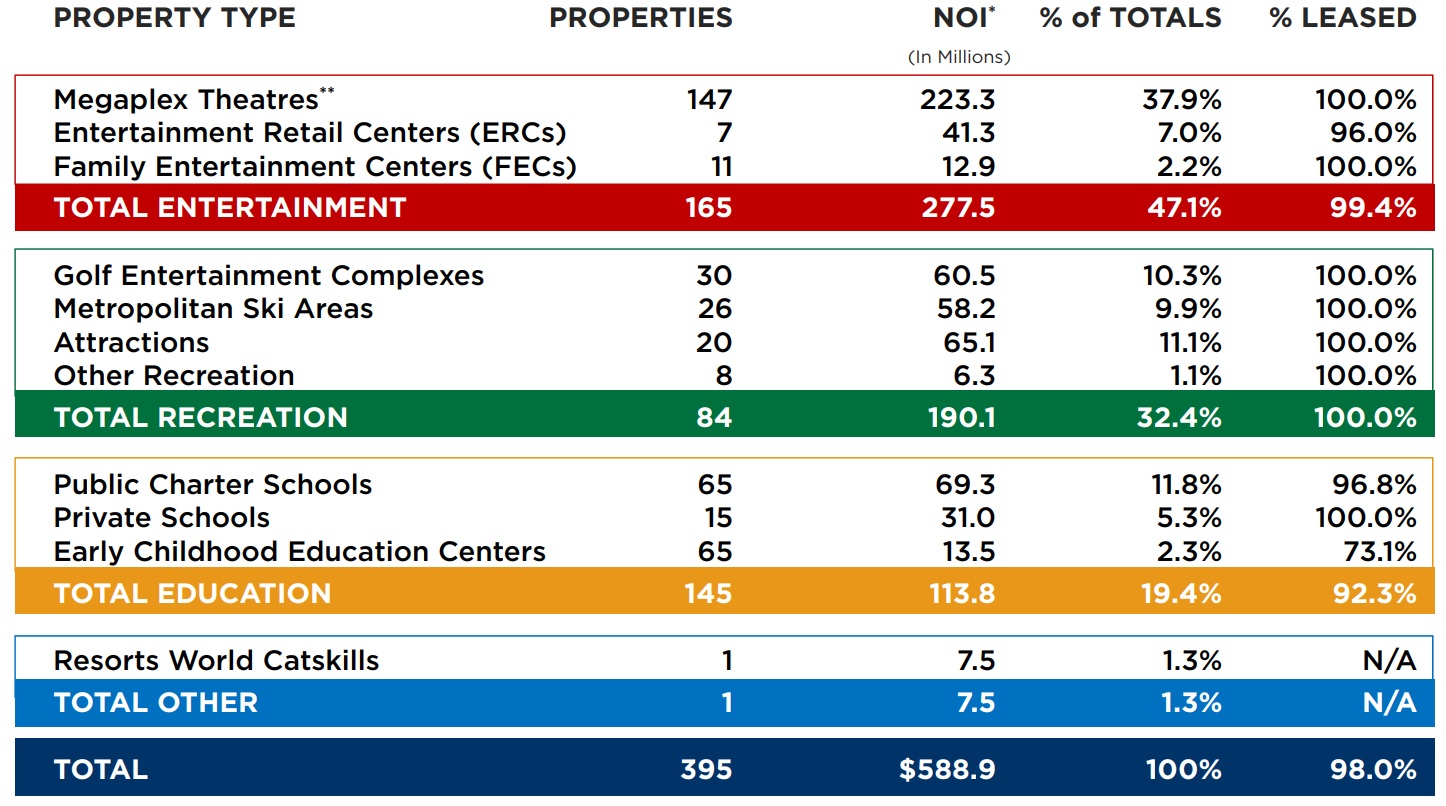

- Entertainment (60% of rent revenue): includes investments in 147 megaplex theatre properties, seven entertainment retail centers (which include seven additional megaplex theatre properties), and 11 family entertainment centers.

- Recreation (27% of rent revenue): includes investments in 26 ski areas, 20 attractions, 30 golf entertainment complexes, and eight other recreation facilities.

- Education (10% of rent revenue): includes investments in 65 public charter schools, 65 early education centers, and 15 private schools.

- Other (2% of rent revenue): consists primarily of the land under ground lease, property under development, and land held for development related to the Resorts World Catskills casino and resort project in New York.

In total, EPR owns 395 properties in 43 states leased to over 250 tenants. The company has another 15 properties representing $258 million in investment under development.

Note that in December 2017 daycare provider Children's Learning Adventure (CLA) filed for bankruptcy. EPR has 25 leases with CLA and is negotiating with the company to see if it could help CLA restructure without evicting it from its current locations. However, there is no guarantee of success so EPR has written off all $9 million of CLA rent, which represents 1.6% of the REIT's total revenue.

Despite this troubled tenant, the REIT's occupancy rate remains very strong at 98%.

Business Analysis

There are three major appeals of EPR Properties that could make it a reasonable long-term, high-yield income investment.

First is the nature of the business model. EPR Properties specializes in triple net leases, which represent 86% of its properties. Under this structure, EPR will buy a new property and then lease it back to the former owner (now a tenant) under very long-term and inflation-adjusted rental agreements.

In fact, EPR's average remaining lease term is 12.5 years in duration, and over the next decade leases representing just 2.9% of annual rent will be expiring. As long as its tenant are financially healthy enough to meet their rent obligations, EPR should enjoy extremely consistent and recurring cash flow from which to fund its dividend.

In addition, because triple net leases require the tenant to pay maintenance, taxes, and insurance costs, the rent EPR generates is extremely profitable. For example, its adjusted funds from operation, or AFFO (similar to free cash flow for a REIT), margin was 64% in 2017.

Importantly, EPR's tenants are mostly high-quality businesses, with even its cinema properties sporting tenant rental coverage ratios (operating cash flow/rent) of 1.6. Most of the company's recreation and education properties have even higher ratios near 2.0, and the weighted average REIT-level tenant coverage ratio is 1.7. For context, a ratio over 1.3 is generally considered safe in this industry.

The firm's high coverage ratio is largely due to management' disciplined acquisition strategy. Specifically, EPR tries to only acquire properties with financially strong tenants who are unlikely to have trouble covering rent or the lease's inflation-adjusted annual escalators (indexed to CPI and capped at 2%).

For example, EPR currently owns about 3% of the nation's movie theaters. However, these locations generate 7% of total cinema revenue, due to the REIT's disciplined approach to buying only high-quality, growing assets.

For example, EPR currently owns about 3% of the nation's movie theaters. However, these locations generate 7% of total cinema revenue, due to the REIT's disciplined approach to buying only high-quality, growing assets.

EPR is also very disciplined about not growing its dividend too quickly but instead ensuring that the current payout remains sustainable. As a result, the company maintains a conservative 80% AFFO payout ratio, which is lower than the level reported by most triple net lease REITs. This provides greater cushion in the event of an economic downturn and allows EPR to retain about 20% of its internally generated cash flow to reinvest in growth opportunities.

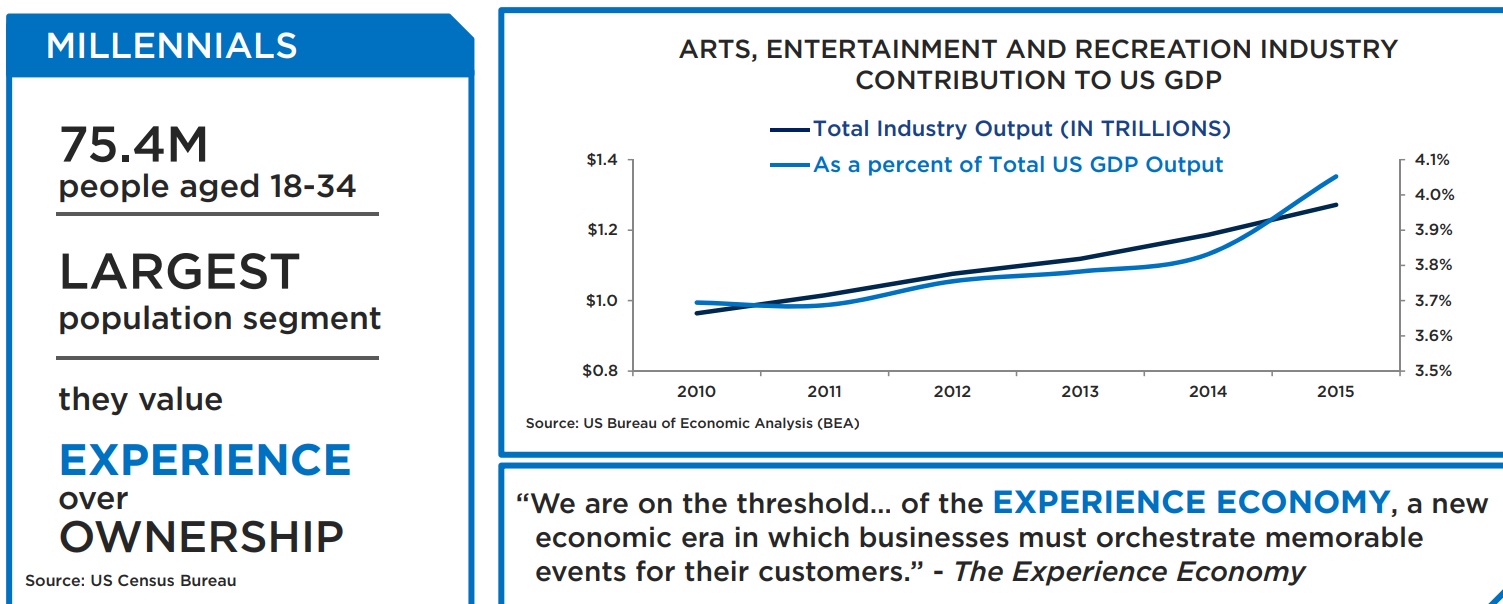

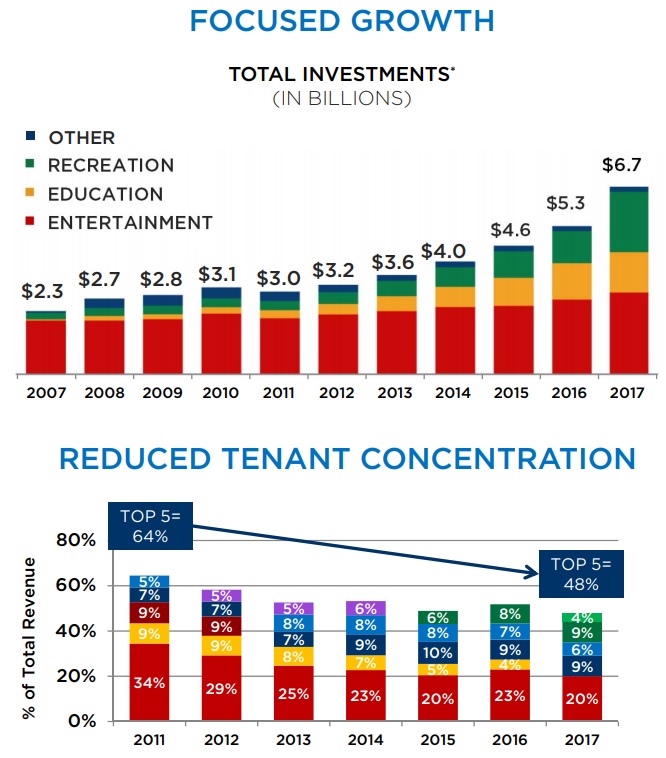

The second reason EPR Properties could be an appealing investment is the large growth runway created by two favorable trends. First, most of the company's properties are focused on the growing popularity of experiential retail. Millennials, now the largest generation in U.S. history, prefer to spend money doing things rather than buying things. This is one reason why the share of consumer spending going to arts, entertainment, and recreation has been steadily rising over time.

Another trend the REIT is targeting is private education, specifically: charter schools, private schools, and early childhood education centers. Management estimates that these three industries represent about $5.5 billion in potential future growth opportunities.

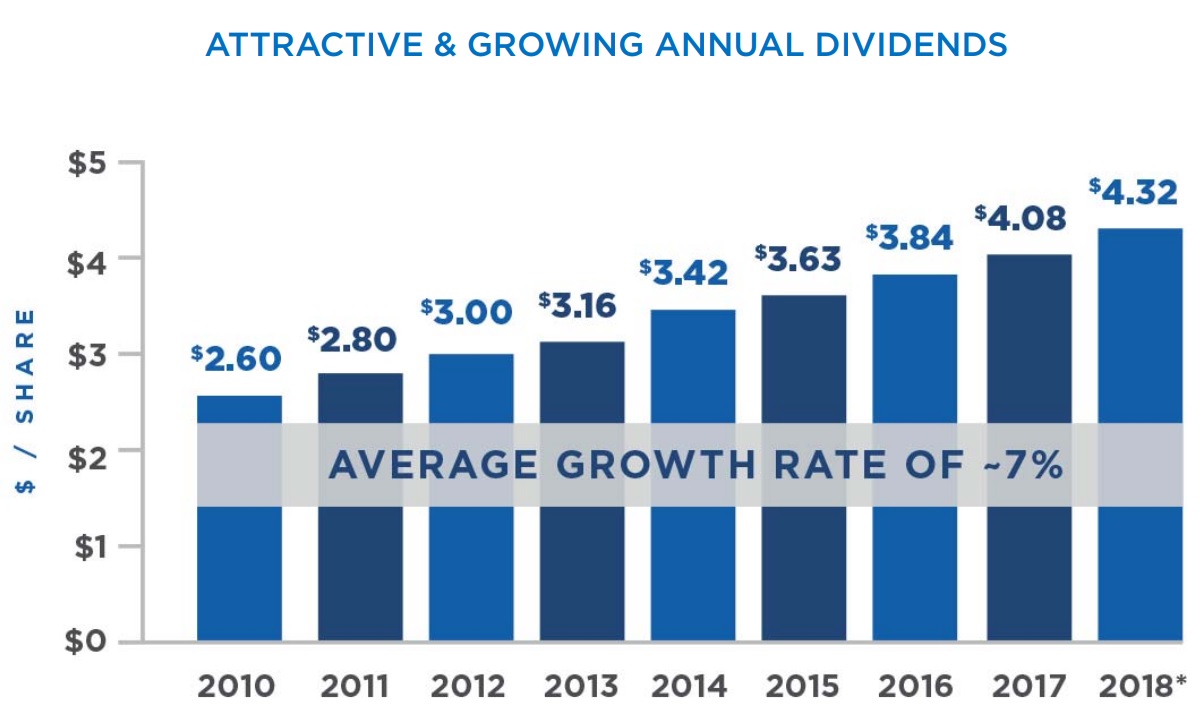

To put that in context, EPR Properties has only invested a total of $6.7 billion in total through its entire 20-year tenure as a REIT. Those investments were made to grow AFFO per share, (7% annual growth since 2010) and diversify its tenant base to create a safer cash flow stream.

Management's selective investments have allowed EPR's dividend (paid monthly) to rise 7% annually, in line with AFFO per share growth. Again, that aligned growth allowed EPR to maintain an 80% payout ratio, balancing dividend growth with reasonable safety while retaining enough cash to keep growing.

For 2018, management raised the dividend 6% and is guiding for 6% AFFO per share growth. Over the long term, investors can likely expect mid-single-digit payout growth from EPR.

The final main appeal of EPR is its disciplined use of debt, which is critical for successful long-term REIT investing. Acquiring real estate is a very capital intensive activity, and the tax code also requires REITs to pay out at least 90% of their taxable income as dividends, resulting in relatively large debt loads to finance their growth.

However, EPR's leverage ratio (debt/Adjusted EBITDA), is beneath the industry average of 6.0 and has been relatively stable over time. Management has a target leverage range of 4.6 to 5.6 to ensure the firm maintains its investment-grade credit rating and has ongoing access to low cost borrowing. Approximately 90% of EPR's debt also has fixed rates, minimizing the firm's interest rate sensitivity and locking in the profitability of real estate assets purchased with those funds.

However, EPR's leverage ratio (debt/Adjusted EBITDA), is beneath the industry average of 6.0 and has been relatively stable over time. Management has a target leverage range of 4.6 to 5.6 to ensure the firm maintains its investment-grade credit rating and has ongoing access to low cost borrowing. Approximately 90% of EPR's debt also has fixed rates, minimizing the firm's interest rate sensitivity and locking in the profitability of real estate assets purchased with those funds.

Besides reasonably conservative leverage ratios, the REIT also has no significant debt maturing until 2020.

Simply put, EPR Properties appears to be a well-managed triple net lease REIT and has an impressive growth rate given its niche in the industry. Management's conservative use of debt, disciplined dividend growth, and focus on healthy tenants with reasonable rent coverage ratios suggest EPR Properties has the potential to be a solid long-term income investment.

However, there are some key risks that could ultimately threaten the REIT's future dividend growth potential, or possibly even its security.

Key Risks

There are two major risk factors to consider for virtually any REIT, including EPR Properties.

The first is tenant concentration and health. After all, no matter how profitable long-term leases may be, EPR's rent revenue could be disrupted and potentially have to be totally written off if a tenant goes bankrupt.

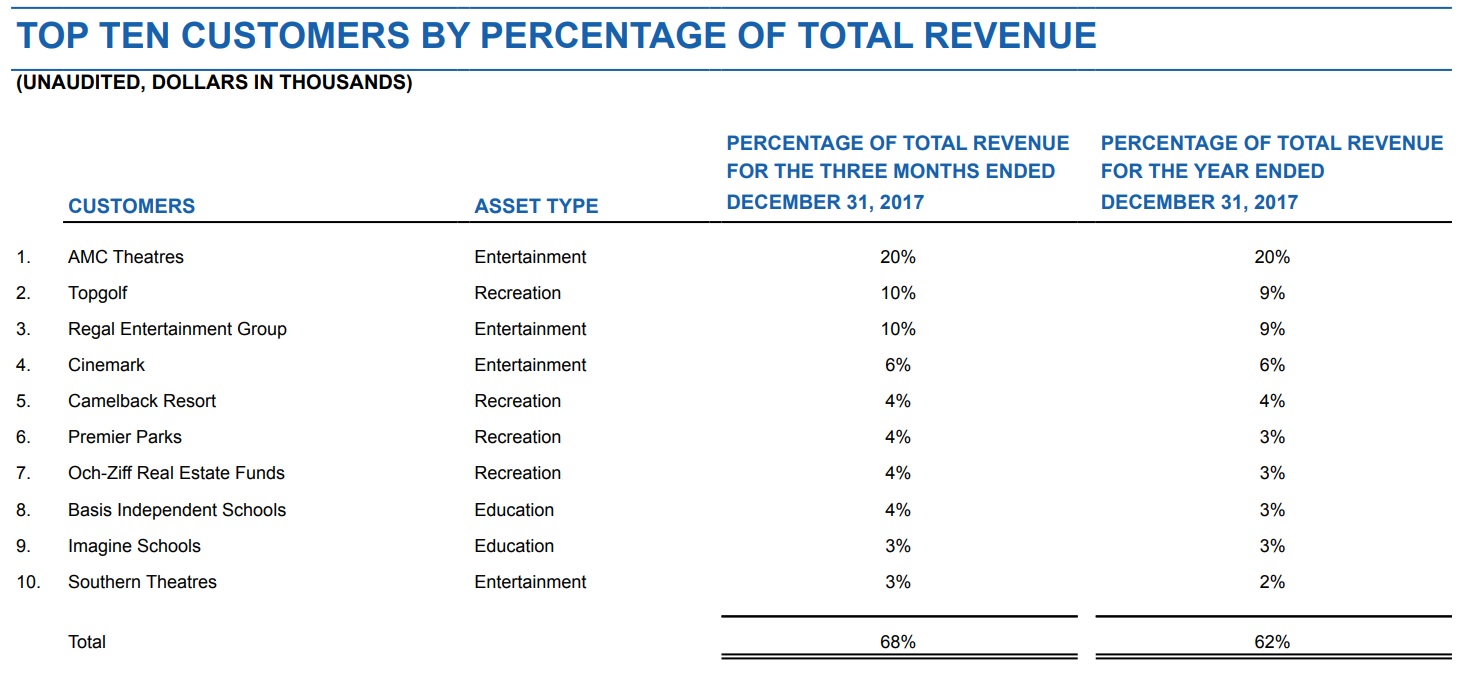

While EPR has been diversifying over time, the company's tenant base remains highly concentrated, with 68% of rent coming from its top 10 customers.

While EPR has been diversifying over time, the company's tenant base remains highly concentrated, with 68% of rent coming from its top 10 customers.

Over 35% of rent is from the largest U.S. theater chains, which are currently struggling with declining traffic.

The good news is that the actual properties owned by EPR are in high traffic urban areas with theaters that are still performing reasonably well and even enjoyed a solid 1.6 tenant coverage ratio in 2017. However, theater attendance has been struggling for several years as streaming continues taking share.

AMC, EPR's largest customer (20% of revenue), saw its U.S. and international attendance decline 2.9% and 2.0% in 2017, respectively. Theater attendance hit its lowest level since 1995 last year, according to data from the National Association of Theatre Owners cited by The Wall Street Journal.

Only steadily rising ticket and concession prices have been keeping theater chains in relatively good financial health. However, there is likely a limit to how high these prices can go before negatively affecting customer traffic. As a result, the U.S. theater industry will have to rely on increasing the premium nature of the cinema experience, such as with luxury seating and more premium food options, in order to continue growing its cash flow. None of these upgrades are cheap, which could further strain movie theaters' financial health.

The good news is that the actual properties owned by EPR are in high traffic urban areas with theaters that are still performing reasonably well and even enjoyed a solid 1.6 tenant coverage ratio in 2017. However, theater attendance has been struggling for several years as streaming continues taking share.

AMC, EPR's largest customer (20% of revenue), saw its U.S. and international attendance decline 2.9% and 2.0% in 2017, respectively. Theater attendance hit its lowest level since 1995 last year, according to data from the National Association of Theatre Owners cited by The Wall Street Journal.

Only steadily rising ticket and concession prices have been keeping theater chains in relatively good financial health. However, there is likely a limit to how high these prices can go before negatively affecting customer traffic. As a result, the U.S. theater industry will have to rely on increasing the premium nature of the cinema experience, such as with luxury seating and more premium food options, in order to continue growing its cash flow. None of these upgrades are cheap, which could further strain movie theaters' financial health.

There is a real chance that higher prices relative to alternatives available at home, such as streaming TV and movies, might ultimately put some theater chains out of business. In such a scenario, EPR would likely be hard-pressed to quickly find a replacement tenants for its theaters, since they are highly specialized and could only be re-leased to other theater owners.

Since these rival chains might also be struggling, there is no assurance that EPR would be able to maintain pricing power but might have to accept drastically reduced rents that could negatively impact its cash flow.

Since these rival chains might also be struggling, there is no assurance that EPR would be able to maintain pricing power but might have to accept drastically reduced rents that could negatively impact its cash flow.

The other major risk to consider is a REIT's access to low cost growth capital. REITs are required by law to distribute 90% of taxable income as dividends, meaning that most REITs retain relatively little cash flow to invest in future growth.

In the case of EPR, the company usually retains about 20% of AFFO but must raise the rest of its growth capital from debt or equity markets. Historically, EPR has split its capital needs down the middle, funding about 40% of growth capital with debt and another 40% with equity (selling new shares).

However, issuing new shares raises the cost of the dividend and dilutes existing investors. In order for a REIT to grow profitably, its cost of capital must be below the cash yield on invested capital it earns on its acquired properties. If the spread is positive, then the new cash flow from investments will cover both interest and dilution, and AFFO per share will rise over time, allowing for continued dividend growth as well.

But if a REIT's share price is too low, then its cost of equity rises, potentially making new growth unprofitable. EPR's share price has struggled over the past year, pushing up its cost of equity capital to levels that leave the firm with a much narrower investment spread.

This is likely why management's guidance for 2018 calls for far slower growth in the company's property base. For example, EPR has revised down investments for 2018 from $750 million to $550 million, and raised its expected asset sale guidance from $175 million to $400 million. In other words, EPR will go from $1.4 billion in net investments in 2017 to just $150 million in 2018.

The slowdown is primarily due to EPR's share price being so low as to force management to fund much of 2018's investments with proceeds from assets sales. This limits how much extra external capital needs to be raised in debt and equity markets.

EPR could theoretically borrow more, since debt costs far less than equity. However, management wants to preserve the company's investment-grade credit rating (BBB- with stable outlook from all three rating agencies). Therefore, EPR must still balance debt issuances with equity issuances to keep its debt metrics roughly the same as they are today.

Should interest rates rise in the coming years, EPR's borrowing costs are likely to increase as well. Maintaining a good credit rating becomes ever more important to ensure the REIT can continued funding growth while maintaining a safe dividend.

The good news is that rising interest rates will also likely push up cash yields on new properties which should help the REIT continue finding profitable growth opportunities. However, management believes there is a three to nine month lag between when interest rates increase and cash yields on new acquisitions start increasing.

In other words, EPR's growth potential, while meaningful over the long term, is not fully within management's control over shorter periods of time. EPR's heavy reliance on debt and equity markets for growth capital means that should interest rates rise too high, and its share price remain too low, the REIT might have to start retaining more AFFO to fund growth internally.

While that would preserve the safety of the dividend by lowering EPR's payout ratio, it would also translate into slower cash flow and dividend growth that could further disappoint investors.

In addition, it should be noted that EPR, like many REITs, did cut its dividend during the financial crisis. The cut wasn't due to dangerous amounts of leverage or a dangerous decline in AFFO per share. Rather the collapse of credit markets caused management to decide to retain more cash flow just in case.

So while EPR's dividend is likely to remain safe during a regular recession, another financial crisis could lead to a dividend cut if credit markets face a similar meltdown, especially if the movie theater industry finds itself on even shakier ground.

Closing Thoughts on EPR Properties

EPR has many of the hallmarks of a potentially solid triple net lease REIT. The company benefits from high occupancy, relatively strong tenants, and long-term leases. Management also has a proven track record of profitably investing in niche but fast growing industries while staying committed to highly disciplined acquisitions and use of debt.

However, concerns over the future health of the movie theater industry, high tenant concentration, and growing risks of a liquidity trap that cuts off its growth potential mean that EPR Properties is still a somewhat riskier stock, despite the safety of its payout today. As a result, EPR might not be suitable for conservative investors and should only be considered as part of a well-diversified income portfolio.