Cracker Barrel: A Quality Dividend Payer in a Tough Market

Cracker Barrel Old Country Store (CBRL) has been in business since 1969 and operates a chain of more than 650 company-owned restaurants located throughout the U.S. Cracker Barrel's country-themed, full-service restaurants offer diners a variety of breakfast (24% of sales), lunch (39%), and dinner (37%) foods with meals costing about $10 on average.

Each restaurant location also has a large gift shop, which offers decorative and functional items, such as apparel and accessories, packaged foods, decor, toys , and bed and bath goods.

In 2018, about 80% of Cracker Barrel's revenue was generated from restaurants, with the remaining 20% from its gift shops.

Cracker Barrel has paid dividends for more than 30 years, raising its payout each year since 2011. The company has also paid a special dividend each year since 2015.

Business Analysis

The restaurant industry is extremely challenging thanks to brutal competition, (there are over 1 million restaurants in the U.S.), a business model that's sensitive to the economy, high labor turnover rates, and fluctuating input costs that can result in swings in profitability.

In fact, about 60% of restaurants fail or change ownership within their first three years, according to a 2005 study conducted by Cornell University.

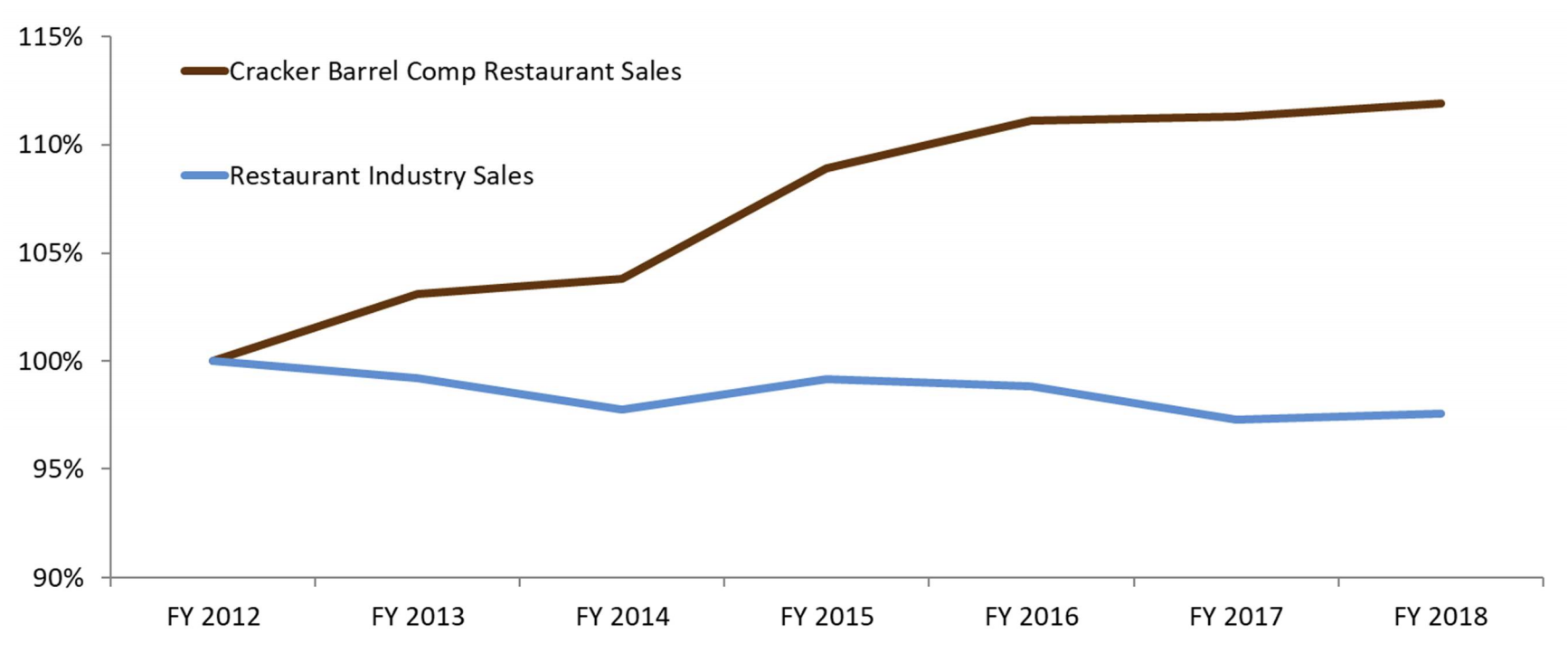

However, Cracker Barrel has done better than most of its peers at managing to maintain both top and bottom line growth. As you can see below, the company's same-store restaurant sales, which measures sales growth from locations open at least a year, have outpaced the restaurant industry's sales in recent years.

Source: Cracker Barrel Investor Presentation

Strong brand recognition and mastering the Southern casual dining experience have driven Cracker Barrel's long-term success.

In business for 50 years, Cracker Barrel has built a brand focused on serving travelers who desire affordable comfort food. Approximately 83% of the firm's restaurants are located along interstate highways, with many others located near tourist destinations.

This positioning helped the company grow a loyal base of diners well before the digital age arrived. Outdoor advertising such as billboards has long been the largest advertising vehicle used by Cracker Barrel to build awareness with travelers. With decades of marketing spending behind the company, this approach has been a success.

However, the restaurant world is changing. Consumers desire healthier foods, faster service (e.g. the continued rise of fast casual restaurants), and greater convenience (online ordering, to-go offerings, delivery, etc.). Technology has also reduced the search cost travelers face to find quality dining options.

To maintain its relevancy going forward, Cracker Barrel is implementing several long-term strategies. First, the company wants to enhance its core brand with new menu items to continue meeting consumers' tastes. In its 2018 annual report, for example, CEO Sandy Cochran discussed the firm's specialty beverage initiative which intends to take advantage of consumers' desires for coffee and more upscale drinks.

Cracker Barrel also desires to make its offerings more accessible to consumers who like the restaurant's food but do not want the sit-down restaurant experience. The company is adding the convenience of online ordering and mobile payments, expanding its catering and to-go offerings, and increasing its delivery coverage.

Off-premise sales accounted for 7% of Cracker Barrel's fiscal 2017 sales, and thanks to these efforts management believes this part of the business will eventually reach at least 10% of total revenue.

Besides improving its existing operations, management hopes to expand Cracker Barrel's store count. In October 2017 Cracker Barrel said it believed its ultimate buildout is 750 to 800 units, compared to about 650 today. If successful, new store openings could add around 1 percent point to Cracker Barrel's top-line growth.

Overall, Cracker Barrel has historically done a nice job differentiating itself in a crowded and competitive marketplace. The company's unique Southern brand, economies of scale, relatively low-cost locations off highways, conservative balance sheet, and blend of restaurant and gift shop revenue have helped it create meaningful value for dividend growth investors over the years.

However, the business faces several risks that could challenge its long-term outlook for profitable growth.

Key Risks

In the short term, Cracker Barrel's business can be impacted by a number of factors: restaurant discounting, consumer spending trends, commodity price inflation, labor market shortages, and more (food costs and labor account for about 65% of the company's revenue).

While none of these issues seem likely to affect the firm's long-term outlook, there are several risks that could weigh on Cracker Barrel's long-term earning power.

First, brick-and-mortar retail is under increased pressure from the rise of e-commerce. Gift shops account for 20% of company-wide revenue, and Cracker Barrel's same-store retail sales have declined at a low-single digit pace each year since fiscal 2017.

Part of the problem is likely that the value proposition of Cracker Barrel's gift store isn't nearly as strong as its food menu. Cracker Barrel's retail store earns a gross margin near 50% (sales less cost of merchandise). For perspective, Target and Walmart have gross margins around 25% to 30%, and packaged food maker General Mills earns a gross margin near 35%.

In other words, Cracker Barrel's merchandise assortment (apparel, accessories, packaged food, toys, decor, etc.) isn't very price competitive. Online shopping continues making it easier for consumers to find the best deals, and Cracker Barrel's retail concept could be losing some of its relevancy, weighing on the firm's overall growth rate.

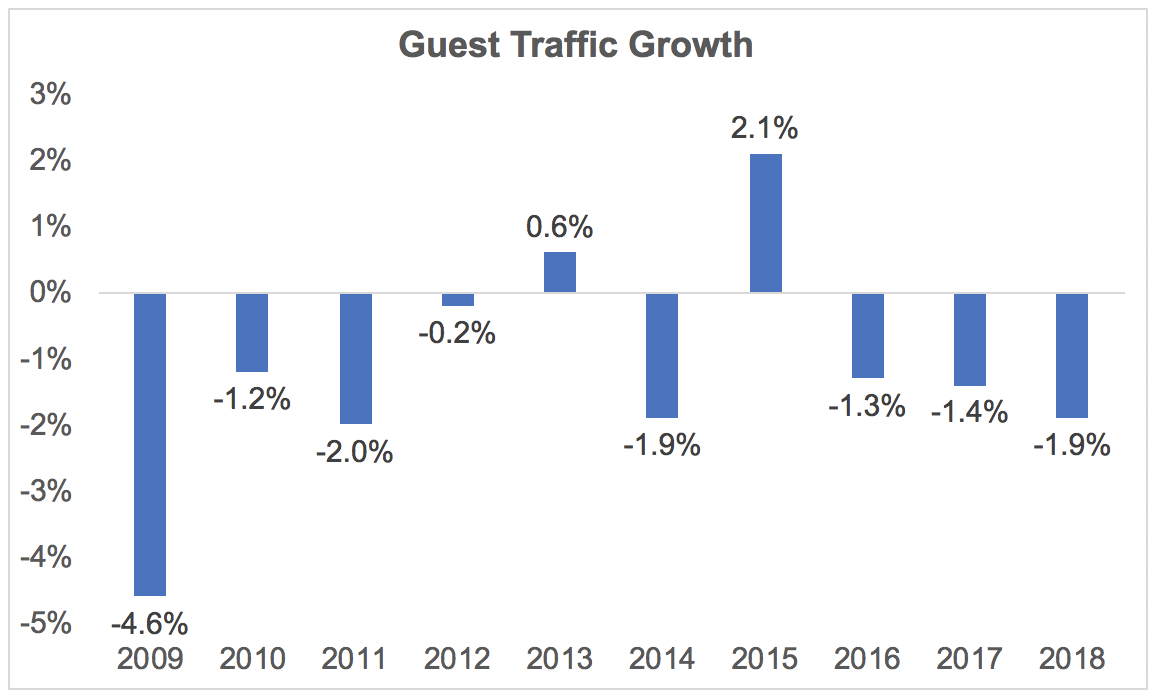

The company continues generating same-store growth on the restaurant side of the business, but these gains have come solely from price increases in recent years. In fact, Cracker Barrel's guest traffic has declined in eight of the last 10 years, including 1% to 2% declines each year since fiscal 2016.

Source: Cracker Barrel, Simply Safe Dividends

Fewer customers visiting the company's existing restaurant locations suggests the Cracker Barrel concept is losing some of its luster. It also doesn't bode well for a turnaround in the firm's high-margin retail sales.

Poor traffic trends could also mean that management's goal of reaching upwards of 800 store locations will be out of reach. As a casual sit-down restaurant, and one with a very specific regional theme, the total addressable market may not be much larger than the company's store count currently serves.

With that said, cost savings initiatives, price increases, operational improvements, and new store openings have helped Cracker Barrel continue growing its earnings and generating significant free cash flow. The company's balance sheet also remains in good shape, reducing Cracker Barrel's risk profile.

However, while Cracker Barrel seems likely to remain a cash cow, investors should not expect much growth going forward. Low- to mid-single digit dividend increases that track underlying earnings growth seem most likely.

Closing Thoughts on Cracker Barrel Old Country Store

The restaurant business is very competitive, cyclical, and not where one usually looks for steadily growing dividends. Cracker Barrel has managed to handle the industry's challenges well, recording decent same-store restaurant sales, solid earnings growth, and generous dividend increases over the last five years.

However, given the cyclical nature of the industry and the maturity of Cracker Barrel's core concept, the company is likely to grow its top and bottom line much slower going forward. When combined with the struggles the firm is having with its retail business in an ever-more digital world, Cracker Barrel's best dividend growth days could be behind it.

The company's dividend certainly appears to remain on solid ground, but income investors looking at Cracker Barrel may be able to find a better combination of income and growth elsewhere, especially in other industries that are less ruthless than the restaurant business.