SJW Group (SJW)

Founded in 1866 as the San Jose Water Company, SJW (SJW) is a regulated water utility that serves customers in two fast-growing markets: Silicon Valley, California, and San Antonio, Texas.

The company’s two primary business units are San Jose Water and SJWTX, which owns the Canyon Lake Water Service Company.

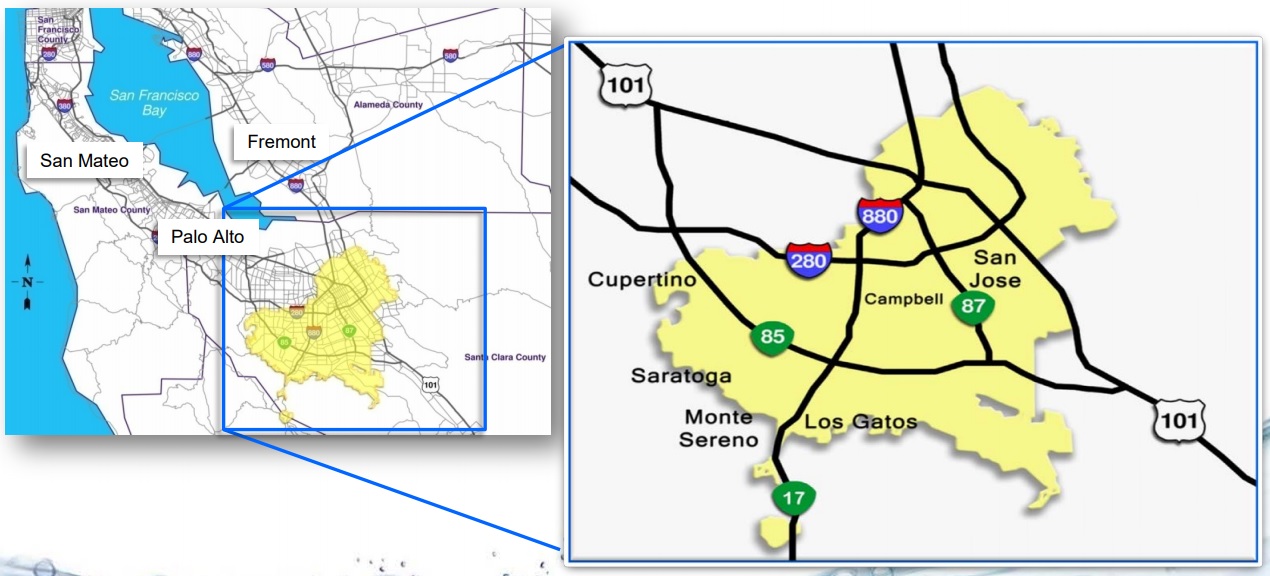

San Jose Water’s 111 wells, 2,400 miles of water mains, and two water treatment plants service 230,000 connections. This segment provides water to approximately 1 million people (about 33% of the population) in Silicon Valley, with a total capacity of over 280 million gallons of water per day.

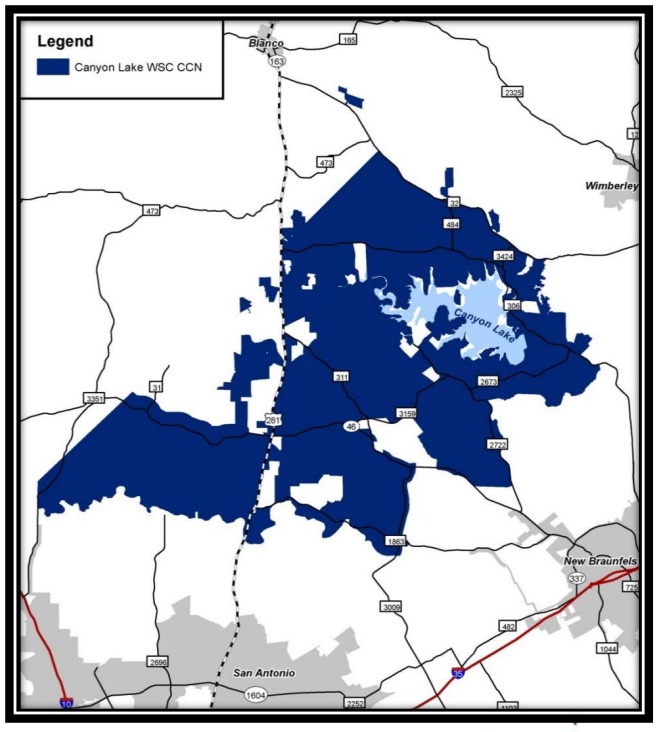

Meanwhile, Canyon Lake Water’s 42 wells, 599 miles of water mains, and three treatment facilities provide up to 9 million gallons a day to 14,000 connections (serving 42,000 people) across central Texas, located between San Antonio and Austin.

The company also has a small real estate arm, SJW Land Company, which owns undeveloped land and operates commercial buildings in the states of California and Tennessee.

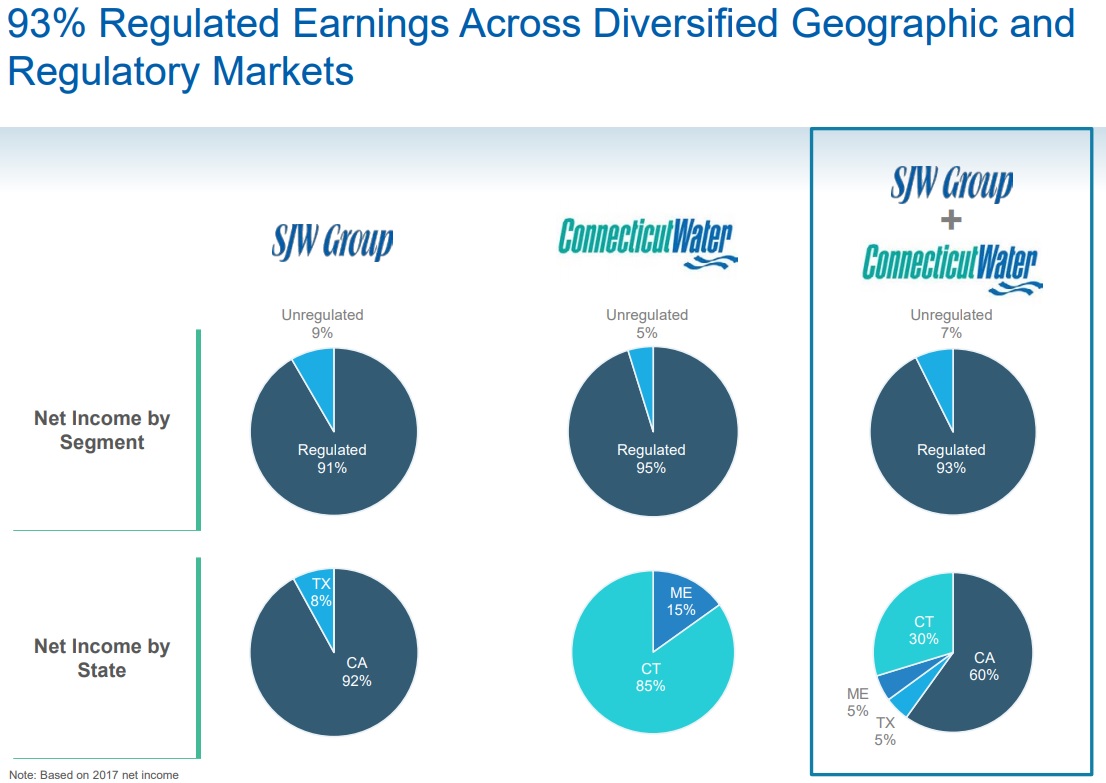

In 2017, 98.5% of SJW’s revenue came from its regulated water businesses, with $5.7 million generated by its land business subsidiary. The land business is used purely to help fund the core regulated utility business.

In 2017, 98.5% of SJW’s revenue came from its regulated water businesses, with $5.7 million generated by its land business subsidiary. The land business is used purely to help fund the core regulated utility business.

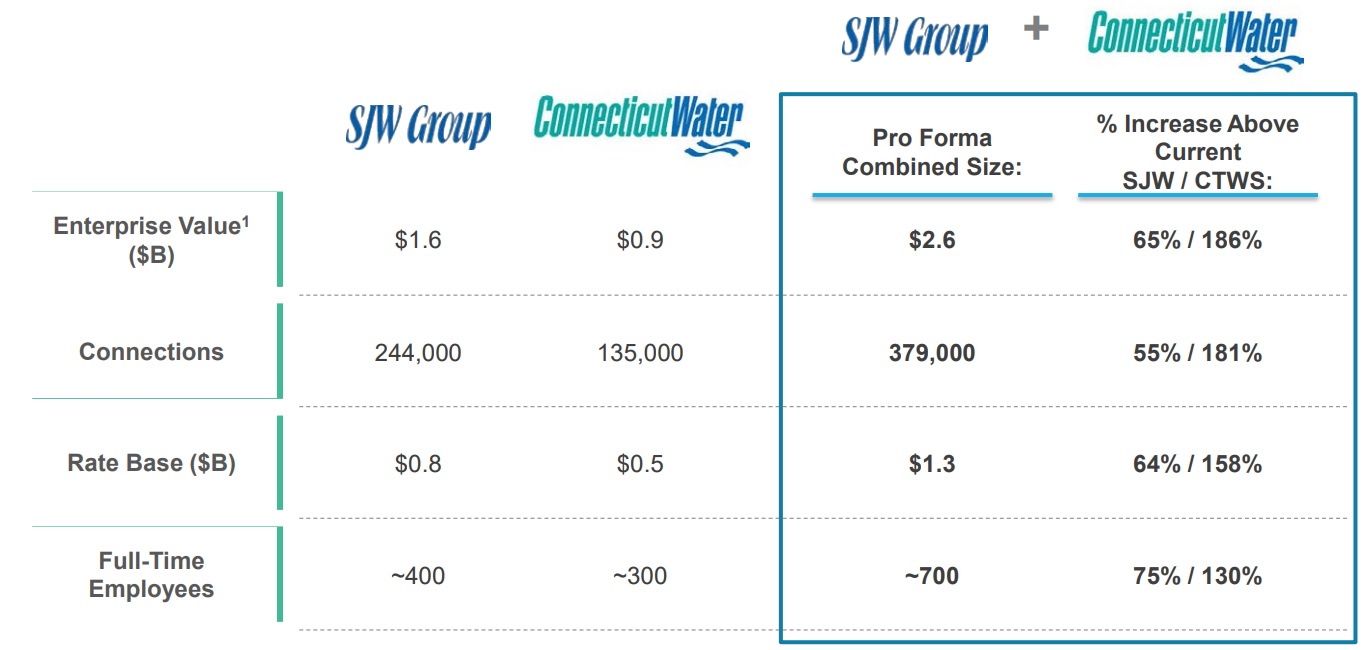

In March 2018, SJW and Connecticut Water Service (CTWS) agreed to a $1.9 billion all stock merger. Upon closing (expected by end of 2018), this deal will make SJW America's third-largest publicly traded water utility with 1.5 million customers in four states: California, Texas, Connecticut, and Maine. SJW shareholders will own about 60% of the combined company.

With 50 consecutive years of dividend increases under its belt, SJW is a dividend king.

Business Analysis

Water utilities are the ultimate defensive businesses. That's because they are regulated monopolies with locked in customer bases and government regulated returns on equity. In other words, they sell essential products to a captive base of customers at guaranteed rates of return, which creates extremely stable cash flow and very steady earnings growth. As a result, many water utilities have some of the longest and most consistent consecutive annual dividend growth streaks in America (50 years for SJW, 48 years for Connecticut Water).

However, the downside of the water utility business is that it's a very slow growing industry. Companies add new connections on existing assets (municipal water systems) as the population grows. In addition, companies can acquire other water systems (there are about 160,000 in the U.S.). The problem is that most of these consist of just a few thousand connections (new customers), meaning that sales and earnings growth in this industry is very slow (usually low to mid-single-digits).

SJW has managed to achieve some of the industry's fastest growth, compounding its revenue and earnings per share by 8.3% and 12.8%, respectively, over the past five years. Two main factors are behind the company's success.

First, the utility operates in constructive regulatory environments characterized by government bodies allowing SJW to earn above industry average returns on capital. That's because SJW primarily operates in growing regions where relatively fast population growth and a large need for improving and expanding water infrastructure result in regulators approving and encouraging more large-scale investments.

First, the utility operates in constructive regulatory environments characterized by government bodies allowing SJW to earn above industry average returns on capital. That's because SJW primarily operates in growing regions where relatively fast population growth and a large need for improving and expanding water infrastructure result in regulators approving and encouraging more large-scale investments.

However, in recent years Silicon Valley's population growth has slowed to a crawl and threatens to even reverse in coming years. That's because home prices are rising so quickly (nearly 30% in the past year due to a massive undersupply in new home construction) that many people simply can't afford to move to San Jose or continue living there (rents are also skyrocketing). So SJW needed a major growth boost which is why it decided to merge with Connecticut Water Systems.

There are three main reasons the company is combining with Connecticut Water Systems. First, the deal will significantly increase SJW's size with the firm gaining 55% more water connections and a 62% larger rate base. The combined company should operate more efficiently thanks to its greater scale.

The second big reason for the merger was to diversify its markets away from just two states. The new SJW will now operate in four states, California, Texas, Maine, and Connecticut, were it will serve 1.5 million customers. As a result, SJW should be less sensitive to unfavorable developments in any of its regions (e.g. a drought in California) and have more opportunities to acquire smaller rivals across its larger network of service territories.

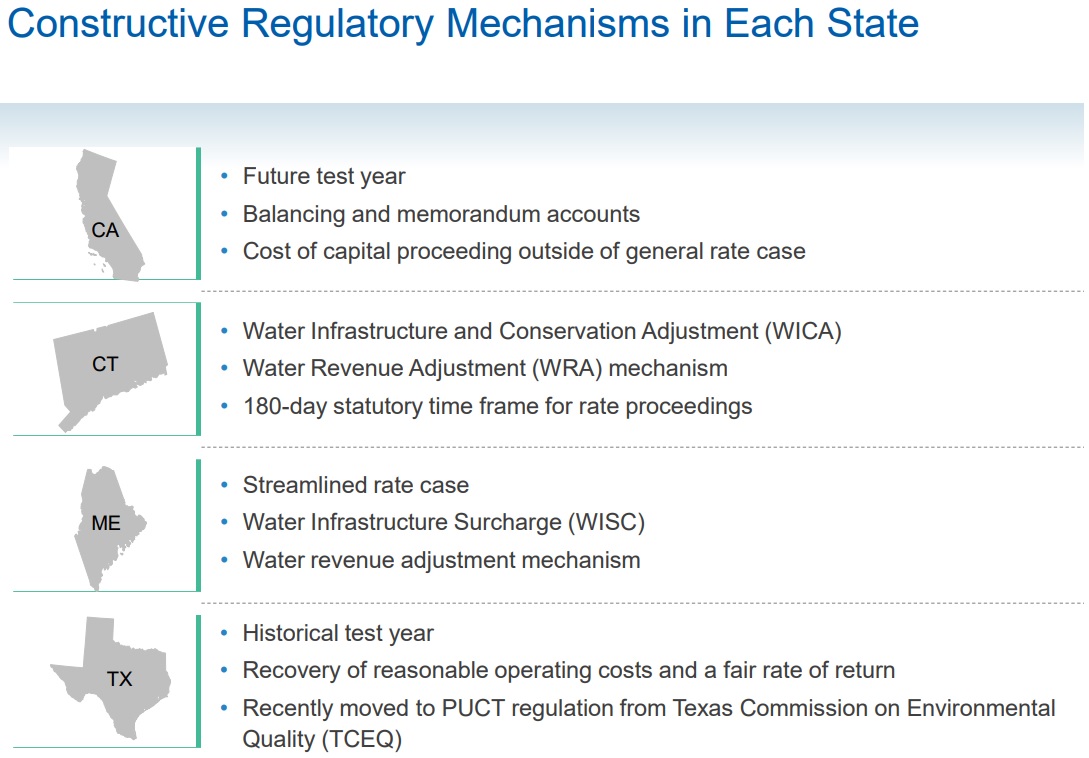

Importantly, all of its key markets have favorable regulatory environments. This means above-average returns on capital as well as favorable regulatory mechanisms that streamline the investment approval process and how fast the company can recoup its investments.

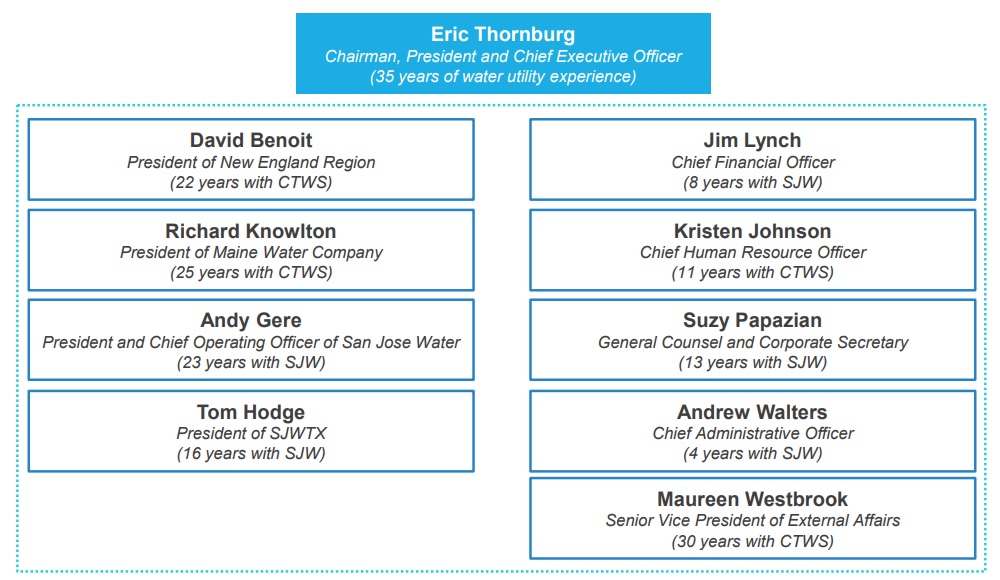

To ensure the merger goes smoothly (and positive relationships with regulators continue), the combined company will be led by one of the industry's most experienced management teams. All told, the top 10 executives have a combined 152 years of industry experience between them.

The merger with Connecticut Water Systems should also help to improve the company's already-strong balance sheet. In fact, management expects that the combined company will enjoy Connecticut Water Systems' current "A" credit rating. This should allow it to borrow at lower long-term fixed rates and improve its already impressive economies of scale (for such a small utility).

Once the merger closes, the new SJW should see a 25% boost to revenue and a 30% increase in net income. The combined company will also enjoy a slightly higher net margin near 15%, which is more than double the industry average. The deal is expected to be immediately accretive to SJW's EPS and over the next few years boost EPS by the low to mid-single-digits once synergistic cost savings are achieved.

Another benefit of the merger is that Connecticut Water is a much faster-growing company. For example, analysts expect SJW and CTWS to grow their earnings at annual rates of 4.5% and 7.6%, respectively, over the next decade. The combined company has an expected long-term growth rate of 5.7%, which is higher than SJWs previous growth forecast. That's thanks to a combined approved growth capex budget of approximately $650 million over the next three years. That will grow the company's rate base by about 50% and ensure strong earnings growth for years to come.

While all long-term growth projections must be taken with a grain of salt, modeling utility growth rates is usually more accurate given the predictability of the business model. The faster growth rate of the bigger SJW should allow it to continue growing its dividend at least as fast as its historical pace of 4% annually over the last 20 years. Dividend growth along the lines of 5% to 6% per year, in line with EPS growth, is a definite possibility, especially over the next few years as SJW's large backlog of growth projects comes online.

However, while SJW's dividend growth record is impressive, and the Connecticut Water merger will make it a much more diversified and faster-growing company, there are still several risks to keep in mind.

Key Risks

The biggest risk stems from the highly regulated nature of this business. In its largest market (even post-merger), the California Public Utilities Commission (CPUC) re-adjusts the rates SJW can charge its California customers every few years. SJW has usually been on friendly terms with its regulators. For example, in 2017 the CPUC granted the company's $13.2 million rate base increase (3.8% price hike).

However, when considering the company's 2.8% proposed increase for 2018, the CPUC has been far less friendly. Specifically, the CPUC is proposing to lower the company's allowed return on equity and return on base rate from 9.4% to 8.3% and from 8.1% to 7.2%, respectively. If the CPUC decides to go with the lower rate, then SJW faces a $10 million decrease in revenue that will largely offset its 2017 price increase.

However, when considering the company's 2.8% proposed increase for 2018, the CPUC has been far less friendly. Specifically, the CPUC is proposing to lower the company's allowed return on equity and return on base rate from 9.4% to 8.3% and from 8.1% to 7.2%, respectively. If the CPUC decides to go with the lower rate, then SJW faces a $10 million decrease in revenue that will largely offset its 2017 price increase.

In Texas, the Public Utilities Commission of Texas (PUCT), authorizes base rate increases anytime SJW requests it, no more than once every 12 months. Meanwhile, the company must deal with numerous other regulators at both the state and federal level including the EPA and various state environmental agencies to receive approval to expand its asset base.

And after the merger closes, SJW will also have to deal with the Connecticut Public Utilities Regulatory Authority and the Maine Public Utilities Commission. While in general the company enjoys a constructive relationship with its regulators, as we saw with the latest CPUC proposed rate case, sometimes regulators can lower the firm's allowed returns on capital.

And after the merger closes, SJW will also have to deal with the Connecticut Public Utilities Regulatory Authority and the Maine Public Utilities Commission. While in general the company enjoys a constructive relationship with its regulators, as we saw with the latest CPUC proposed rate case, sometimes regulators can lower the firm's allowed returns on capital.

However, even when regulators are willing to give SJW a good return on equity and rate bases, there are some other regulatory risks that investors need to be aware of. During the recent California drought, the CPUC, which regulates all water utilities in the state, imposed 30% reductions in volumes. This was later reduced to 20% and then recently lifted due to greater rainfall.

However, on May 31, 2018, Governor Jerry Brown signed two bills into law which orders the States Water Resource Board to maintain the current 55 gallon per person per day limit. That will be reduced to 50 gallons per day by 2030 but shows that changing hydrological conditions in its key market in San Jose has the potential to decrease SJW's growth rate in the future.

However, on May 31, 2018, Governor Jerry Brown signed two bills into law which orders the States Water Resource Board to maintain the current 55 gallon per person per day limit. That will be reduced to 50 gallons per day by 2030 but shows that changing hydrological conditions in its key market in San Jose has the potential to decrease SJW's growth rate in the future.

Next, it's worth mentioning that mergers, while potentially serving as meaningful growth drivers, can be hard to pull off well. SJW used its richly priced shares to buy Connecticut Water at an 18% premium, creating risk that is overpaid for the business And much of the EPS accretion the company expects is based on cost savings that are far from guaranteed to materialize in the coming years.

A final risk to consider is that water utilities have bucked the trend of regulated utilities and seen very strong outperformance in the past year. For example, SJW is up nearly 30% in the past year compared to about a 15% return for the S&P 500. As a result, its shares are likely overvalued and its 1.7% dividend yield indicates that it doesn't make a good choice for those needing immediate high income.

While SJWs status as a dividend king is certainly attractive to income growth investors, keep in mind that even the faster-growing SJW is likely to only see its dividend grow at 4% to 6% per year over the long term. As a result, it might not make a great choice for dividend growth investors who normally accept lower yields like this in exchange for double-digit dividend growth.

Closing Thoughts on SJW Group

Water utilities are a great source of safe and growing dividends. Their entrenched businesses, characterized by a captive customer base and guaranteed returns on capital, make for very stable and recession-resistant cash flow that supports dividend growth streaks that can span 50 years or more.

Once it merges with Connecticut Water Systems by the end of 2018, SJW will become the third-largest publicly traded water utility in America. The utility will achieve far larger economies of scale, greater geographic diversification, improved access to low-cost capital, and increased profitability. Combined with constructive regulatory environments and a large backlog of approved growth projects, SJW is likely to continue its impressive dividend growth streak for years to come.

However, as with virtually all utilities, paying a fair price is especially important given the sector's slower growth rate compared to other areas of the market. Given the strong performance of water utilities, investors considering the stock should remain patient for a reasonable valuation.