Merck (MRK) has deep roots that date back to 17th century Germany, but the company was officially founded in the U.S. in 1891. Merck has since grown to become one of the largest pharmaceutical giants in the world, with a presence in over 140 countries. Merck organizes its business into two segments:

Pharmaceutical (88% of 2017 revenue) makes patented drugs to treat all types of diseases and conditions, such as cardiovascular disease, type 2 diabetes, asthma, chronic hepatitis C virus, HIV-1 infection, fungal infections, hypertension, arthritis, osteoporosis, and fertility diseases.

This segment also offers antibacterial products, cholesterol modifying medicines, and vaginal contraceptive products, as well as vaccines for measles, mumps, rubella, varicella, chickenpox, shingles, rotavirus gastroenteritis, and pneumococcal diseases.

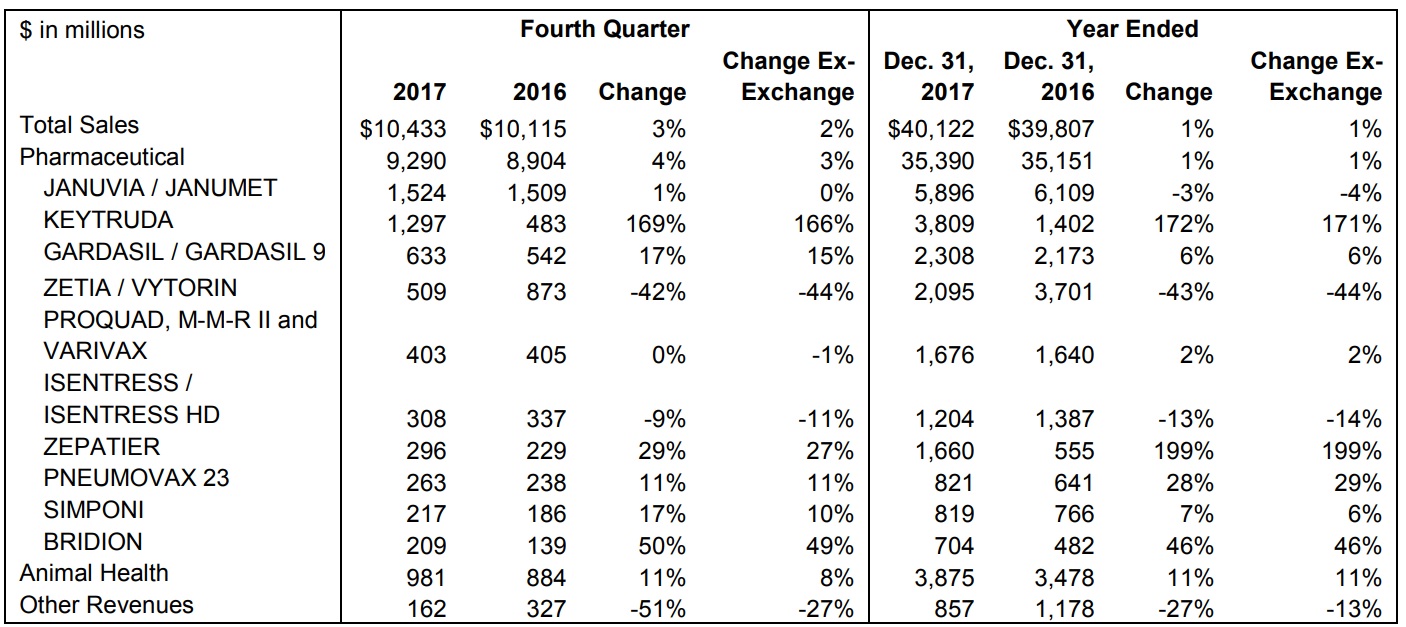

The bulk of the company’s sales, earnings, and free cash flow stem from just 12 main drugs, including blockbusters: Januvia (type 2 diabetes; 15% of company-wide sales), Keytruda (antibody based cancer drug; 10% of sales), and Human Papillomavirus (causes cervical cancer) vaccine Gardasil. These 12 blockbusters accounted for 53% of the company's total sales in 2017.

Source: Merck Earnings Release

Animal Health (10% of sales) this fast-growing segment sells antibiotic and anti-inflammatory drugs to treat infectious and respiratory diseases, fertility disorders, and pneumonia in cattle, horses, and swine; vaccines for poultry, parasiticide for sea lice in salmon, and antibiotics and vaccines for fish.

Merck’s 2017 sales were geographically diversified, with the U.S. responsible for 43% of revenue and international markets representing the other 57%.

Business Analysis

There are several characteristics that potentially make drug makers like Merck appealing dividend growth stocks.

First, the drug manufacturing industry enjoys meaningful competitive advantages thanks to: very high development costs (up to several billion dollars per drug), enormous regulatory hurdles (drugs can take up to 10-15 years to receive approval), and patent protection that grants windfall profits for a number of years.

In addition, the prescription drug market is recession resistant and benefits from the world's aging population, which is expected to boost healthcare spending over the decades ahead.

Merck has managed to build one of the world's largest drug development and marketing machines, giving it enormous economies of scale and access to far greater resources than most of its rivals. For example, in 2017 the company spent a whopping $10.2 billion on R&D, representing 25% of its total revenue.

Much of that spending was on drug trials for its largest potential blockbuster, cancer drug Keytruda. Keytruda is a PD-L1/L2 checkpoint inhibitor. It works by blocking a tumor's ability to circumvent the body's own immune system, which is generally very good at hunting down and killing tumor cells before they can multiply and threaten the body's health.

Clinical studies have shown that using Keytruda and chemotherapy nearly doubles treatment efficiency compared to chemo alone (from 29% to 55%). It also results in a 47% reduction in disease progression at 13 months, significantly improving overall survival odds.

Keytruda has been in development for over 9 years and participated in over 500 clinical studies. It's been tried in over 300 combination treatment programs, approved to treat 20 cancers, and launched in over 50 markets around the world. Merck has Keytruda in trials for 10 more indications (cancer types) and believes it might be effective against 30 more. In the coming year, the company hopes to launch it in over 110 additional markets.

All of which is why Keytruda sales almost tripled in 2017 to $3.8 billion and represented over 12% of company-wide sales during the fourth quarter last year.

Analysts expect Keytruda sales to grow to $6 billion in 2018, with upside potential to hit $10 billion in annual revenue by 2022. However, unlike some pharmaceutical/biotech companies, even at its peak Keytruda would likely only represent around 20% of the company's sales.

In other words, Merck remains diversified enough to never rely on just one blockbuster for the majority of its sales, earnings, and free cash flow.

Today Merck has 35 drugs in its pipeline, including promising candidates to treat some of the biggest future problems of a rapidly aging world. These include: heart disease, diabetes, cancer, and Alzheimer's.

Source: Merck

Merck's development pipeline also includes biosimilar (i.e. biological generics) versions of other blockbuster medications, which had combined sales of about $40 billion in 2017 and offer plenty of opportunity for new competition.

All told, Merck has a number of moving parts but seems likely to grow its earnings per share and dividend at a low to mid-single-digit rate going forward. The company has been a very reliable income stock historically, maintaining or raising its annual payout for 26 consecutive years.

Key Risks

Despite Merck's impressive long-term track record, the pharmaceutical industry is one that is fraught with numerous risks, including new drug development.

For example, just one in 10,000 new potential compound/treatment candidates makes it through the FDA's increasingly rigorous three-stage human trial approval process. That process can take anywhere from 9 to 15 years to complete and cost as much as $2.7 billion in total pre-clinical and post-clinical follow-on monitoring. And those costs have been climbing over time as drug development becomes ever more complex and FDA safety and approval standards become stricter.

In other words, there is a lot of uncertainty about whether large R&D spending will actually pay off. In the past, Merck has faced major setbacks and drug trial failures in numerous promising products including:

Cardiovascular disease drugs Tredaptive, Rolofylline, and TRA

Telcagepant for migraines

Osteoporosis drug odanacatib

In addition, there have been setbacks with Keytruda as well. In 2017, a disappointing study caused Merck to withdraw an application in the European Union for making Keytruda a first line treatment for lung cancer. Lung cancer is the most profitable market for oncology due to the large number of cases caused by smoking.

That same year regulators changed the benchmarks on a study involving Keytruda and chemotherapy. Rather than focus on improved outcomes relative to current treatments, the study will be looking at overall gains in survival rates. This is expected to push back the results of the study to February of 2019.

If the outcome of this study is also disappointing, this could cause Keytruda future sales potential to fall. Furthermore, Keytruda isn't the only PD L1/L2 checkpoint inhibitor on the market.

Bristol-Myers Squibb's (BMY) Opdivo is a similar drug that is expected to also generate $10 billion in sales by 2022. If Opdivo has greater drug trial success for increased indications, than it could end up stealing market share from Keytruda.

Even if Keytruda is as successful as the company hopes, Merck, like all drug makers, faces a major challenge with growing its sales over time. This is because drug patents are granted at the beginning of the development process and typically last for 20 years.

However, since it takes so long to get approval for a drug, the actual amount of time a pharmaceutical company has to enjoy windfall profits can be as short as five years. At that point, generic competition can quickly erode market share and pricing power.

Merck's revenue growth is likely to remain very low due to some major patent expirations it is facing on cholesterol drugs Zetia and Vytorin (generic competition likely in 2017 and 2018, respectively), as well as the decongestant Nasonex. These three drugs combined for about 5% of sales in the last year.

In other words, drug makers face a blockbuster and patent cliff-fueled boom and bust cycle. And due to the large costs associated with R&D, long development phases, and the uncertain nature of drug trial outcomes, the pharmaceutical industry is one of the most M&A dependent in the world. However, large acquisitions pose significant risk, too.

Not only does a drug maker have to avoid overpaying for a rival (and its drug development pipeline), but it also has to smoothly integrate that rival's corporate culture into its own. All while achieving the synergistic cost savings that usually underpin the profitability of the entire deal.

Merck has made some very smart acquisitions in the past. For example, in 2009 the company bought Schering-Plough to diversify its business ahead of a major upcoming patent cliff. Merck paid a fair price for Schering and in the process obtained a large pipeline of promising drugs including Keytruda.

However, Merck, like almost all drug makers, has also made some pretty bad acquisitions. These include its 2014 purchase of antibiotic maker Cubist for $9.5 billion (including debt assumption).

Cubist's top seller, Cubicin, was facing potentially fierce generic competition. In 2015, a federal district court invalidated four of Cubucin's patents which allowed generic rivals to hit the market by 2016. And by 2017 the drug had lost all patent protection and has seen a steady slide in sales.

Merck has said it may withhold from any M&A activity this year and next in an effort to reduce its debt, which would be a welcome move to reduce risk. The company's balance sheet stretched when Merck acquired lab equipment manufacturer Sigma-Aldrich for $17 billion in 2015, its largest deal ever.

Besides M&A risk, drug makers face the unpredictable regulatory risks involving government-funded medical spending, both in the U.S. and abroad. Remember that in many countries national governments foot a large part (or all) of medical costs. That can be a point of contention given the high price of many treatments.

The cost of one year of Keytruda and chemotherapy, for example, is typically $272,000. The average course of treatment is eight months, meaning that the average cost for treatment to a medical system is $172,000.

With an aging global population pushing up medical costs on both private and public health systems, there are increasing calls for price controls on certain important drugs.

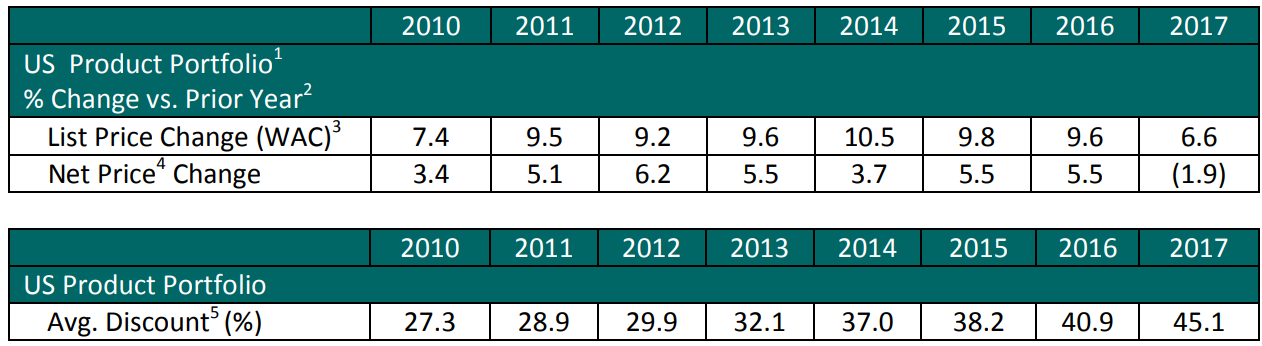

Pharma companies have responded to this pressure (as well as the continued rise of generic drug manufacturers) by slowing their pace of price increases. You can see that Merck's U.S. product portfolio actually saw its net price decline 1.9% in 2017, and its average discount has increased meaningfully since 2010.

Source: Merck

Even if regulations are not put in place to help alleviate rising medical costs, the U.S. Congress can always change current laws which prevent Medicare/Medicaid from negotiating bulk drug purchases. This would represent a less controversial and easier cost saving initiative for lowering medical spending that might negatively impact all drug maker profit margins.

Finally, as if all of these risks weren't enough, there are also legal liabilities to consider. Even if a drug makes it through the incredibly expensive, uncertain, and time consuming development process, a drug can ultimately prove to be unsafe and harmful, resulting in costly legal bills.

For example, in 2004 post approval safety studies showed that Merck's popular painkiller Vioxx significantly increases the risk of heart attack and stroke. The company pulled the drug off the market but then spent the next 12 years battling numerous class action lawsuits that ultimately resulted in nearly $6 billion in fines and settlements.

The point is that the pharmaceutical industry is one of the most highly complex and uncertain business models in the world. While high development costs, strict regulations, and patent protection can provide meaningful competitive advantages for the incumbents, all of these uncertainties can create lots of sales and earnings volatility over time.

As a result, it's usually best to stick to the industry-leading blue chips in this space, companies who have long track records of paying safe and growing dividends to prove that they've mastered the very difficult drug development and marketing process.

Closing Thoughts on Merck

The pharmaceutical industry has high barriers to entry and can be very profitable, but it is also extremely complex. Conservative investors considering the space are best off sticking to the industry's largest and most proven names.

Merck is certainly one of those, with a long history of navigating the challenging pharma waters while delivering safe and steadily growing payouts. The company's strengths come from its solid balance sheet, reasonably diversified drug portfolio, excellent free cash flow generation, and time-tested drug development processes.

With that said, Merck's dividend growth potential and portfolio diversification are still inferior to some of its rivals, such as Johnson & Johnson (JNJ) and Pfizer (PFE). Investors looking to be extra selective may consider reviewing those alternatives instead.