Simon Property Group: A High-Yield REIT Adapting to the Times

Simon Property Group (SPG) is America’s largest mall owner, with full or partial ownership interest in over 230 properties across North America, Europe, and Asia. In 2018 Simon's U.S. mall tenants generated over $60 billion in retail sales.

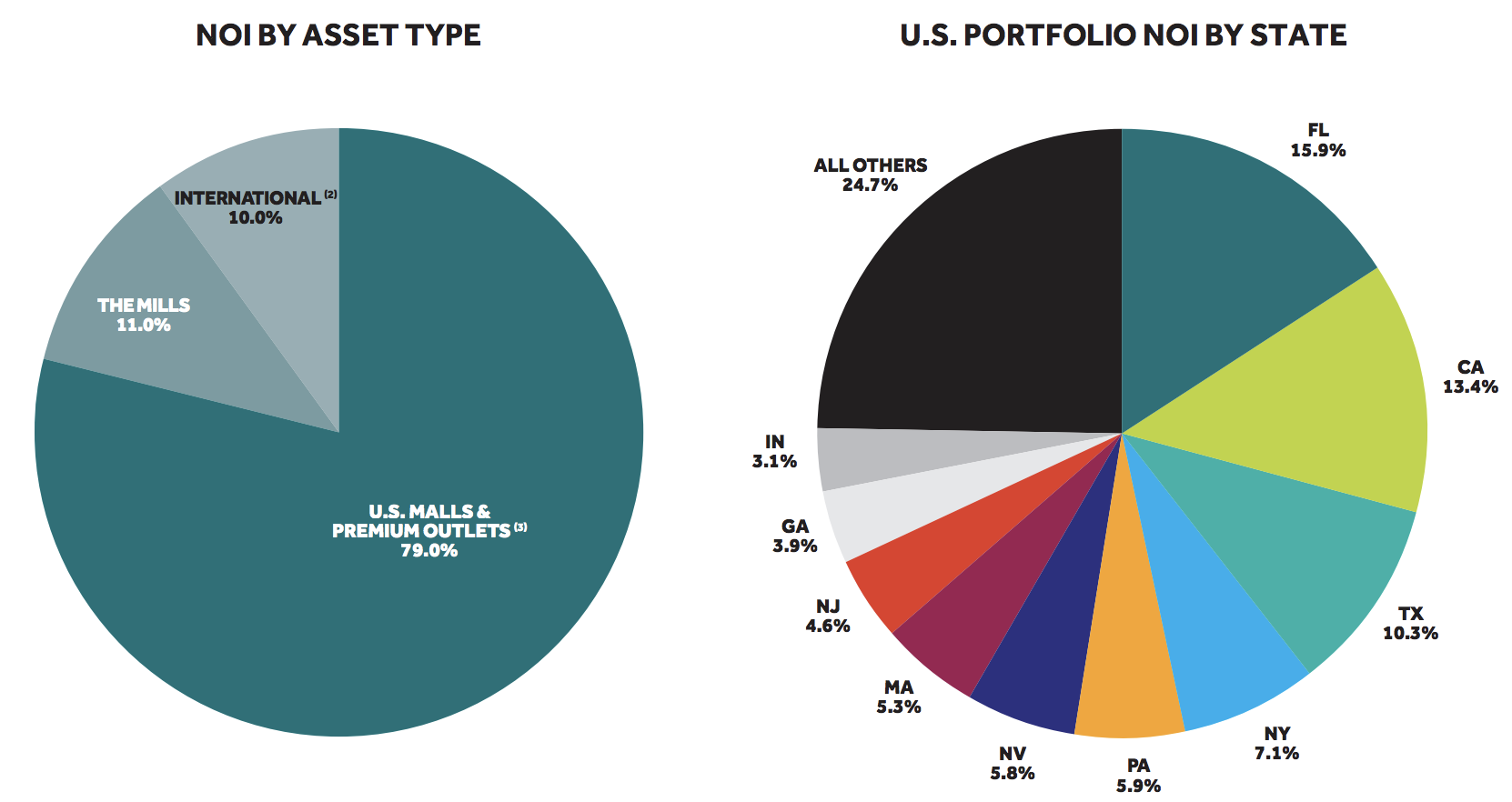

Most of Simon's locations are anchored by department stores, and the vast majority of net operating income, or NOI, is derived from the company's U.S. malls (48% of NOI) and premium outlet centers (42%), which are essentially groups of discounted luxury stores. Simon's U.S. malls and outlets, which accounted for 79% of NOI in 2018, are concentrated in large and relatively fast-growing states, including Florida (16% of NOI), California (13%), Texas (10%), and New York (7%). The company's premium super regional mall properties ("The Mills" - 11%) and International properties (10%) account for the remainder of its income.

Source: Simon Investor Presentation

In 2014 Simon refocused its portfolio on its top regional malls. The company spun off its weaker strip centers and smaller enclosed malls, which consisted of about a third of its properties but generated only 10% of its cash flow. The new spin-off REIT was named Washington Prime Group (WPG), and today Simon derives the vast majority of its profits from higher quality malls.

The REIT’s historical success has been due to management’s disciplined approach to slow but steady growth. Specifically, Simon Property Group focuses exclusively on high-end and ultra-premium luxury properties (such as its “Mills properties”), with good diversification across the U.S. as well as with tenants.

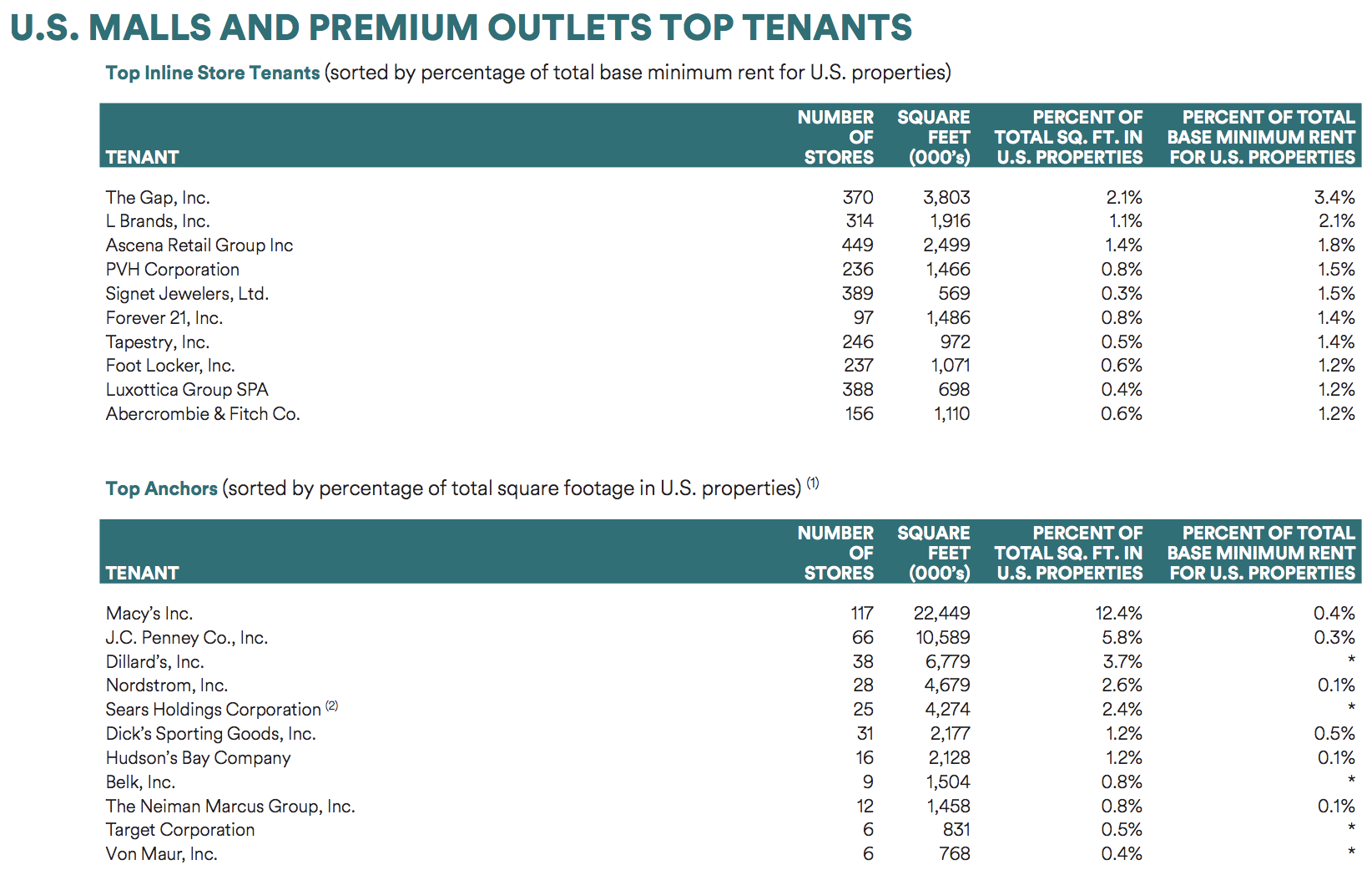

Simon Property Group’s largest tenant (The Gap) accounts for just 3.4% of its total rent for U.S. properties, for example. The malls the company owns are also reasonably diversified by anchor tenants with Macy’s representing the biggest share of square footage (12.5% of the total).

Source: Simon Property Group Earnings Presentation

This helps protect Simon Property Group from being overly exposed to the fate of any single retailer, which is important because brick-and-mortar retail is a notoriously tough business with a low survival rate for many companies (consumers are fickle).

Simon has grown its dividend every year since 2010. While the firm did cut its dividend during the Financial Crisis, that was due to an overly leveraged balance sheet. Over the past decade, Simon has strengthened its balance sheet and is now one of the few A-rated REITs by credit rating agencies.

Business Analysis

While lower quality retailers and malls have suffered in recent years, Simon Property Group’s focus on the high end of the market has helped it continue growing despite the rise of e-commerce giants such as Amazon (AMZN).

While rivals such as CBL & Associates (CBL), Tanger Factory Outlet Centers (SKT), and Simon's spin-off Washing Prime Group are experiencing low- to mid-single digit same-store net operating (NOI) declines, Simon expects to continue generating low single-digit growth through at least 2019. That has helped the firm maintain industry-leading occupancy rates and lease spreads.

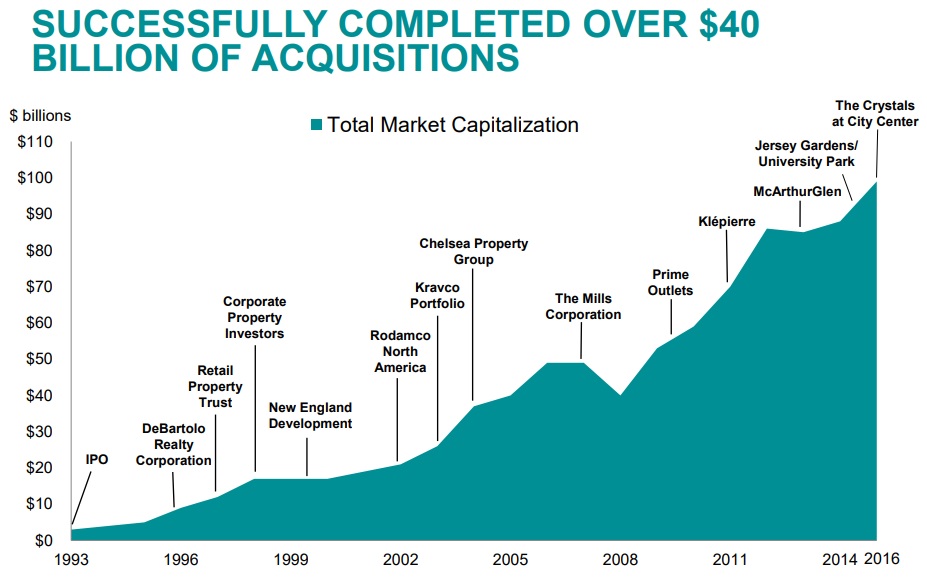

Simon's success is due to several competitive advantages, starting with its management team. The company is led by CEO David Simon, who has held the top job since 1995. Mr. Simon has delivered an impressive track record of wise capital allocation decisions to drive profitable growth, especially with acquisitions (over $40 billion in total since going public) and foreign joint ventures.

Source: Simon Property Group Investor Presentation

For example, in 2007 Simon partnered with private equity firm Farallon Capital Management to acquire the REIT "The Mills" for $7.9 billion. This business specializes in super regional malls (mega malls of 800,000+ square feet of leasable space). In 2012 Simon bought out Farallon and now owns all of The Mills' 14 locations outright.

In 2012 Simon paid $2 billion to purchase a 28.7% stake in Klépierre, the highly successful European mall REIT with properties in 16 EU countries. Compared to the U.S., European regions tend to have less mature and more fragmented shopping centers, potentially making them more appealing for long-term growth.

Over the years Simon has further expanded its overseas holdings, and today The Mills and its International portfolio enjoys some of the highest occupancy (nearly 100%) and highest leasing spreads (almost 35% in 2018) of any mall REIT in the world.

Leasing spreads measures how much a mall REIT increases its rent on expiring leases. In other words, it represents the pricing power a mall owner has. A consistently strong and positive lease spread (10+%) is often a sign of a vibrant mall, one with good traffic, high sales per square foot, and thriving tenants.

Even in its U.S. malls, which are arguably under the most potential pressure as consumer shopping habits change, Simon has continued enjoying strong occupancy of over 95%, low double-digit lease spreads (over 10% since 2010 and 14.3% in 2018), and consistent gains in sales and rent per square foot.

The firm's steady fundamentals are attributable not only to its ability to maintain some of the most premium luxury malls in the country, but also Simon's investments in non-retail assets. Specifically, the REIT is incorporating more office space, apartments, and hotels into its existing properties, thus making its malls more valuable "experiential" locations.

Simon's tenant base is also highly diversified (top 5 = 10.3% of U.S. rent) with little exposure to deeply distressed department store chains such as Sears (2.4% of total square feet, less than 0.1% of rent), and J.C. Penney (5.8% of total square feet, 0.3% of rent).

Thanks to its diversification and focus on more differentiated mall properties, Simon's cash flows have remained stable, which allows for a more reliable dividend.

In 2018 Simon managed to generate solid results across all of its most important fundamental metrics, even despite the cautionary headlines about the state of the mall industry:

Occupancy: 95.9% (+0.3%)

Sales per square foot: $661 (+5.3%)

Same-Store NOI: +2.3%

Total NOI: +3.7%

U.S. Mall Lease Spread: +14.3%

FFO per Share Growth: +8.2%

Going forward, the vast majority of Simon's investments are expected to be focused on improving its existing locations rather than expanding its number of properties. Low- to mid-single digit cash flow and dividend growth seems like a reasonable expectation for income investors, though Simon's risk profile looks more attractive than most of its mall peers.

Since REITs must legally payout 90% of taxable income as dividends, most REITs retain very little cash flow for reinvesting in future growth (usually 10% to 20%). This is why the industry offers high yields but is also marked by large debt levels and frequent equity issuances (selling new shares).

However, Simon is one of the few REITs with a self-funding business model. That means it's able to fund all its growth with reasonable amounts of low-cost debt and retained cash flow. In other words, Simon's growth potential does not hinge on a fickle equity market, and the firm is also one of the few REITs to have a buyback program.

Simon's board first authorized share repurchases in 2015. If the REIT's share price gets too low, Simon can buy back some of its stock and thus further boost its cash flow per share growth. In early 2019 management authorized a new $2 billion share repurchase program (about 4% of SPG's market value), indicating that the firm likely plans to continue self-funding for the foreseeable future.

Simon's ability to self-fund its growth is supported by its conservative balance sheet. The firm's leverage ratio is the lowest in the industry, helping it achieve an "A" credit rating from Standard & Poor's. Management appears to have learned from its mistake of running the business with too much leverage during the financial crisis, reducing the risk of another dividend cut whenever the next recession happens.

Overall, Simon Property Group appears to be the undisputed leader in its industry and enjoys competitive advantages in terms of management quality, cost of capital and profitability, and a decent runway of projects that it can finance with zero dependence on fickle equity markets. In other words, Simon is one of the few REITs whose growth potential is fully within its own control.

But while Simon Property appears to represent one of the highest quality mall REITs, there are still risks to keep in mind.

Key Risks

Simon has done an admirable job of adapting to fast-changing industry conditions over the decades. However, there are still risks that could still challenge the REIT and result in slower than expected future growth.

For one thing, Simon does have exposure to some struggling retailers, including top tenants The Gap, Abercrombie & Fitch, Ascena Retail, and L Brands. Together these represent 5% of rent. If they end up closing stores, then Simon's occupancy rate could temporarily decline as it has to find replacement tenants.

While Simon's premium-focused properties have strong enough sales and traffic to eventually allow management to replace weaker tenants with thriving ones, there is a transition period that can result in slower cash flow growth in any given year.

For example, due to having to replace many struggling tenants in 2019, management is guiding for just 2.9% cash flow per share growth this year, or less than half of 2018's impressive rate. Fortunately, management expects growth to accelerate in 2020 and 2021 and be among the highest in the industry.

However, a potentially larger risk is that malls and tenants will continue to emphasize omnichannel shopping (mixing retail and online sales), which could result in physical store locations becoming less important in the future.

Specifically, the concern is that if retailers focused more on online sales, with physical stores serving merely as pick up and return points, then many of Simon's tenants might not be willing to pay the higher rents that the company has been so good at extracting. Omnichannel typically requires less retail space as well, so Simon could face a tougher time profitably replacing old tenants than it has in the past.

While Simon's occupancy remains strong near 95%, many of its rivals have found that in order to maintain occupancy they've had to offer more concessions on rent, resulting in declining lease spreads. Only time will tell if the REIT can continue delivering growth across its key metrics.

Building new malls is incredibly expensive and time consuming as well, and in the U.S. the market is already oversaturated. In fact, Morningstar observes that the U.S. has 24 square feet of retail space per capita, two to 10 times that of other developed countries.

In 2017, Credit Suisse estimated that by 2022 about 20% to 25% of U.S. malls (representing over 1 billion square feet of leasable space) could close. While few of those are likely the type of high-quality malls that Simon focuses on, the point is there is limited ability for the firm to grow its U.S. mall property base, other than potential acquisitions of major rivals like Taubman (TCO) and Macerich (MAC).

But all large acquisitions come with the risk of overpaying and execution not going as well as planned. Fortunately, on the company's fourth-quarter 2018 earnings call, management made it clear that Simon has no short-term plans for major acquisitions. Instead of buying or building new U.S. malls, Simon is investing in premium outlet centers, and all of its new malls are currently being constructed overseas.

Redevelopment projects are another important focus, though there is also a limit to how long Simon can maintain its growth simply by improving its U.S. properties.

While mixed-use properties add some cash flow diversification, management expects non-retail to mainly serve as a value-adding feature to continue driving foot traffic at its existing malls. In other words, these properties are unlikely to ever make up the majority of the REIT's income.

All of these risks put together mean that Simon is essentially the highest quality operator in an industry that's working through large-scale disruption, and thus the company might end up proving to be "the nicest house in a bad neighborhood."

Investors will want to watch the REIT's core fundamental metrics closely in the coming years, especially sales per square foot, occupancy, and U.S. mall lease spreads.

If lease spreads dip below 10% and remain there for several years, then Simon's ability to deliver similar organic growth rates as it has enjoyed in the past might become permanently impaired, reducing its long-term outlook even though the dividend would likely remain on solid ground.

And while the firm's premium locations and skilled management team seem likely to help Simon outperform most of its mall rivals in the coming years, it's also true that investors can't expect Simon's strong double-digit dividend growth to continue.

The firm's payout ratio has increased from less than 50% in 2013 to around 70% today, so Simon will probably need to grow its dividend in line with cash flow per share growth (likely 3% to 4% annually).

Closing Thoughts on Simon Property Group

Simon Property Group has proven to be a solid long-term dividend growth investment thanks to the company's disciplined and adaptable management team, strongest balance sheet in the sector, and low-cost growth capital.

Simon's future looks the brightest of almost any mall REIT, but investors need to remember that it's quite possible that continued changes in consumer spending habits will make it much harder for the company to recreate its past successes.

So while Simon appears to represent a potentially decent high-yield value investment today, interested investors must understand and be comfortable with the long-term growth risks the company faces as the industry evolves.

When dealing with businesses facing a wider range of potential outcomes, it's especially important for investors to maintain well-diversified portfolios with reasonable position sizes to minimize company-specific risks.