STORE Capital (which stands for Single Tenant Operational Real Estate) is a relatively new triple-net lease REIT, having gone public in 2014. However, the company is led by an experienced management team that previously built three successful triple net lease REITs (FFCA, Spirit Finance, STORE Holding) and has invested over $17 billion in more than 9,600 properties.

STORE owns over 2,200 properties leased under long-term contracts (average remaining lease duration is 14 years) to more than 400 companies operating across roughly 100 industries. The REIT mostly serves middle market businesses, with its median tenant generating just over $50 million in annual revenue.

While smaller businesses can be riskier, STORE's tenants appear to be in good shape, collectively recording 15% revenue growth in 2018 while sporting a median rental coverage ratio (operating cash flow / rent) of 2.1, which is quite safe for this industry. In fact, management believes the REIT's median customer could see a 40% decline in sales before their ability to cover rent would be at risk.

It's also worth nothing that 91% of STORE's leases are "master leases" in which a tenant has to pay STORE for all of its leased properties, even for stores that may be underperforming individually. Master leases further help to insulate the REIT's cash flow.

That strong tenant profile helps explains why STORE's occupancy rate has never fallen below 99% since its IPO. While all of STORE's properties are located in the U.S., the firm's rent is derived from a variety of industries.

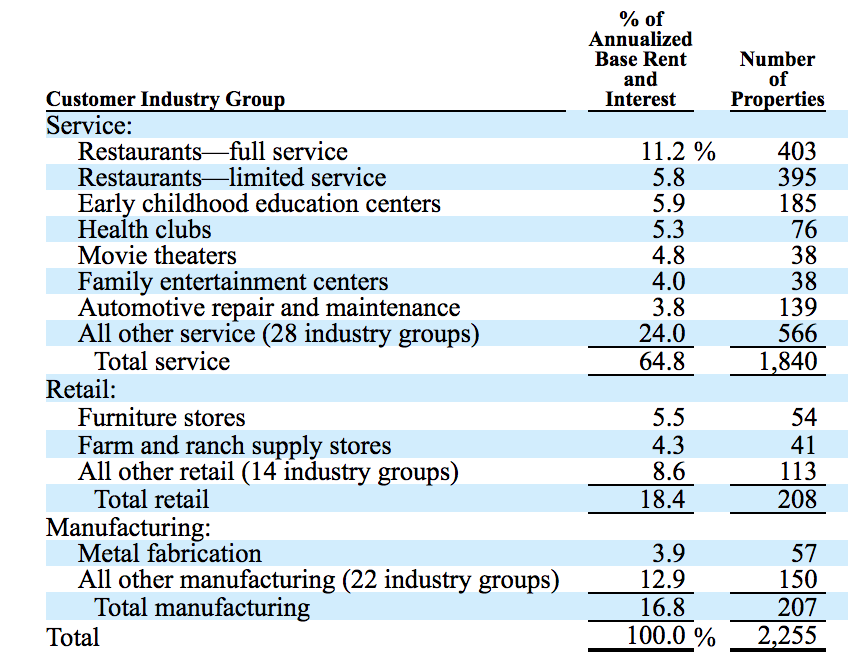

Approximately 65% of STORE's rent comes from service focused industries, with the remainder from retail (18%) and manufacturing (17%) markets. Importantly, its retail exposure appears to be mostly in markets that are internet resistant.

Source: STORE 10-K

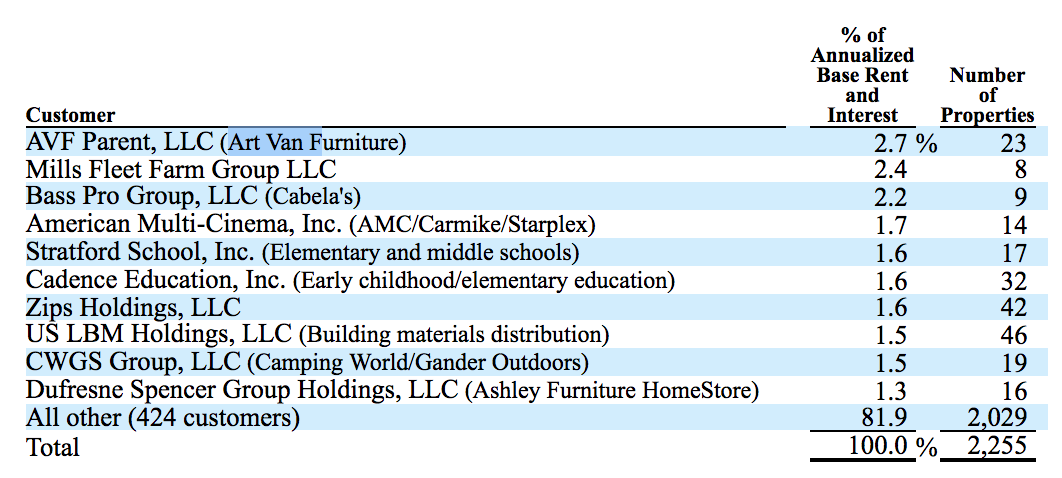

No tenant accounts for more than 3% of rent (Art Van Furniture is the largest at 2.7%), and its top 10 tenants represent less than 20% of rent. With the firm's number of property locations growing around 15% annually in recent years, the REIT's business seems likely to remain well diversified.

Turning to the dividend, STORE's track record is short because it is a relatively new REIT. However, the company has grown its dividend every year since its IPO in 2014 and publicly emphasizes its commitment to a safe and growing payout.

Business Analysis

There are several key attributes that every REIT should ideally possess to be considered a quality high-yield dividend growth stock.

The first is a quality management team, with experience in disciplined capital allocation and good risk management skills. This is because the triple net lease industry is one in which a REIT will buy a store from an existing tenant, and then lease it back under a long-term (10- to 20-year) contract with annual rent price escalators baked in. These escalators are usually tied to inflation and give a REIT some cash flow protection should inflation accelerate in the future.

Of course, if a tenant's business falls on hard times, then the cash flow-to-rent ratio might also decline to potentially dangerous levels. In such a scenario a tenant may default on its rent, or even go out of business entirely. That would leave the REIT on the hook for maintaining the property, including paying property taxes and insurance costs (negative cash flow properties).

Fortunately, STORE's management team appears to be very good at managing risk. For example, the average tenant's cash flow-to-rent ratio has remained above 2.0 and stable over time. This indicates that the company's tenants are generally performing well and are more likely able to afford the low single-digit rent escalators built into STORE's leases.

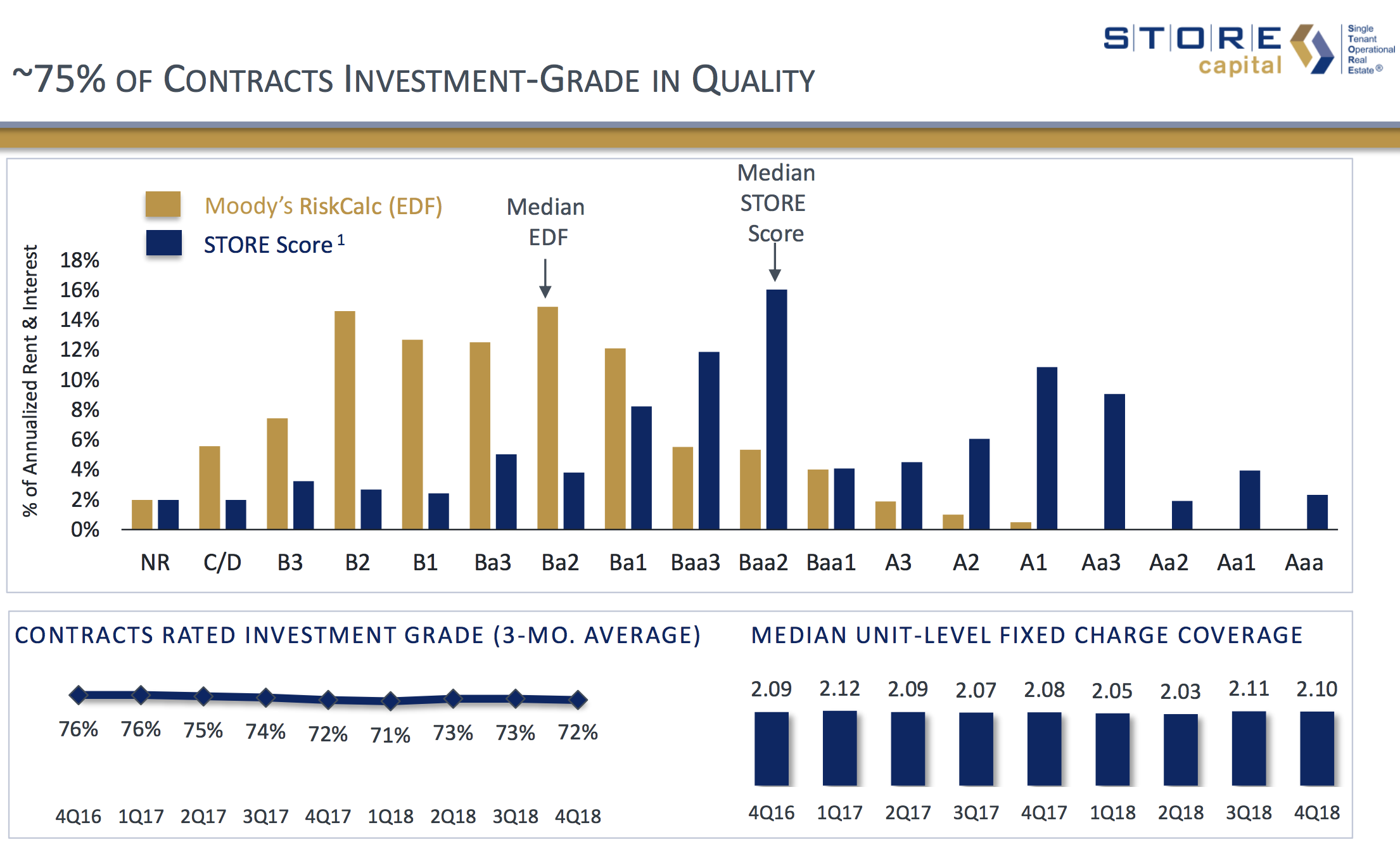

Importantly, STORE estimates that approximately 75% of the lease contracts it holds are of investment-grade quality, though that's based on management's assessment and not official credit rating agency scoring.

Source: STORE Investor Presentation

Moody's quantitative risk assessment calculator rates STORE's tenants slightly lower but still relatively high grade given the generous cash yields the REIT is obtaining on new properties. And the median rental coverage ratio on its tenants have been stable at 2.1 over the last two years, indicating STORE's rent is coming from customers who are doing well in today's economy.

When combined with STORE's conservative payout ratio (more on that later), this focus on contract quality should help protect the dividend over time.

Quality REITs also possess business models that generate recurring and predictable cash flow each year, supporting their ability to pay generous dividends. Once again, STORE's operations are impressive.

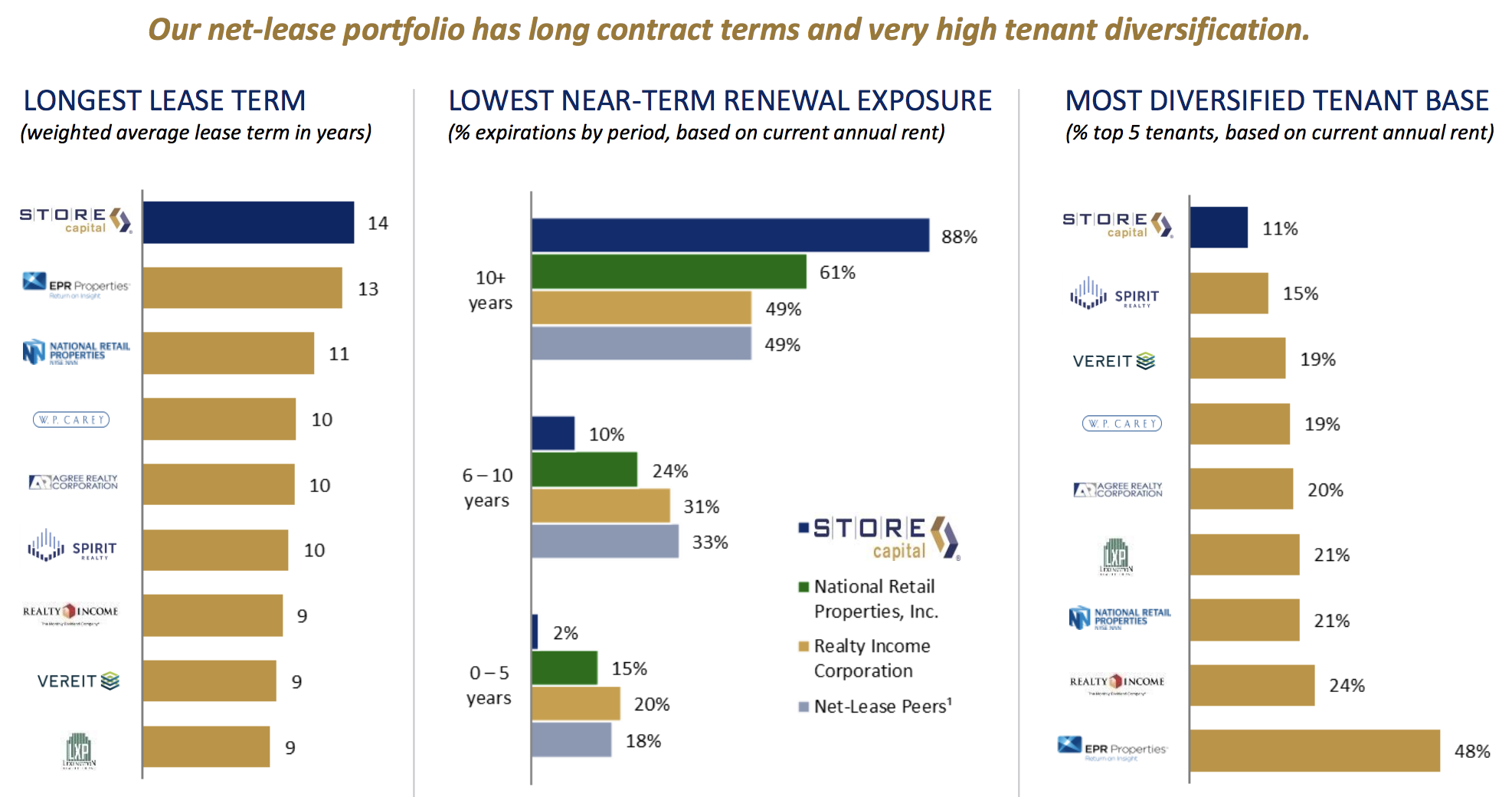

First, the company has the industry's longest average remaining lease term, at 14 years, though this is largely a function of being so new. Just 16% of the firm's leases are set to expire over the next decade, creating a very stable source of cash flow as long as its tenants can continue paying their rent obligations in full.

And despite its relatively small size, the REIT also has one of the most diversified property portfolios, with only 11% of its rent coming from its top five tenants. In fact, STORE's single largest tenant makes up just 2.7% of its cash flow.

Source: STORE 10-K

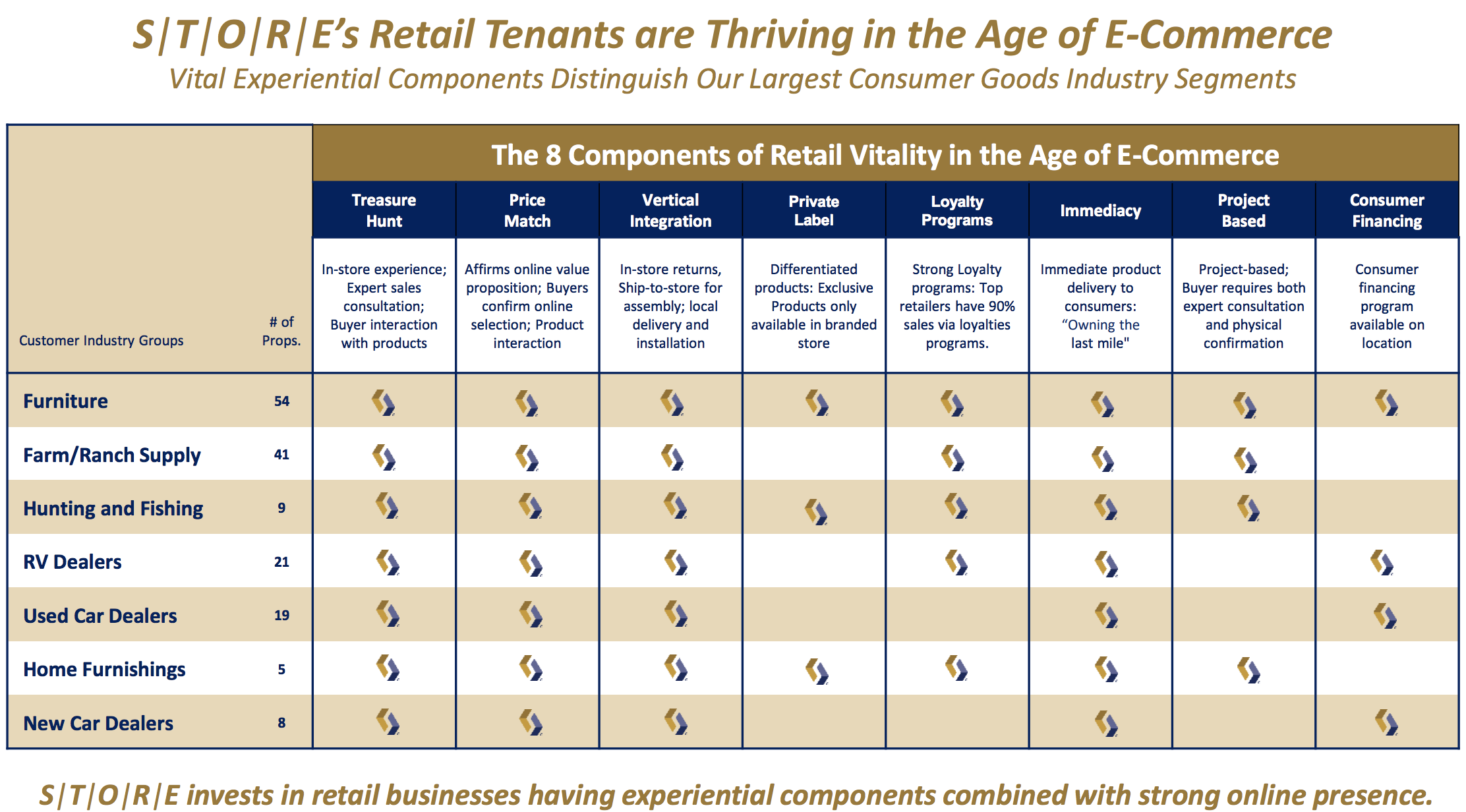

The company's retail exposure, which is among the smallest in the industry, is mostly focused on furniture and has proven relatively e-commerce resistant compared to other retail industries like sporting goods, electronics, and apparel.

Source: STORE Investor Presentation

STORE's cash flow stability also benefits from the fact that its properties are leased out to tenants in over 100 industries, meaning the REIT has minimal exposure to any single industry (full service restaurants are its biggest exposure at approximately 11% of base rent). In fact, among its peers STORE's customer concentration of its top five tenants is the lowest by far.

Source: STORE Investor Presentation

The third component of a quality REIT is its ability to grow profitably over time. Specifically, its ability to make acquisitions that are accretive to adjusted funds from operation, or AFFO (similar to free cash flow for REITs).

REITs must legally pay out 90% of taxable income as dividends. This means that they retain far less cash flow than most companies with which to grow their businesses. Thus REITs frequently turn to debt and equity markets to fund their growth.

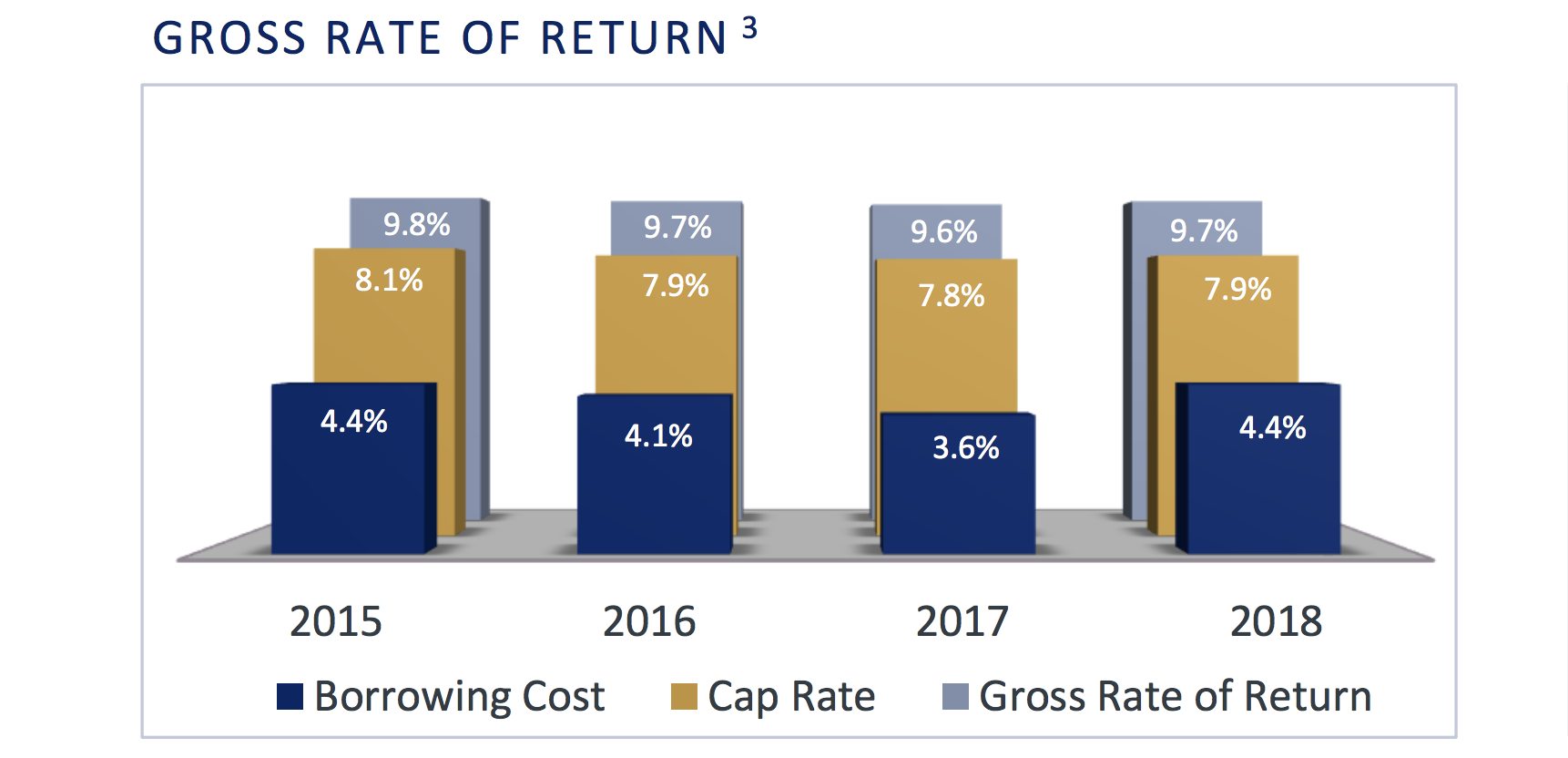

Whether or not that growth is profitable, however, depends on two things: the REIT's cost of capital, and the cash yield on new properties (called the "cap rate").

If the company's weighted cash cost of capital (taking into account retained AFFO, debt, and new equity sold) is not lower than the cap rate, then a REIT's marginal cash flow from new properties won't cover its higher interest and dividend costs.

In other words, the REIT will grow for growth's sake only, but AFFO per share will stagnate or decline. As a result, the dividend becomes less safe over time and is less able to be safely increased.

Fortunately, STORE has solid growth potential thanks to having one of the industry's lowest costs of capital. As you can see, STORE's cost of capital is well below its lease rates, providing a stable and profitable spread as it continues expanding its portfolio.

Source: STORE Investor Presentation

The company's low cost of capital is a function of two main things. First, management has been highly disciplined about how quickly it grows the dividend.

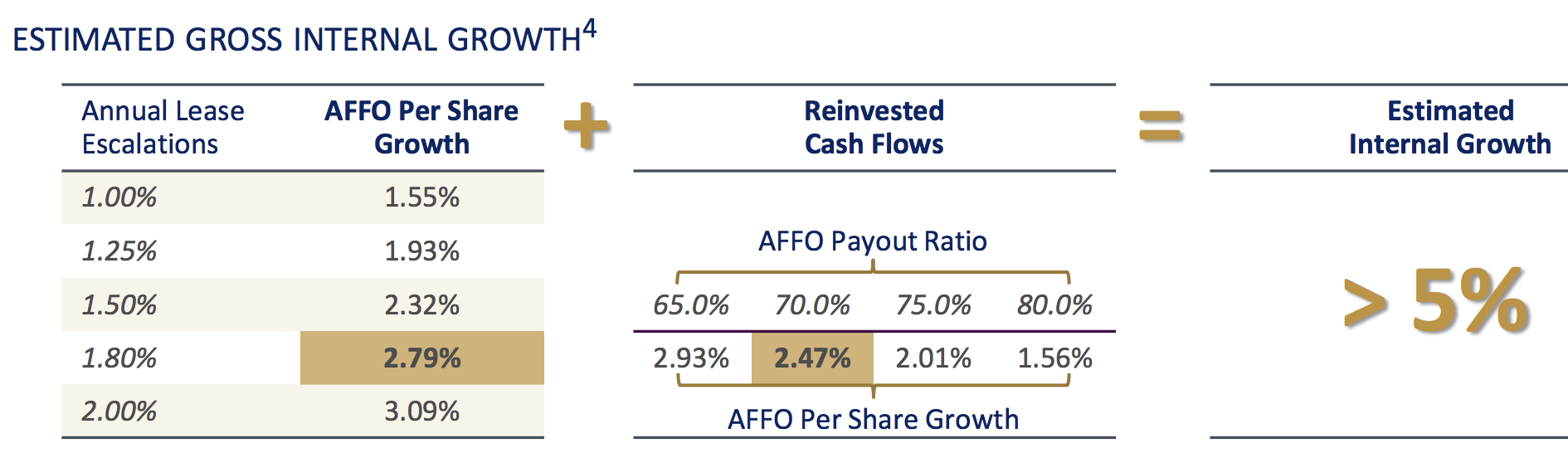

This allowed the REIT to maintain an AFFO payout ratio no higher than 70% (most triple net lease REITs pay out 80% to 90% of AFFO as dividends), creating greater protection and growth potential for its dividend.

A relatively low payout ratio also means STORE retains around 30% of its internally generated cash flow, which it can reinvest in growth projects. As a result, STORE is less dependent on debt and equity markets.

In fact, STORE's relatively large amount of retained cash flow, when combined with its rental escalators, means that it is capable of growing AFFO per share organically (without new property acquisitions) by at least 5% per year.

Source: STORE Investor Presentation

The other reason for STORE's low cost of capital is the REIT's cheap borrowing costs. This is thanks to management's disciplined use of debt, which has earned the company a solid BBB investment grade credit rating from Standard & Poor's.

The company's investment grade credit rating helps STORE to borrow money on very long terms (locking in its cost of capital) and allows for industry leading investment spreads (cash yields minus the cost of capital).

Having easier access to relatively cheap debt is important because STORE appears to have a long growth runway. In fact, there are currently over 2 million single occupant properties that have a combined value of $3.4 trillion.

Management estimates that STORE's specific type of target properties number over 200,000 and put the REIT's market share in these areas at about 2%. In other words, given the market's fragmentation, management's experience, and the company's low cost of capital, STORE seems likely to continue generating mid-single digit AFFO per share and dividend growth for the foreseeable future.

While STORE is a well-run REIT, there are still some challenges it may face in the future.

STORE's impressive growth rate of the past may not be sustainable over time, for example. For one thing, as its property portfolio increases in size, it's harder to move the needle and maintain strong growth rates of 6% to 8%.

That's especially true given how disciplined management is with its acquisitions. Approximately 80% of STORE's purchases are from management's deep ties in the industry and thus sourced through its business-to-business (B2B) connections.

In other words, STORE's industry-leading profitability is partly due to management's ability to locate excellent deals, with quality tenants, at attractive prices. However, there might be a limit to how many of these great deals STORE can come up with, especially since cap rates have declined in recent years due to rising competition from an increasing number of other triple-net-lease REITs and private equity players.

Low interest rates and continued economic growth have helped inflate commercial property prices, making it harder to find attractively valued properties to purchase. STORE has managed to continue investing at high cap rates despite these headwinds, but this isn't guaranteed to continue forever.

This could result in somewhat slower AFFO per share and dividend growth, but STORE's long-term outlook seems likely to remain intact.

Another risk to consider is that STORE's focus on service-oriented tenants could serve as a double-edged sword.

On one hand, STORE’s tenant base is largely immune from current industry challenges (the decline of certain kinds of brick-and-mortar retail). However, in a recession, discretionary spending at businesses like restaurants and movie theaters can fall significantly.

These kinds of properties are also usually more specialized and can take longer to find new tenants if existing ones fail. Rather than pay to refurbish an empty property (which is generating negative cash flow because of maintenance, insurance, and tax costs), a triple net lease REIT will sell empty properties to reinvest the capital into new properties with healthy tenants and brand new long-term leases.

However, the number of property dispositions can be volatile and fluctuate with the economy, as well as other factors (local property markets). In years when dispositions are very high, cash flow growth can slow or even potentially fall.

If a REIT's AFFO payout ratio is low enough, like STORE's, such periods are unlikely to put the dividend at risk. However, the short-term hiccup in growth means that dividend growth can come in lower than investors expected and the share price can suffer.

Closing Thoughts on STORE Capital

Before Berkshire bought his stake in the company, not many investors had heard of STORE Capital.

While the relatively young REIT is still far from earning the label of a blue chip, its disciplined management team, conservative payout ratio, healthy balance sheet, low cost of capital, large and fragmented target market, and solid dividend growth potential mean that STORE could be a worthy high-yield investment to keep an eye on for a diversified income portfolio.