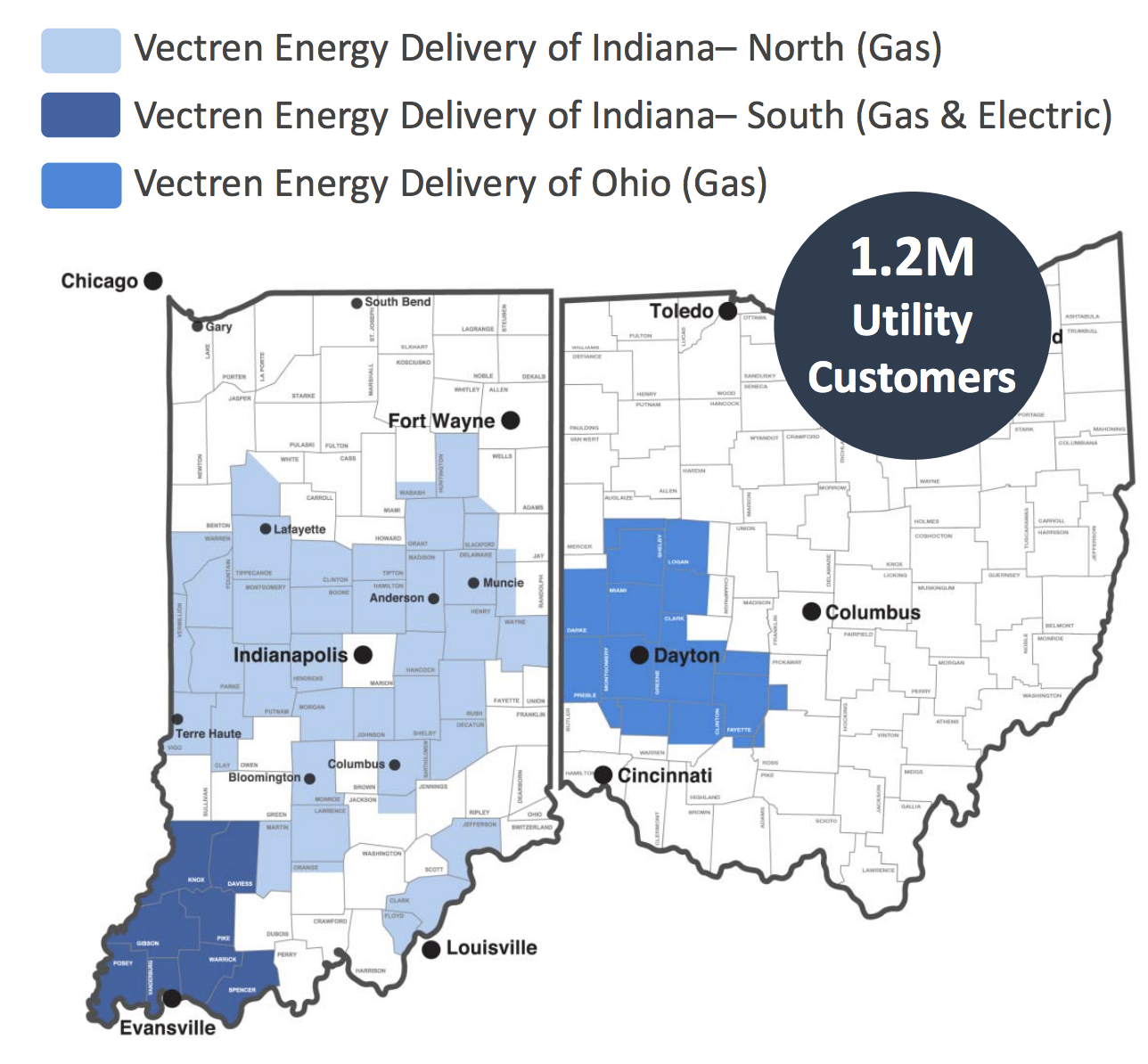

Formed in 1999 as the merger of two Indiana utility companies (one of whose roots date back to 1912), Vectren (VVC) serves natural gas (55% of utility earnings) and electricity (45% of utility earnings) to more than 1 million customers in central and southern Indiana as well as Ohio.

Source: Vectren Investor Presentation

Vectren’s customers in these areas are a healthy mix of residents, businesses, and industrial complexes. In its core natural gas business, 67% of 2017 revenue was from residential customers, 22% from commercial customers, and 11% from industrial customers.

Like all utility companies in the United States, Vectren is regulated by the public utility commissions (PUC) of the states in which it operates. These commissions set the prices utility companies can charge.

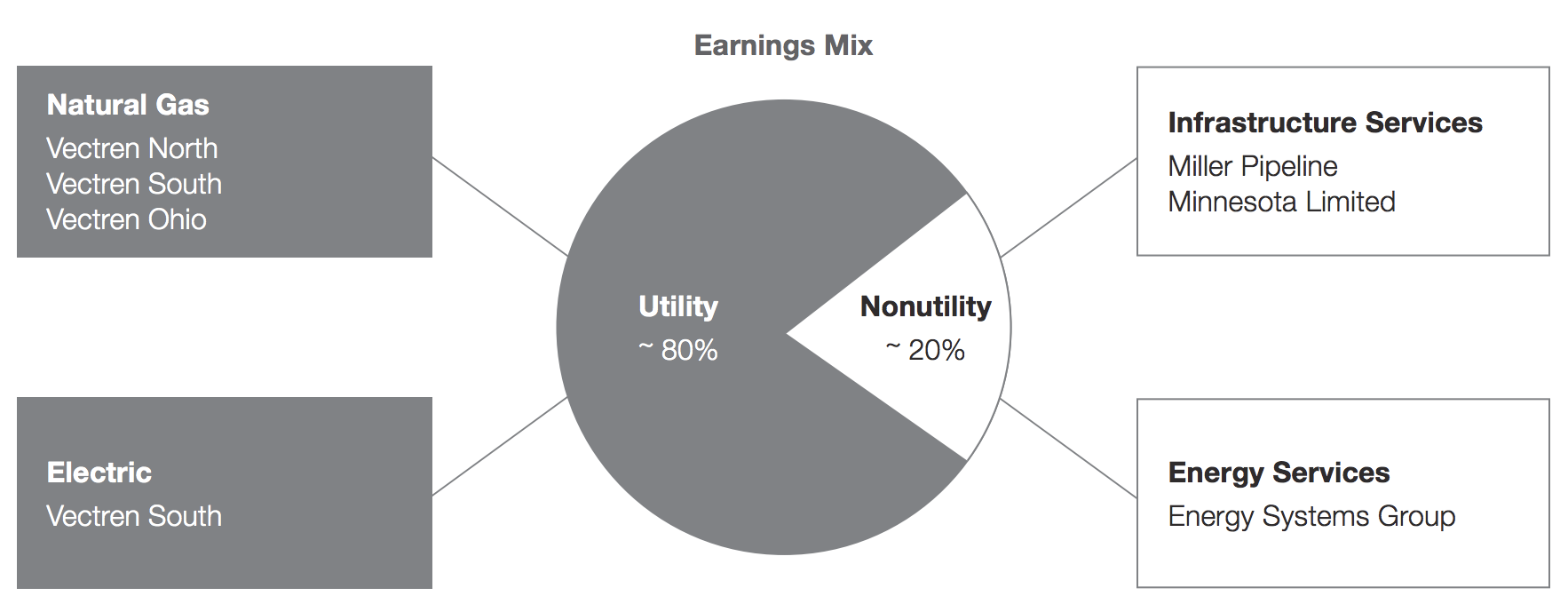

Vectren also runs a non-regulated business that provides pipeline construction and repair services to other utility companies and, to a lesser extent, energy contracting for large institutions like universities.

These unregulated, non-utility services account for about 20% of Vectren’s business each year and, unlike the company's regulated utility group, will benefit from U.S. tax reform.

Source: Vectren Annual Report

Business Analysis

“Location, location, location” is the mantra for most businesses. But for utility companies like Vectren, it’s “regulation, regulation, regulation.”

Enormous investments in infrastructure like generating stations and power lines are required to provide energy to people. As a result, competition in the industry is scarce, and were it not for regulation, utility companies would be able to charge exorbitant rates.

Thus begins the dance between regulators and utility companies. Regulators see to it that utility companies charge reasonable rates while also granting them the right to earn a profit.

This relationship between a utility company and its regulators is paramount. If poorly regulated, a utility company can fail. Pacific Gas & Electric, for example, declared bankruptcy in 2001 after California regulators refused a rate increase to compensate for soaring energy costs.

Thankfully for Vectren and its investors, the company has enjoyed a long history of favorable relations with regulators in Indiana and Ohio.

For example, the company's regulated utility group has earned a return on equity between 10% and 11% in each of the last six years, which is somewhat higher than the nationwide average.

With the cost of living already below the national average in both Indiana and Ohio, and savings from tax reform being passed on to customers, there’s also little reason to think that regulators in the two states will turn hostile towards Vectren and squeeze their profits.

That's especially true considering how stable Vectren's relationship has remained with regulators in both states. While the company did file a base rate case in Ohio in February 2018, there had been no change to the rate since January 2009.

The story is similar in Indiana. The company's gas utilities last filed a base rate case in early 2008 (the next case is expected to be filed in 2020), and Vectren's electric utility last faced a base rate case decision in 2011 (another case is expected to be filed in 2023).

Not surprisingly, S&P has issued both states' commissions a "Strong" rating, which bodes well for Vectren's future plans.

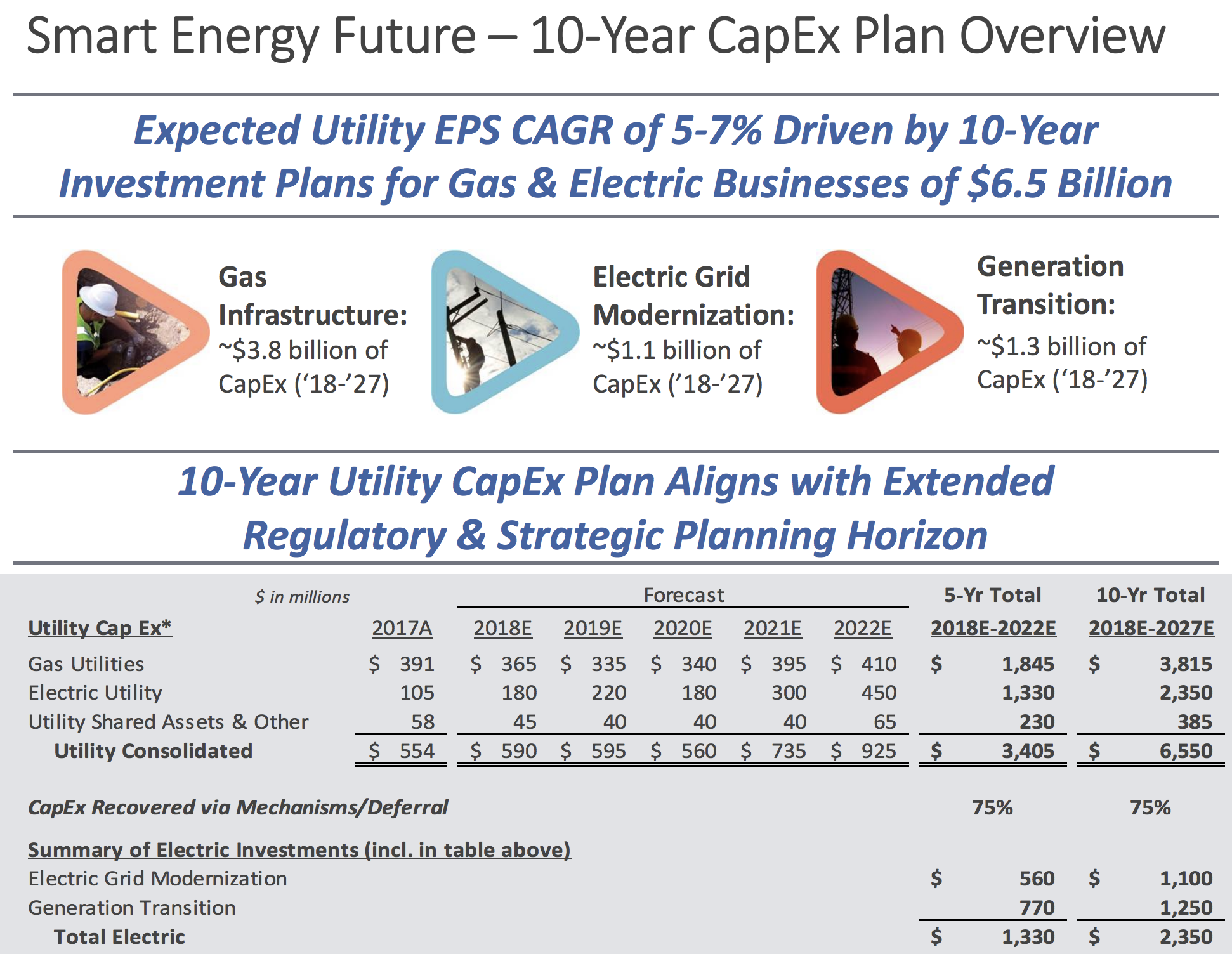

In 2017, the utility unveiled its Smart Energy Future vision to diversify its electric generation fleet and continue its ongoing gas and electric infrastructure modernization efforts across Indiana and Ohio.

Coal-fired plants account for 95% of Vectren's electric generation today, but that mix will change significantly over the next decade, assuming all goes according to plan. Management intends to begin building a new $900 million natural gas-fired power plant in late 2019 at the site of one of the company's coal-fired plants in Indiana.

Vectren has also requested approval to construct a new large solar farm for $75 million, with plans to bring it online by 2020.

The final piece of this plan is to retire three coal-fired generation units, lowering the carbon footprint of its fleet and providing customers with a more diversified energy mix to ensure affordable and reliable energy supply.

When combined with Vectren's substantial investments to modernize its gas infrastructure across Indiana and Ohio and continue improving the electric grid, the company its its utility earnings per share to grow 5% to 7% annually over the next 10 years. Importantly, the bulk of this spending will be covered by cash generated from operations, reducing financing risk.

Source: Vectren Investor Presentation

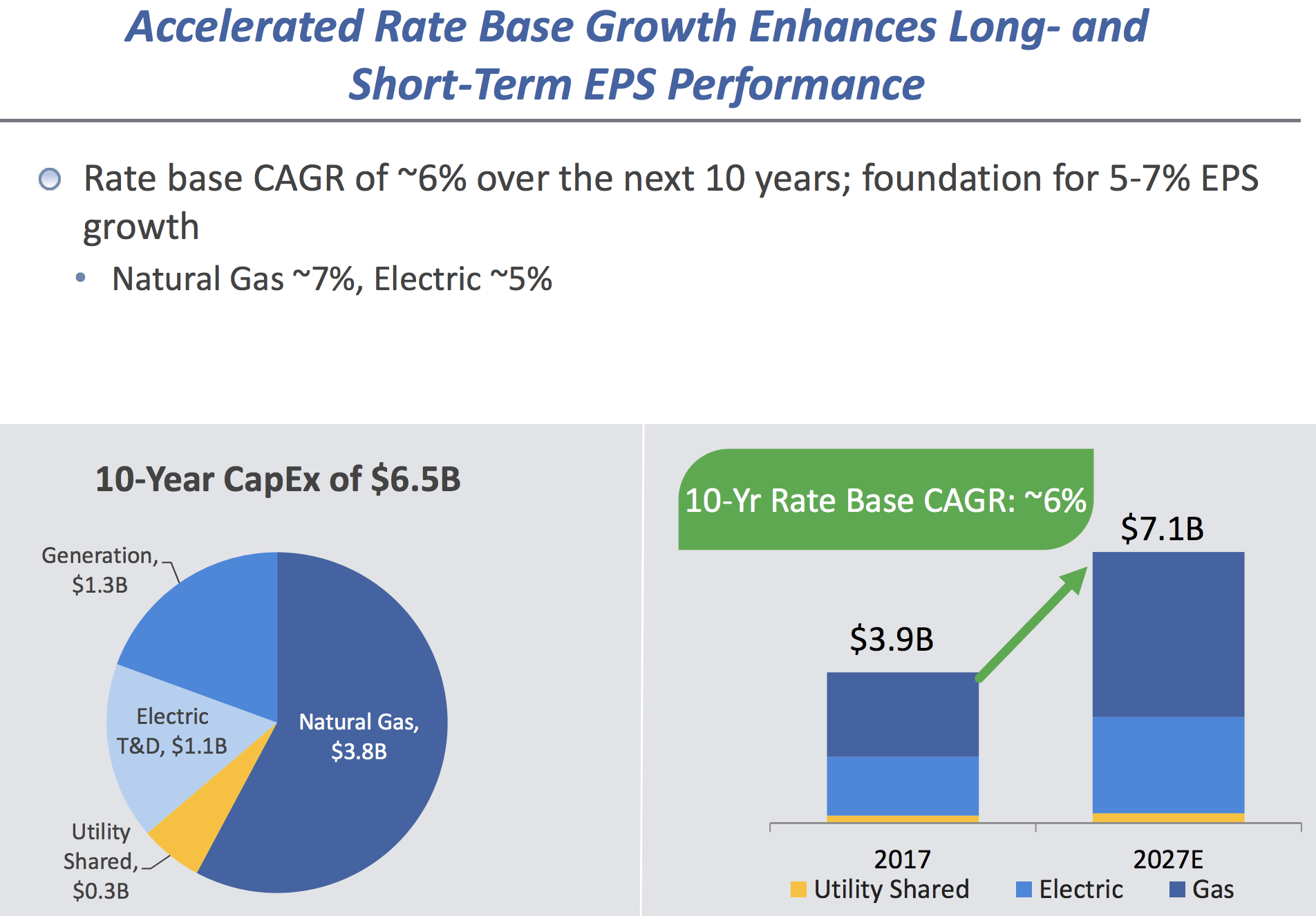

The $6.5 billion of gas and electric investments Vectren has planned over the next decade drive growth for utility companies, whose permitted revenues are tied to their “rate base”, or the value of their infrastructure. The higher Vectren’s rate base, the more revenue the company is afforded.

Vectren expects approximately 6% annual growth in its rate base over the next decade as a result of regulator-approved investments in infrastructure. Driven by its utility growth expectations, management believes long-term earnings per share and dividend growth will be in the 6% to 8% range.

Source: Vectren Investor Presentation

While mid-single-digit rate base growth is respectable for most utilities, it is still a rather slow pace overall.

To grow faster, the company runs two non-regulated, non-utility businesses that promise higher profit margins: infrastructure construction and energy contracting.

Through its infrastructure construction business, Vectren sells pipeline construction and repair services to other utility companies. These days, demand is high as states across the country work to replace their aging gas infrastructure.

Source: Vectren Investor Presentation

Vectren also does a wide range of projects for large institutions through its energy contracting business. For example, the company won a contract to build a power plant at NASA’s headquarters in recent years.

Although the energy contracting business accounts for only a small fraction of total revenue, the company’s backlog of energy contracts has picked up significantly in recent years.

Source: Vectren Investor Presentation

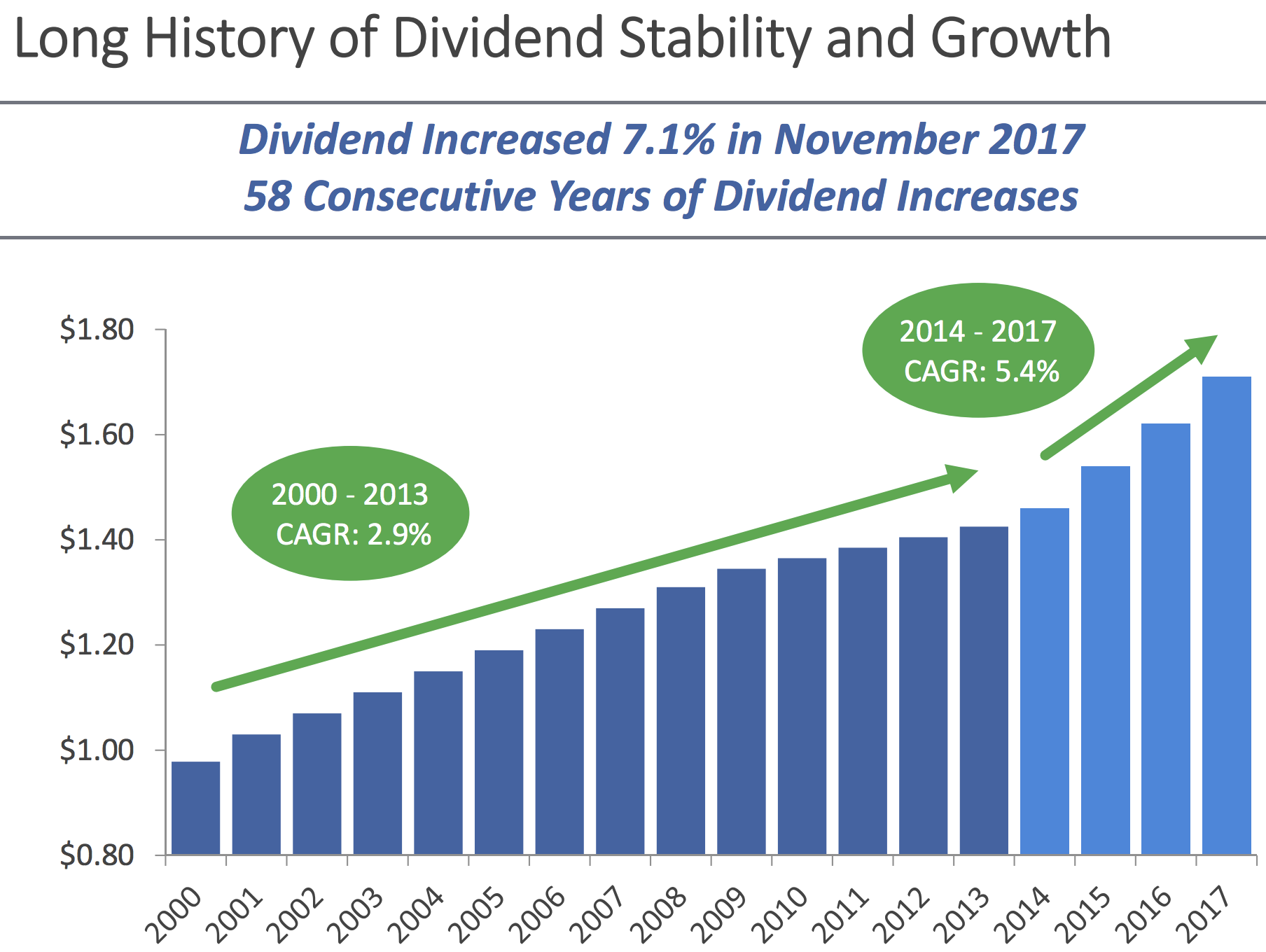

All said, Vectren’s blend of regulated utility and non-utility business, along with favorable oversight by regulators, has meant the company has been an extremely reliable dividend payer. In fact, Vectren has increased its dividend for 58 consecutive years, including a 7.1% boost in 2017.

Management continues to run the business very conservatively, ensuring Vectren maintains its solid investment grade credit rating and limits its dividend to 70% of its stable utility earnings (company-wide payout ratio is targeted at 60% to 65%).

Source: Vectren Investor Presentation

Key Risks

There’s little to be said about the stability of Vectren’s utility business. As a regulated monopoly, it has few competitors and enjoys undisturbed profits year in and year out.

What’s less certain, though, is whether Vectren can meet expectations to sustain its recent high rate of growth. If it can’t, the stock will likely disappoint.

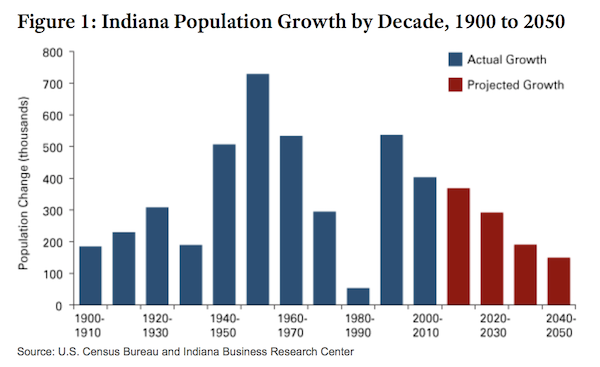

Like all businesses, Vectren makes more money when the company sells to more customers. Vectren’s customers are the populations of Indiana and Ohio, both of which are forecasted to slow in growth.

Indiana’s rate of growth is forecasted to slow substantially over the next few decades.

And Ohio’s population has all but flattened in recent years.

Source: Ohio Development Services Agency

Decelerating population growth in Vectren’s service areas won’t likely impact the company in the short-term, but it may eventually put the brakes on the company’s current trend of higher growth.

Another obstacle to growth is energy efficiency. New lightbulbs, energy-efficient appliances, and other innovations may curtail the average person’s use of electricity.

In fact, the Energy Information Administration (a U.S. federal agency) projects that electricity use in U.S. households will rise 0.7% per year through 2040, a far cry from the 8% annual growth seen in past decades.

Should renewable energy sources become more cost effective and widely adopted, the very nature of today's regulated utility business model could also have to meaningfully evolve.

Another risk to consider is that Vectren’s non-utility business accounts for 20% of revenue, a larger percentage of sales than the non-utility businesses of most other utility companies we’ve researched.

This unregulated, non-utility business is competitive and cyclical, leaving Vectren more—though not much more—vulnerable to recession than some utility companies.

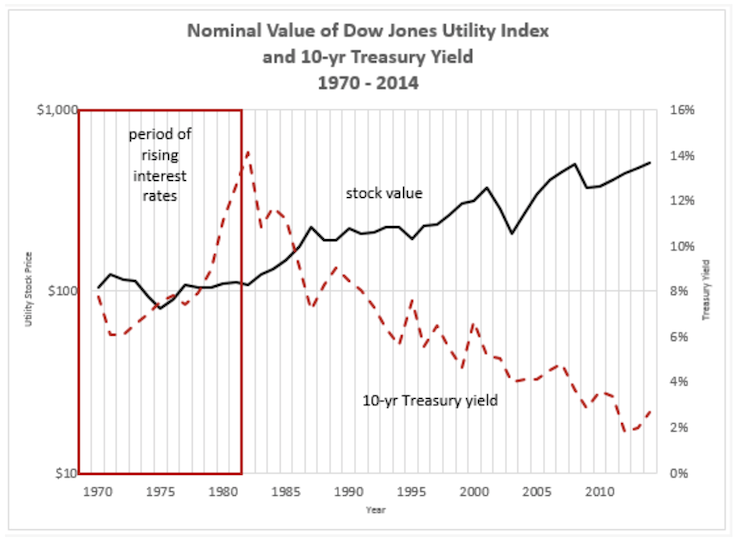

Finally, no analysis of a utility company these days is complete without a discussion on the implications of rising interest rates, which are expected to continue moving higher based on the Fed's latest projections (although certainly no one has a crystal ball on this issue).

If interest rates rise, bond yields will follow. Since utility stocks are often viewed as bond alternatives because of their high dividend yields and stability, investors may choose to sell their shares of utility companies and instead invest in bonds.

Share prices will naturally fall over the short term if investors lose their appetite for utility stocks. In the extreme case, investors of utility companies may witness flat or declining share prices, as they did during the 1970s when interest rates were on the rise.

Source: Berkeley Lab

From a fundamental perspective, higher interest rates raise the cost of debt and equity capital for utilities. Many utility companies depends on tapping capital markets to fund their growth projects, Vectren included.

Fortunately, this risk doesn't seem to be a big concern for the company. Vectren maintains a strong investment grade credit rating to keep its borrowing costs low, almost all of its existing debt has fixed interest rates, and cash flow from operations is expected to fund the bulk of the growth investments it has planned.

The bigger issues to consider seem to be management's ability to continue delivering its planned projects on time and on budget (especially the $900 million gas-fired plant), as well as the company's concentration in just two states, which makes it more sensitive to any unexpected regulatory changes or economic developments in those territories.

In sum, there seem to be few obstacles to a profitable long-term future for Vectren. So long as the regulatory environments remain stable in Indiana and Ohio, and the business continues delivering on its growth projects, Vectren's future appears to remain bright.

Closing Thoughts on Vectren

Vectren has many of the qualities investors seek in retirement: a (stellar) track record of paying safe dividends, moderate growth potential, very predictable earnings and resistance to recession.

The biggest obstacle today is the stock's relatively low dividend yield, which likely reflects the low interest rate environment we have been living in, as well as Vectren's impressive growth potential (for a utility).

All things considered, Vectren appears to be a quality business with a solid dividend profile, making it a worthwhile investment candidate to monitor.