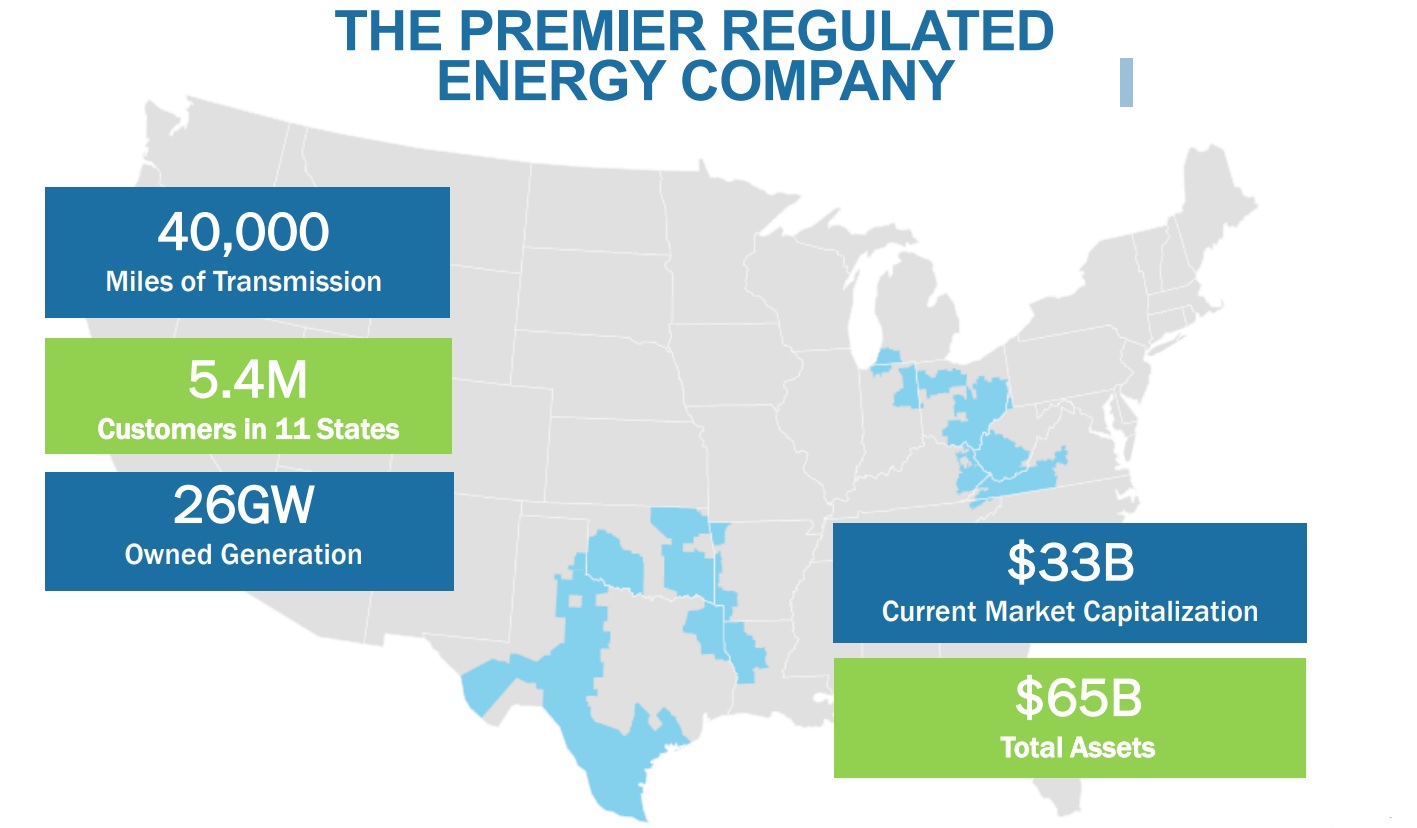

Founded in 1906, American Electric Power Company (AEP) is one of America’s largest electrical utilities. The company's 26 gigawatts of power production capacity, 40,000 miles of power lines, and 224,000 miles of distribution lines serve 5.4 million customers in 11 states including: Kentucky, Michigan, Texas, Oklahoma, Indiana, West Virginia, and Ohio.

Source: AEP Investor Presentation

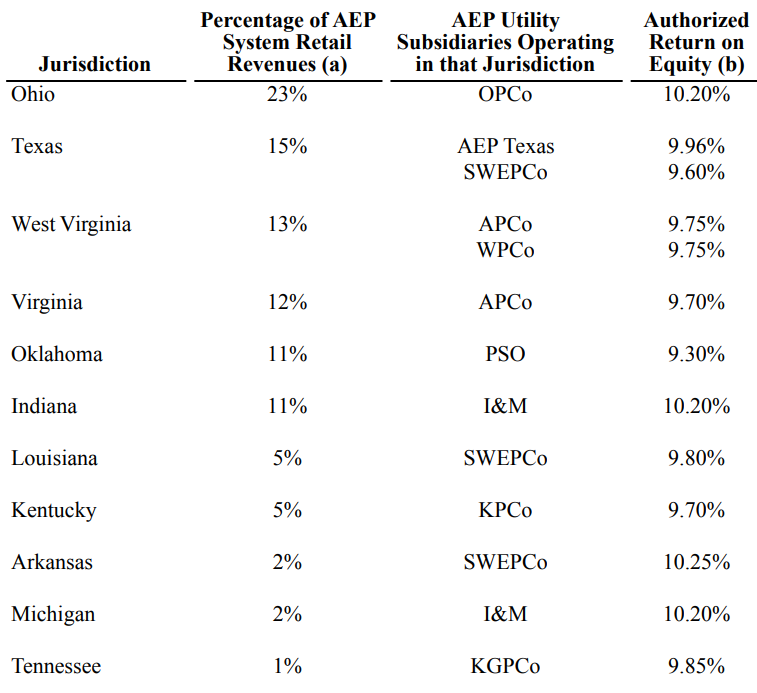

Ohio is the company's most important state, representing 23% of total retail revenue. Texas (15%), West Virginia (13%), Virginia (12%), Oklahoma (11%), and Indiana (11%) are also important contributors. You can see that the company's authorized return on equity ranges between 9% and 11% across all of its regions, which is about average for the industry.

Source: AEP Annual Report

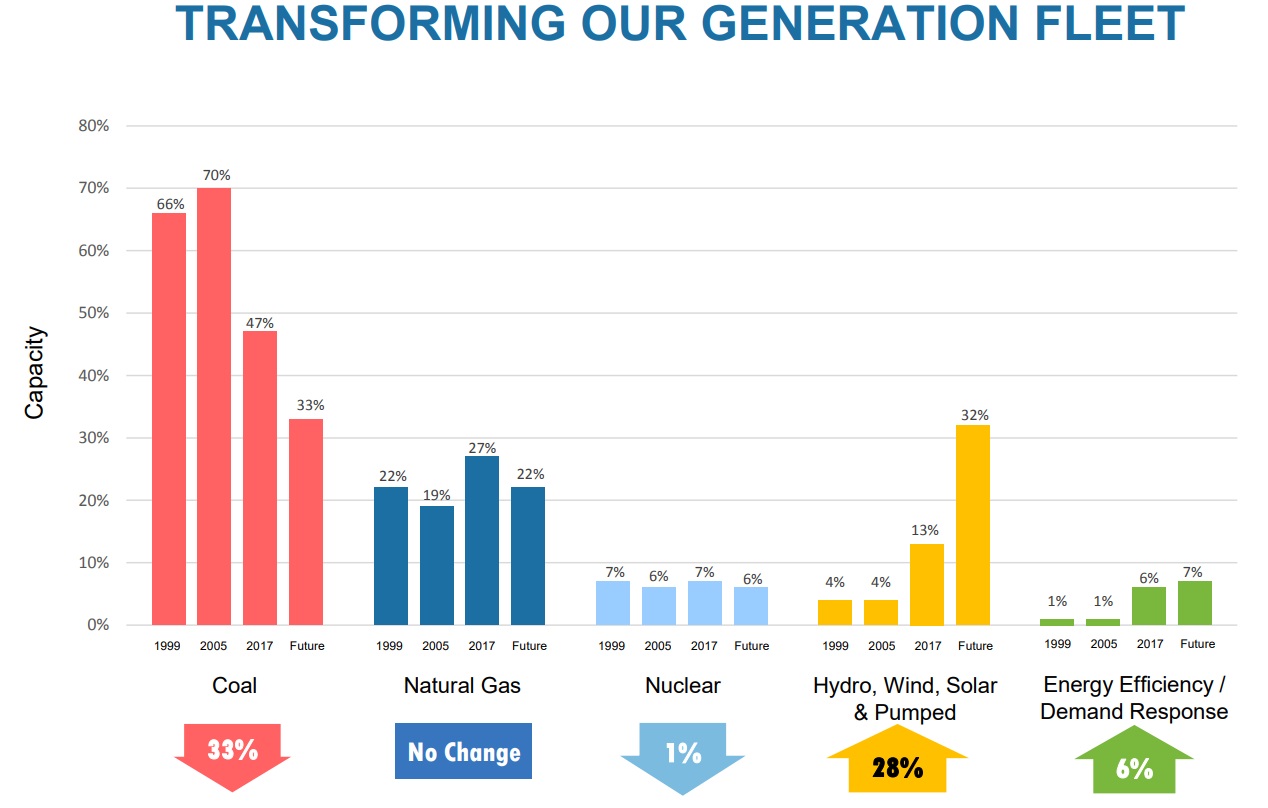

Like many U.S. electric utilities, AEP relies on a substantial amount of coal-fired power (70% of capacity in 2005). However, in recent years stricter environmental regulations, plunging natural gas prices, and steadily declining costs of renewable energy, such as wind and solar, have caused the utility to shifts its energy mix away from coal and towards cleaner sources.

Coal accounts for less than 50% of AEP's generation fleet today, with a long-term goal of 33%. Meanwhile, hydro, wind, and solar generation has increased from 4% of capacity in 2005 to 13% in 2017. Management expects over 30% of AEP's power generation fleet to come from these sources in the future.

Source: AEP Investor Presentation

In an effort to grow earnings faster, AEP, like many utilities, also attempted to diversify into unregulated merchant power production. However, the company ultimately reversed course and sold off its merchant power business in late 2016, as well as legacy coal-fired plants in Ohio that were no longer economical.

By the end of 2018, AEP is expected to sell off almost all of its remaining merchant power assets, meaning that its highly stable regulated business will go from about 70% of revenue in 2016 to almost 100% in 2019.

Business Analysis

Regulated utilities have several qualities that can make them appealing high-yield income stocks. Most of these companies are essentially government-sanctioned monopolies with locked in customer bases, exclusive rights within their service areas, and guaranteed returns on capital set by regulators to incentivize continued investment into their asset base.

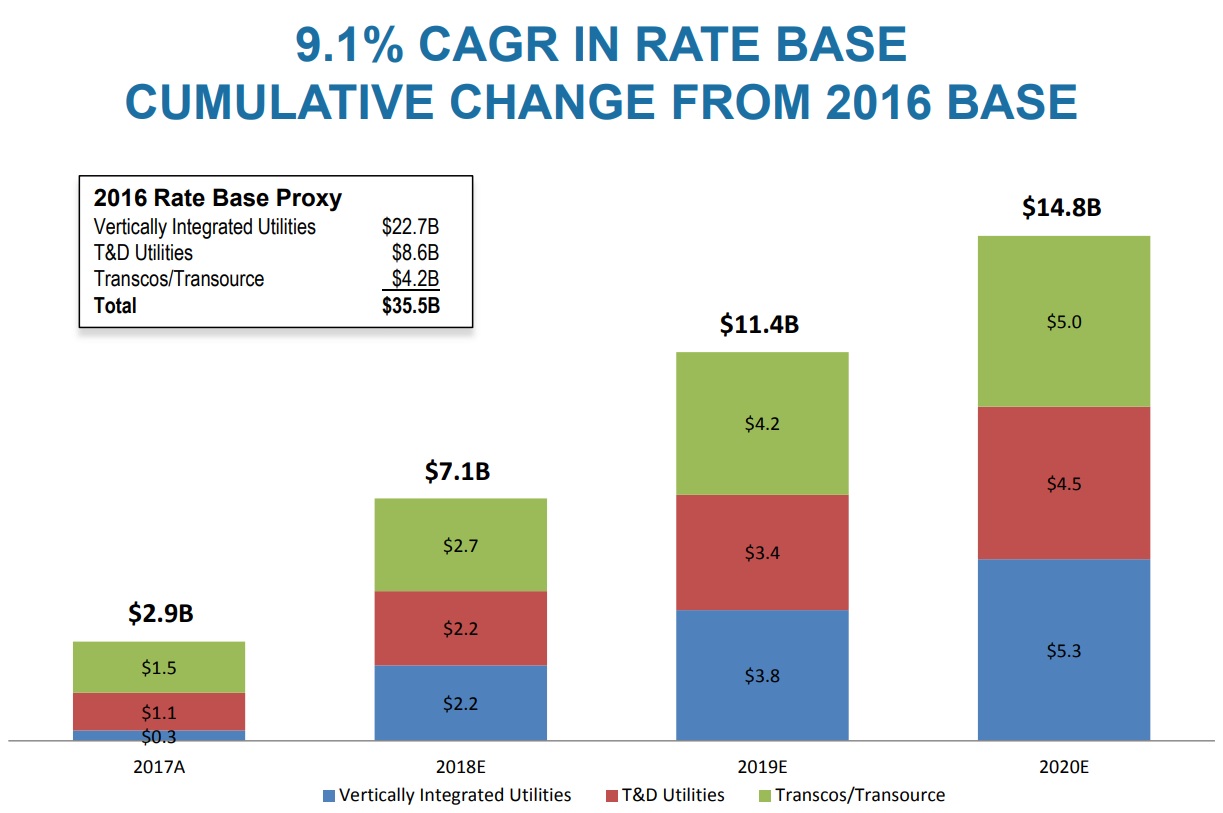

The most important driver of utility earnings is growth of the rate base. Rate base is the assets on which a company earns its allowed return on equity.

American Electric has been growing its rate base at a relatively fast pace thanks to large amounts of investments into maintaining, upgrading, and expanding its infrastructure network.

Source: AEP Investor Presentation

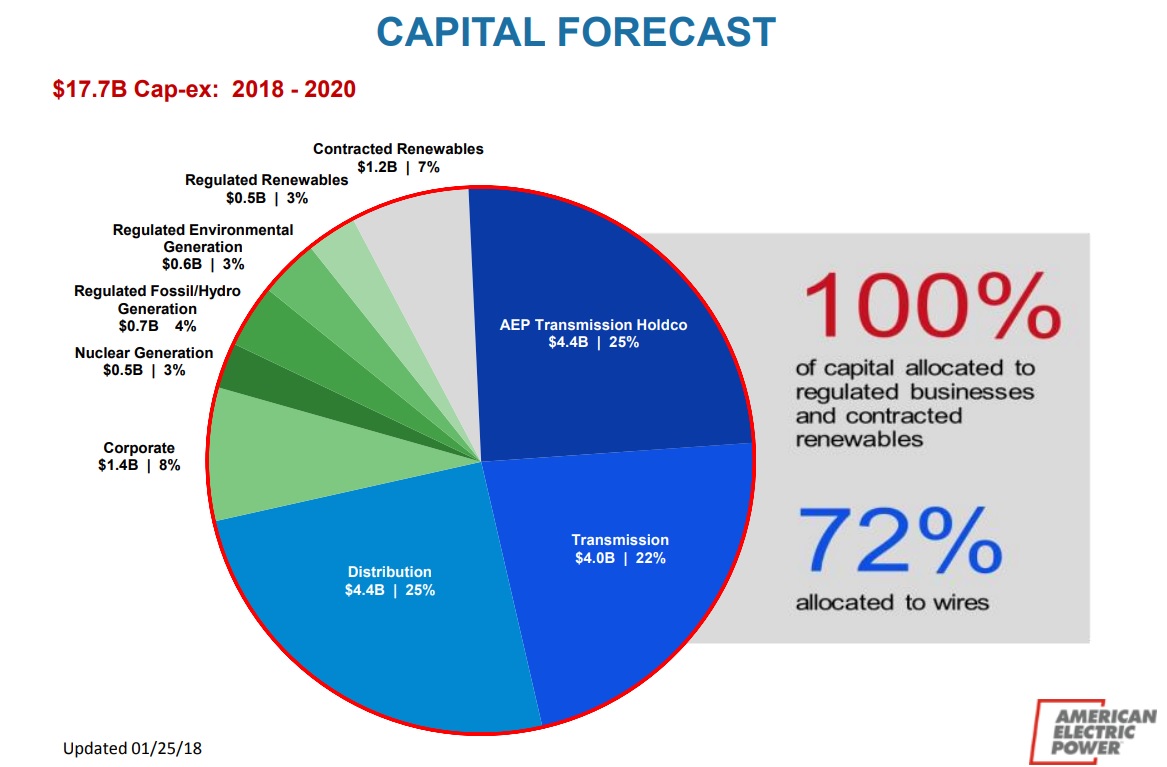

Management expects to invest $17.7 billion, or $5.9 billion per year, into approved growth projects between 2018 and 2020. Importantly, the vast majority of this spending is going into regulated investments and wires, which are lower-risk projects that will provide greater reliability for AEP's customers.

Source: AEP Investor Presentation

In recent years, AEP has struggled in its large Ohio segment, thanks in part due to that state's decision to deregulate its electric industry in 2001. This move helped save electric customers an estimated $3 billion a year, by pitting regulated utilities like AEP and Duke Energy (DUK) against numerous smaller merchant power producers. These producers enjoyed several competitive advantages including newer, more efficient gas fired plants, which require less maintenance and had much lower fuel costs.

Both utilities have lobbied, unsuccessfully, to re-regulate the state's power industry. With little prospect for success, the company decided to sell off four legacy coal plants in 2017 and instead focus on two major growth areas.

The biggest of these is electrical distribution, which has the most favorable regulatory environment in the industry. That's because America's large and aging electric grid is in major need of upgrades and maintenance. For example, the useful life expectancy of electric transformers and transmission lines is about 60 and 70 years, respectively. AEP's average transformer and transmission line is now 41 and 52 years old, respectively.

The major need to maintain, enlarge, and improve this network means that regulators are willing to approve projects and grant them attractive returns on equity between 9.6% and 12.8%. This is why AEP has moved all of its transmission and distribution related assets into a separate holding company and plans to spend 72% of its capex budget ($4.25 billion per year) on high profitability transmission projects.

That in turn is expected to drive 29% earnings growth from this business, whose share of the company's overall earnings is expected to rise from 17% in 2017 to 22% in 2020. The other major reason that American Electric likes the transmission and distribution business is because it ties into another growth catalyst, renewable energy.

American Electric currently has 4.3 gigawatts of renewable power capacity, but the company has enormous plans to grow this in the coming years. For example, AEP is planning on spending $1.8 billion on solar and wind projects over the next three years, not including America's largest clean energy project, the $4.5 billion 2 gigawatt Wind Catcher wind farm in Oklahoma. This project will single-handedly make Oklahoma the country's second biggest wind power producer behind Texas and is expected to be completed in the mid-2020s, assuming it gains regulatory approval.

By 2025 the company expects to add 5.6 gigawatts of renewable capacity, which represents 130% growth in solar and wind power generating assets. And by 2030, American Electric plans to have boosted its renewable capacity by a total of 8.3 gigawatts, or nearly 200%.

Solar and wind are expected to represent about 33% of the company's total generating capacity at that point. And since solar and wind projects are usually located far from urban areas, where its customers are, these projects will require immense investments transmission and distribution systems as well.

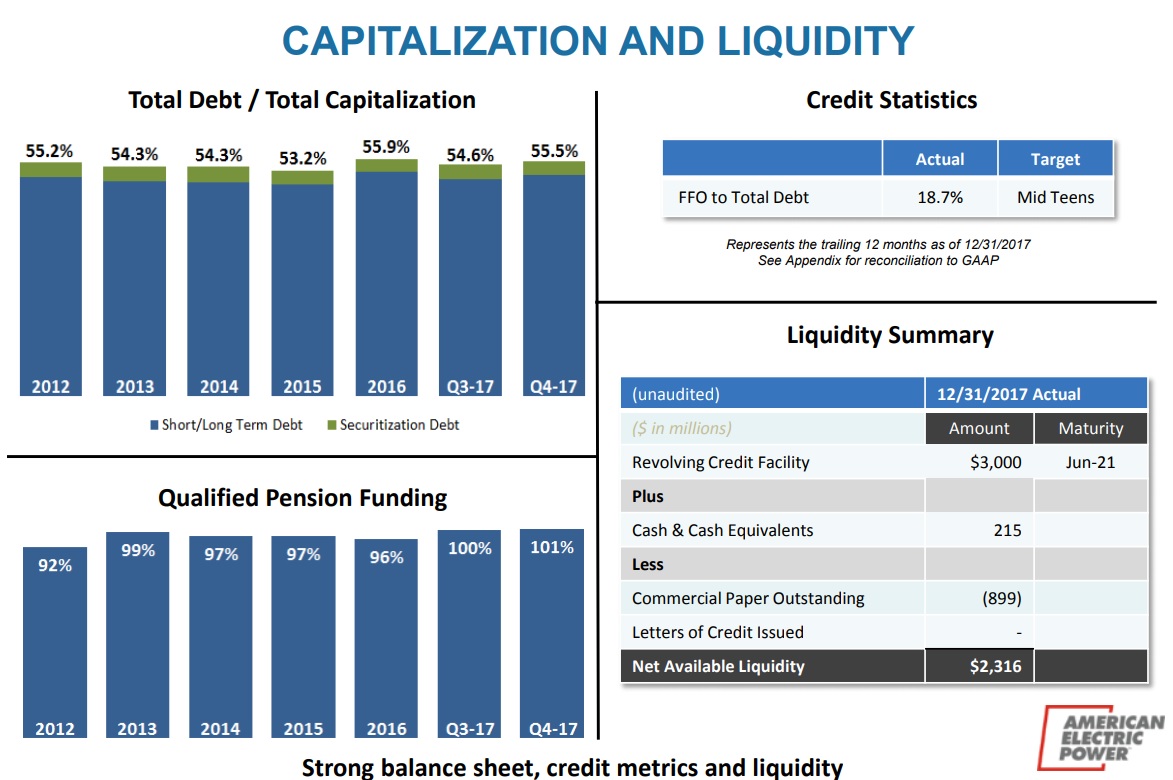

Of course, a large backlog of capex projects and a long potential growth runway is meaningless if a company doesn't have the financial resources to fund it, while still paying a generous and growing dividend. Fortunately, American Electric has a solid track record of balancing its growth without taking on excessive and dangerous amounts of debt.

For example, the utilities debt/capitalization ratio has been highly stable over time, and its pension plan is fully funded.

Source: AEP Investor Presentation

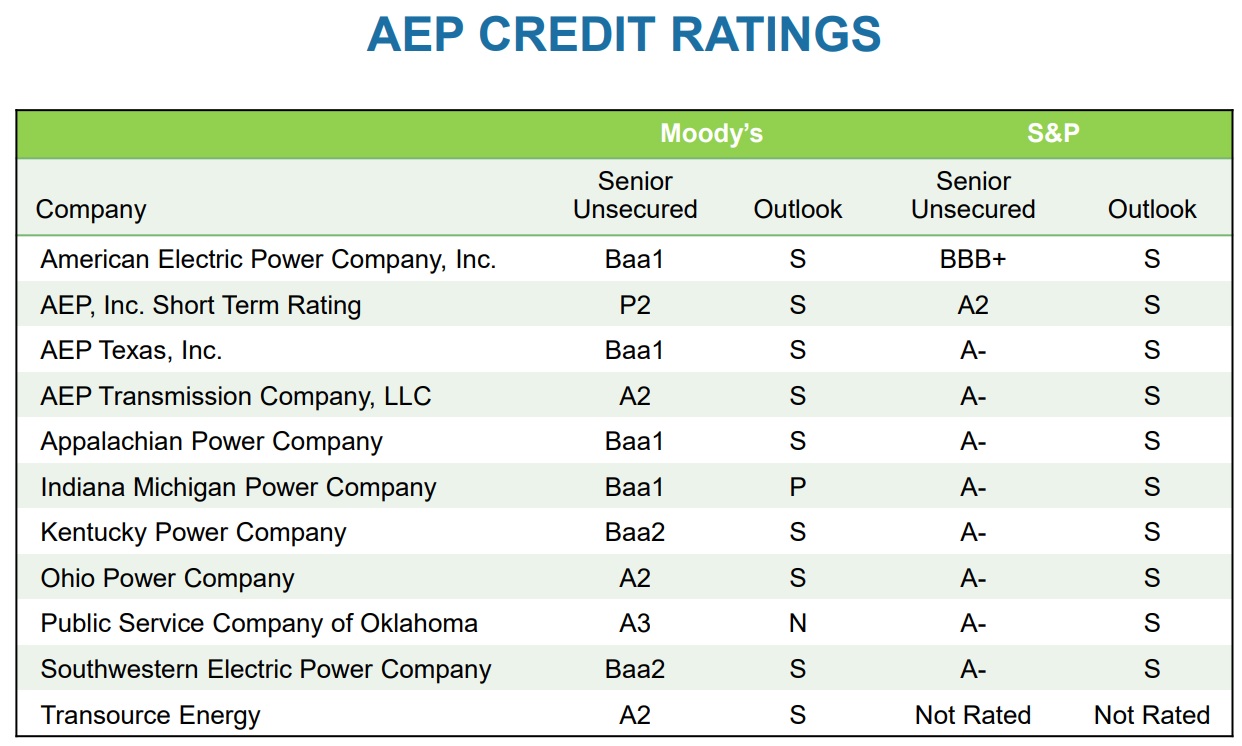

Importantly, AEP also enjoys low borrowing costs thanks to the utility's strong and stable investment grade credit ratings.

Source: AEP Investor Presentation

By using long-term fixed rate debt, the company can lock in its profitability and reduce its earnings sensitivity to rising interest rates, too. Going forward, management has a plan to reduce AEP's leverage ratio to about 3.1 to 3.4, slightly below the industry average. That should help ensure its credit ratings remain stable.

All told, management believes that the company's current growth plan will increase its rate base by about 8% annually through 2020, driving 5% to 7% earnings per share growth during that time. That should allow the utility to continues increasing its dividend at a pace of about 5% to 6% annually, making it a potentially attractive choice for conservative income investors.

Key Risks

Regulated utilities are inherently low-risk businesses, but no company is risk free. In the case of regulated utilities like AEP, the biggest risk is the company's ongoing relationships with its regulators.

For example, in 2018 the company will receive rate/investment decisions in numerous important markets including:

Indiana

Michigan

Kentucky

Oklahoma

Texas

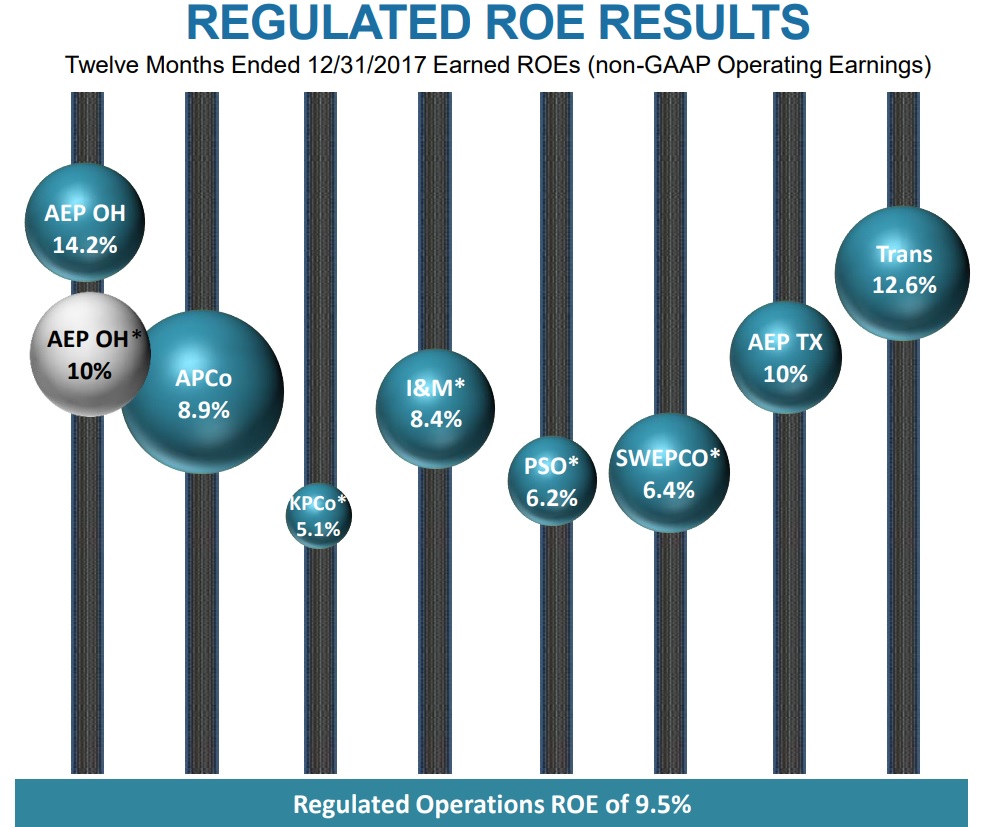

The most concerning of these are the decisions in Kentucky, Oklahoma, and the company's SWEPCO Texas subsidiary. All three business units are currently suffering some of the lowest returns on equity of any electric utility in America.

Source: AEP Investor Presentation

This has caused AEP's overall return on equity to decline from 10.4% in 2016 to just 9.5% in 2017. Note that the average electric utility return on equity in the U.S. is about 9.5%, and analysts are expecting the company's permitted ROE to eventually rise to a long-term average of 10.0%.

However, there is no guarantee that regulators in key markets will actually allow a greater return on equity. That's largely because the nature of this industry is that AEP can pass on almost all costs to consumers, and the company unfortunately has some potentially significant cost uncertainties going forward.

For one thing, AEP's long-term plans call for legacy coal plants to make up 33% of its energy mix, the majority of its base load power capacity. Coal faces far worse economics than gas plants because the U.S. shale gas boom has caused the price of gas to fall by more than 80% in recent years. Gas prices are expected to remain very low going forward.

As a result, AEP's legacy baseload capacity has higher operating costs than many other more gas-focused utilities. This might give regulators pause in authorizing a higher return on equity that could mean greater customer rate increases in the future.

The good news is that American Electric Power's business is spread across 11 different states, so the company is somewhat protected from an unfavorable regulatory outcome in any one region.

Besides the company's outstanding rate cases, AEP's large capex budget, which will drive long-term earnings and dividend growth, also creates risk.

If projects get delayed or come in over budget, the utility's customers must pay for it via higher rates. Therefore, proper execution on its growth plans is essential to maintaining healthy long-term relations with regulators to prevent unfavorable rate case decisions going forward.

Finally, be aware that because of the highly capital-intensive nature of this business, almost all utilities are sensitivie to interest rates for two main reasons.

First, rising long-term rates could mean higher borrowing costs. Regulated utilities are allowed to pass these costs onto consumers, so they won't hurt short-term profitability. But again, if rates rise too high over time, than regulators are less likely to approve generous returns on equity, so overall profitability and earnings growth can suffer.

The second way utilities are sensitive to interest rates is that they must fund a small portion of their growth capital spending via new equity issuances. American Electric expects to issue $700 million of new shares between 2018 and 2020, representing about 2% dilution, for example.

It should be noted that most regulated utilities sell 1% to 3% new shares each year, so AEP's equity issuance plans are actually better than average. However, most utilities still have their growth potential somewhat at the mercy of fickle equity markets.

Should long-term interest rates rise at a brisk pace, utility stocks could continue facing pricing pressure as they become relatively less attractive income options compared to risk-free Treasury bonds. If their share prices sag, they may need to dilute current investors at a greater rate. In this scenario, AEP's earnings and dividend growth rates could end up missing management guidance and investor expectations.

AEP's relatively low equity needs and investment grade credit rating reduce this risk, but it's worth keeping in mind for investors who are focused on the utility sector.

Closing Thoughts on American Electric Power Company

Regulated utilities can make for a reliable source of safe and growing income. American Electric Power Company has a large, diversified customer base, and its plans to focus 100% on regulated businesses going forward should make it an even more attractive high-yield stock with less fundamental risk.

The company's current growth plans also represent a logical approach to serving the long-term needs of its customers, including improved transmission reliability, increased power capacity, and the use of cleaner energy sources.

While AEP certainly faces some regulatory risks in certain markets, its company-wide regulatory profile is about average with solid diversification across states. Overall, American Electric Power could be a potentially decent choice for conservative income investors to consider.