Founded in 1899, General Dynamics (GD) grew largely through acquisitions of military-related companies until the 1990's when it decided to sell off nearly all of its divisions. The company then started expanding again by acquiring combat vehicle businesses, information technology (IT) companies, shipyards, and Gulfstream Aerospace Corporation.

Today, General Dynamics is one of the world’s leading global aerospace and defense companies that sells everything from business jets and submarines to combat vehicles and IT communications systems.

The company’s 100,000 employees are located across more than 40 countries and operate four business segments:

Aerospace (24% of revenue, 35% of operating profit): designs, develops, manufactures, and outfits business-jet aircraft (Gulfstream, which commands 30% global market share), as well as provides aircraft services, such as maintenance, repair, aircraft management, charter, fixed-base operational, and staffing services. It also performs aircraft completion services for other original equipment manufacturers. This segment's operating history dates back more than 50 years.

Combat Systems (19% of revenue, 22% of operating profit): designs, develops, produces, and modernizes, combat vehicles, weapons systems, and munitions. This group offers wheeled combat and tactical vehicles including main battle tanks and tracked combat vehicles, as well as providing armaments and maintenance and logistics support and sustainment services.

Information Systems and Technology (30% of revenue, 25% of operating profit): provides technologies, products, and services that support a range of military, federal/civilian, state, local, and commercial customers. This group offers IT solutions and mission support services; communication, command-and-control, and computer mission systems including imagery, signals, and multi-intelligence systems for customers in the defense sector, intelligence and homeland security communities, as well as foreign governments allied with the U.S.

Marine Systems (27% of revenue, 18% of operating profit): designs, constructs, and repairs surface ships and submarines for the United States Navy and Jones Act ships for commercial customers. This group offers nuclear-powered surface combatants, auxiliary and combat-logistics ships, and commercial product carriers and containerships. It provides design and engineering support services, as well as maintenance, modernization, and lifecycle support services.

Most of General Dynamics’ revenue is from the U.S. Government (61%) with the remainder from U.S. commercial customers (15%) and international commercial and military customers (24%).

Business Analysis

Defense contractors such as General Dynamics typically experience cyclical sales and earnings over time due to changes to government defense spending. In fact, a wave of bankruptcies washed over the defense industry in the 1960's and early 1980's.

And after the end of the Cold War, a large decrease in defense spending caused large-scale industry consolidation. The end result was just five major defense contractors gaining a commanding market share lead (with the blessing of the Pentagon): General Dynamics, Northrop Grumman (NOC), Lockheed Martin (LMT), Raytheon (RTN), and Boeing (BA).

Besides benefiting from operating in a consolidated industry, General Dynamics possesses several competitive advantages that have helped the firm increase its dividend for over 20 consecutive years.

First, defense contractors make mission-critical components on which the lives of soldiers and military mission success depend. Weapons and defense systems are incredibly complex. They often take decades to develop and have to be seamlessly integrated to work with the many systems of a companies' other products.

Given these complexities and the sensitive nature of these products, the procurement process for defense contracts is incredibly complex, involving approval from number of regulators including:

The Federal Acquisition Regulation (FAR)

The DoD's Defense Federal Acquisition Regulation Supplement (DFARS)

The U.S. Defense Security Cooperation Agency (DSCA), a Pentagon-run agency that is responsible for foreign military defense system sales to US allies

Thanks to how long and costly it is to obtain contracts, the defense industry is generally broken up into a series of duopolies for various weapons components. For example, space-based systems are dominated by Boeing and Lockheed, missile systems sales mostly go Raytheon and Lockheed, and Navy shipbuilding contracts are usually awarded to General Dynamics and Huntington Ingalls Industries (HII). In fact, Huntington and General Dynamics control the only five shipyards that build navy ships in the U.S.

In other words, General Dynamics is one of the only two American companies with the technological expertise to construct key Naval systems, including nuclear attack subs and ballistic missile submarines. The firm's moat in this area was enshrined in 2002 and reaffirmed in 2009 when the U.S. Navy agreed to an agreement for Huntington and General Dynamics to share the workload of constructing U.S. Naval vessels.

Since today's naval vessels come with advanced technology, such as all-electric propulsion and laser missile defense systems, it's all the more unlikely that major new competitors will enter this niche but lucrative field.

In addition, the very nature of defense contracts forms a moat for General Dynamics. That's because in 2007 Congress passed a law mandating that fixed-price contracts become the default option on product procurement. In other words, the burden for any delays or cost overruns is born by the contractor, which means that smaller, not well capitalized firms have a much tougher time competing for contracts, especially given the government's need for reliability.

There are only so many government contracts to win each year, too. Fortunately, many of the company’s defense businesses have been around for a very long time. Some of them even have roots dating back to the 19th century.

With so much operating history, General Dynamics has built up very strong relationships with government officials and established a reputation of quality and reliability. New entrants would have a hard time breaking through the strong customer bonds enjoyed by incumbents, especially given the limited number of contracts up for grabs each year.

The high barriers to entry created by regulations, the mission-critical nature of defense systems, and the expertise required to build such systems are why in the first quarter of 2018 alone General Dynamics won contract awards for:

$445 million to produce Piranha 5 wheeled armored vehicle for Romanian military ($1 billion potential contract)

$215 million for NASA contract to upgrade the ground infrastructure for its satellite network

$695 million for the procurement of parts for the construction of four Virginia class nuclear attack subs

And keep in mind that those were just three of 21 contracts the company obtained in the first three months of the year. All told, the company's backlog of contracts stands at $62 billion, and management believes it can potentially achieve a total of $87.6 billion in sales due to later stage contract wins.

To put that in perspective, the current awarded and potential backlogs represent about two and three years of company sales, respectively. Even better, in 2017 General Dynamics reported its fourth consecutive year with a book-to-bill ratio (new orders/revenue) of 1.0 or greater. This means that General Dynamics' backlog is growing over time even as it grows its deliveries and sales.

And on the commercial jet side of the business (which accounts for about 35% of operating earnings), General Dynamics' Gulfstream dominates its niche thanks to decades of experience designing and building safe and reliable aircraft. Building business jets is a capital intensive and complex endeavor, in which few companies dare to tread.

In addition, because of the life and death nature of aircraft, businesses prefer manufacturers with long track records for safety, as well as those large enough to provide ongoing maintenance and upgrades over the course of a jet’s useful life.

With customers paying north of $65 million for its top of the line Gulfstream 650 jets, maximizing safety and minimizing maintenance headaches by outsourcing to the company's service centers helps create a wide moat for General Dynamics.

Not surprisingly, Gulfstream benefits from strong brand recognition and its dominant support network. In fact, this business boasts the largest service network in the business aviation industry with service centers located on four continents, including the largest aircraft maintenance facility in the world. Gulfstream was also the first manufacturer to open a service facility on mainland China.

Business customers fly their jets around the world and need a vendor that can quickly repair and service their jets if any issues arise. The resulting switching costs have helped Gulfstream maintain a strong market share and generate meaningful aftermarket business.

High switching costs and a limited number of rivals grant General Dynamics very large economies of scale, which keep its costs very competitive for price-sensitive government work and results in high margins on the commercial side. And thanks to tax reform, General Dynamics plans to invest $3 billion between 2018 and 2021 into productivity and capacity boosting investments.

Just as importantly, General Dynamics maintains one of the strongest balance sheets in the industry. In fact, the company maintains an A+ credit rating from S&P that allows it to borrow at very low interest rates. As a result, General Dynamics has financial flexibility to invest in R&D, expand and improve its manufacturing capacity, and pay its fast-growing dividend without hampering its long-term growth efforts.

Going forward, analysts believe that higher defense spending, growing demand for commercial aircraft, General Dynamics' productivity initiatives, lower taxes, and ongoing share repurchases will drive low double-digit growth in earnings per share. Assuming those optimistic projections bear out, the company should have no trouble continuing to reward shareholders with double-digit dividend growth.

Overall, General Dynamics has strong staying power. The company's core defense and aerospace businesses benefit from a lack of competition, complex manufacturing processes, regulatory barriers, and massive backlogs. Combined with the company's substantial scale and large installed base, which generates high-margin aftermarket revenue, General Dynamics enjoys excellent profitability and cash flow that should enable it to pay growing dividends for many years to come.

That being said, General Dynamics faces its fair share of major risks that could cause its sales, cash flow, and dividend growth to fall short of expectations.

Key Risks

Many of the factors that form General Dynamics' competitive advantages can also serve as a double-edged sword by creating variability in the firm's financial results. Most notably, defense spending accounts for about 50% of the company's revenue but can be very volatile. For instance, the wind down of the wars in Iraq and Afghanistan caused U.S. defense spending to drop 25% from 2008 to 2015.

That drop in defense spending was also driven by the decision by Congress to enact the Budget Control Act of 2011 (BCA), which established specific limits on annual appropriations for fiscal years 2012–2021. Due to the gridlock in today's highly polarized Congress, the BCA has been amended numerous times resulting in a large fluctuation in DoD spending, including a 7% decline in spending in 2013 followed by flat DoD budgets in 2014 and 2015.

The good news for General Dynamics is that in 2016, 2017, 2018, and 2019, the Pentagon's budget increased 5%, 3%, 15%, and 2%, respectively. At least for the last few years and the next two, almost all U.S. defense contractors should have the growth winds at their backs.

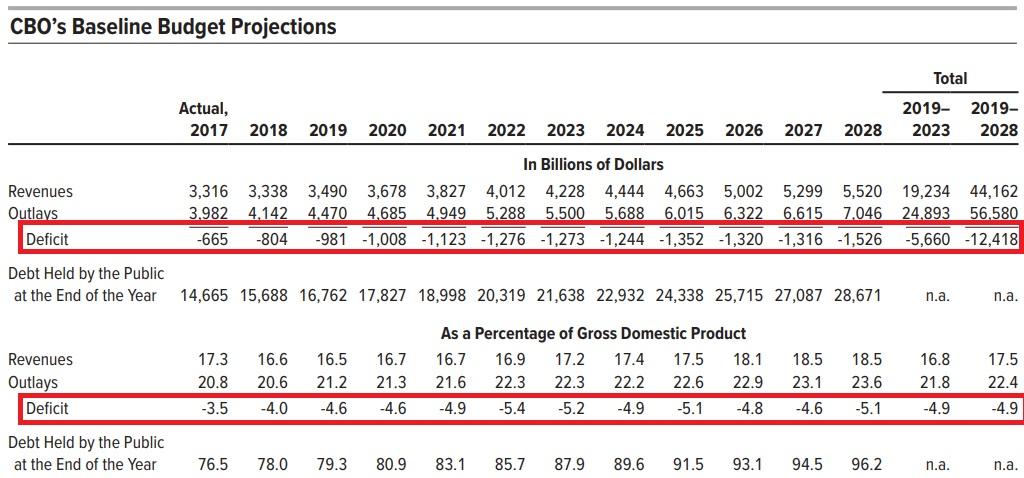

However, General Dynamics' dependence on the U.S. government for 61% of its 2017 revenue means that the firm will remain sensitive to ongoing concerns over rising U.S. deficits. As seen below, the Congressional Budget Office (CBO) expects the deficit to rise by about 150% to $1.5 trillion per year within a decade. As a result, future defense spending cuts might be more severe then in the past and make it much harder for the company to grow its top and bottom lines.

Source: Congressional Budget Office

Next, investors must consider the nature of General Dynamics' government contracts. Over 50% of the firm's contracts are fixed-priced, with 42% being reimbursable cost-plus contracts (mostly R&D related). Fixed-price contracts mean that General Dynamics is at risk from delays and overruns in delivering on its defense systems. That risk is elevated if one of its many subcontractors fails to meet its development or production targets.

Fortunately, General Dynamics is not overly dependent on any single defense system project. The company's diversification (including its commercial jet business) should insulate it somewhat from any cost overrun, and General Dynamics' long-term earnings power is unlikely to be impacted.

Finally, investors should be aware that due to the relatively slow growing nature of the defense industry, acquisitions are a frequent occurrence and bring their own challenges and risks. In early 2018, General Dynamics announced it was buying CSRA, a government IT services contractor, in a $9.6 billion deal.

The deal is expected to diversify the company away from its large dependence on the Pentagon. General Dynamics' government IT business is now doubling in size and will become the second largest government IT contractor by market share, positioning it to benefit from the government's ongoing refresh of dated IT systems and desire to award fewer, larger contracts.

The acquisition is expected to become accretive to earnings per share and free cash flow by 2019. However, that depends on whether or not management can achieve their target of annual cost savings of 2% of the combined company's revenue by 2020.

While CSRA carries high margins for its industry, General Dynamics' IT segment is still a relatively slower growing and lower margin business, with 11.4% operating margins in 2017 compared to 14.9% for combat systems and 17.2% for aerospace. This implies that future efforts at diversification might mean more stable revenue but lower overall profitability.

Investors also need to keep in mind that every major acquisition comes with the risk of overpaying for a company, as well as successfully integrating its corporate culture and achieving cost saving targets. The same is true for General Dynamics' recently announced acquisition of Hawker Pacific for $250 million. This Australian-based provider of jet and helicopter management services is going to be tucked into General Dynamic's Jet Aviation subsidiary.

The deal adds new service centers in seven Asian countries and is designed to bolster the company's aerospace division which has struggled to fully recover from the financial crisis and global great recession.

Unlike commercial aircraft, whose orders and deliveries have soared to all-time highs, global business jet deliveries remain well below their 2008 peak. As the industry leader, Gulfstream has held up better than most but still sold just 120 jets in 2017 compared to 156 jets in 2008.

The good news is that business jet sales tend to track corporate earnings over time, so Gulfstream deliveries should hopefully continue to climb unless another global recession saps the purchasing power of its customer base.

Despite their strong competitive positions, General Dynamics' defense systems and business jets are largely at the mercy of government budgets and the health of the overall global economy over the short term.

Closing Thoughts on General Dynamics

General Dynamics is one of the best defense contractors in America. Thanks to the complex nature of its industry, the company enjoys several advantages that have allowed it to reward investors with more than a quarter century of fast and consistent dividend growth.

And despite the numerous risks inherent to the defense and aerospace industries, General Dynamics' conservative management and fairly diversified sources of cash flow seem likely to make it a dependable dividend growth stock over the long term.