In May 2019 we analyzed a short-seller's bearish report on the company here.

A.O. Smith (AOS) was founded in 1874 and manufactures residential and commercial gas and electric water heaters, boilers, and water treatment products that are sold in over 60 countries around the world.

The company's water heaters are sold to residences, restaurants, hotels, office buildings, laundromats, car washes, and other small businesses. It also produces residential and commercial boilers for use in space heating applications for hospitals, schools, hotels, and other large commercial buildings. And its water treatment products, including filtration bottles, water softeners, and water filtrations, are used in residences, restaurants, hotels, and offices.

A.O. Smith also produces food and beverage filtration products, expansion tanks, commercial solar water heating systems, swimming pool and spa heaters, solar units, and air purification products.

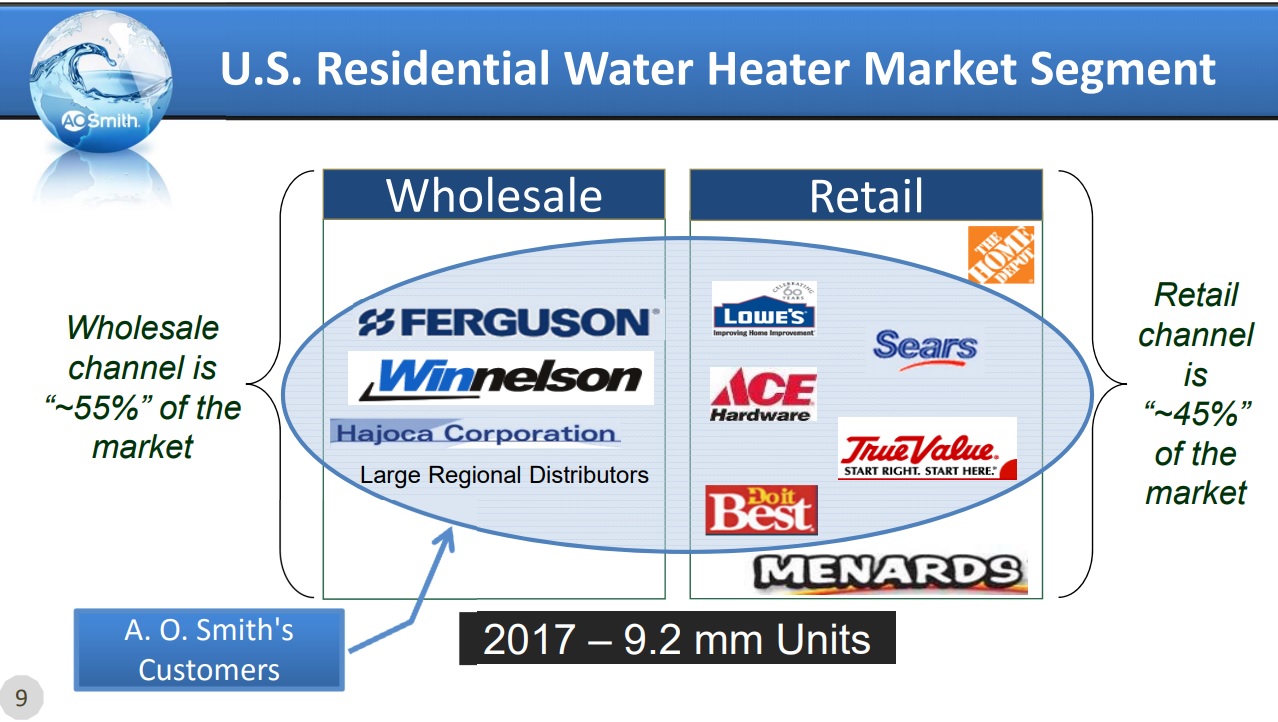

The company distributes its products through independent wholesale plumbing distributors (1,300 in North America), as well as through retail channels consisting of hardware and home center chains. In the U.S., the company's water heater sales are 55% wholesale and 45% retail store chains.

Source: A.O. Smith Investor Presentation

A.O. Smith has two reporting segments:

North America: 64% of 2017 sales (growing mid to high single-digits)

Rest Of World: 36% of 2017 sales (growing low to mid-double-digits)

The company's overall geographic sales breakdown looks like this:

U.S.: 43%

Canada: 20%

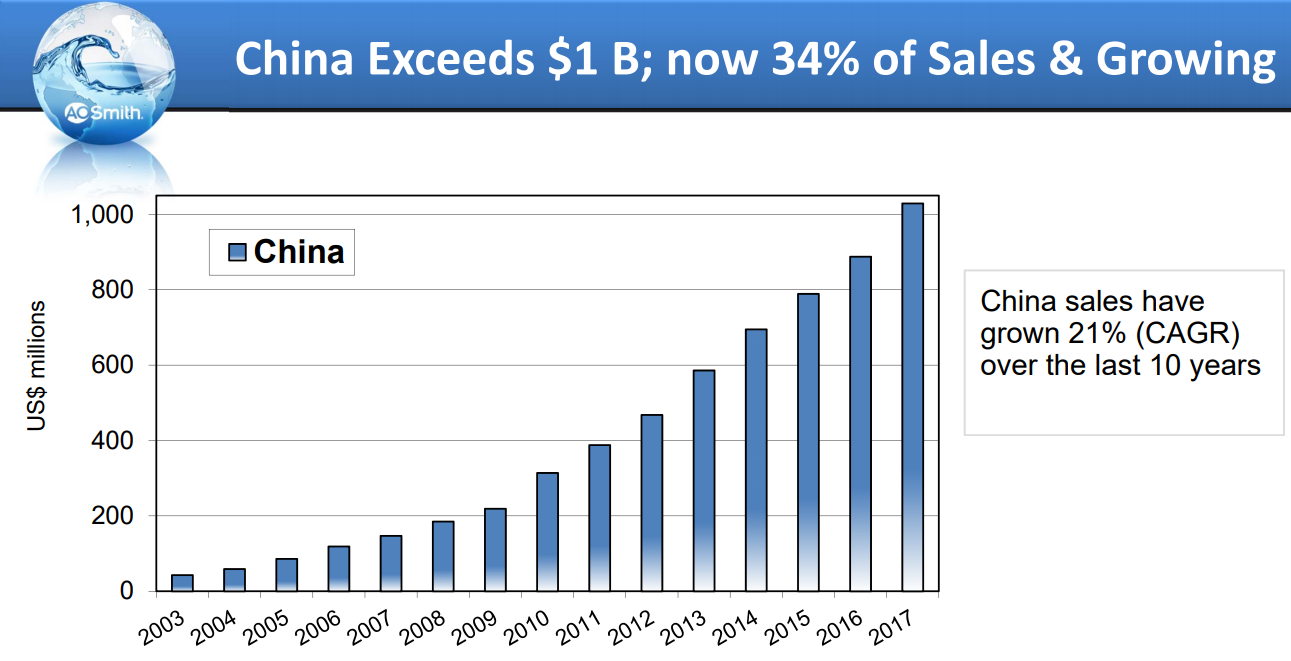

China: 34%

Europe/Middle East: 5%

India: less than 1%

While the vast majority of sales are still from North America, the much faster growth rate of its international sales (especially in China and India) means that A.O. Smith is quickly diversifying by geography.

With 25 consecutive annual dividend increases, A.O. Smith is a dividend aristocrat.

Business Analysis

A.O. Smith is one of those small industrial companies that flies under the radar despite having generated incredible growth in its top and bottom lines over the years. For example, since 2010 the company has recorded:

Sales growth: 10.5% annually

Adjusted EBITDA growth: 21% annually

Adjusted EPS growth: 26% annually

Free cash flow growth: 22% annually

Dividend growth: 24% annually

In fact, over the past 25 years A.O Smith has safely and sustainably grown its dividend by 11.4% per year while rewarding investors with annualized total returns of 16.8%. What's the secret to A.O. Smith's success? The company's strong dominance in its core niche markets of water heaters, commercial boilers, and water purifiers.

A.O. Smith has spent over 100 years carefully building up its core brands and forming great relationships with over 1,300 distributors in North America. The company spends about 3% of its sales on R&D to continually improve the quality of its products, specifically their thermal efficiency (how much energy is used to heat the water versus lost to the environment). The company also prides itself on the reliability and durability of its heaters and boilers.

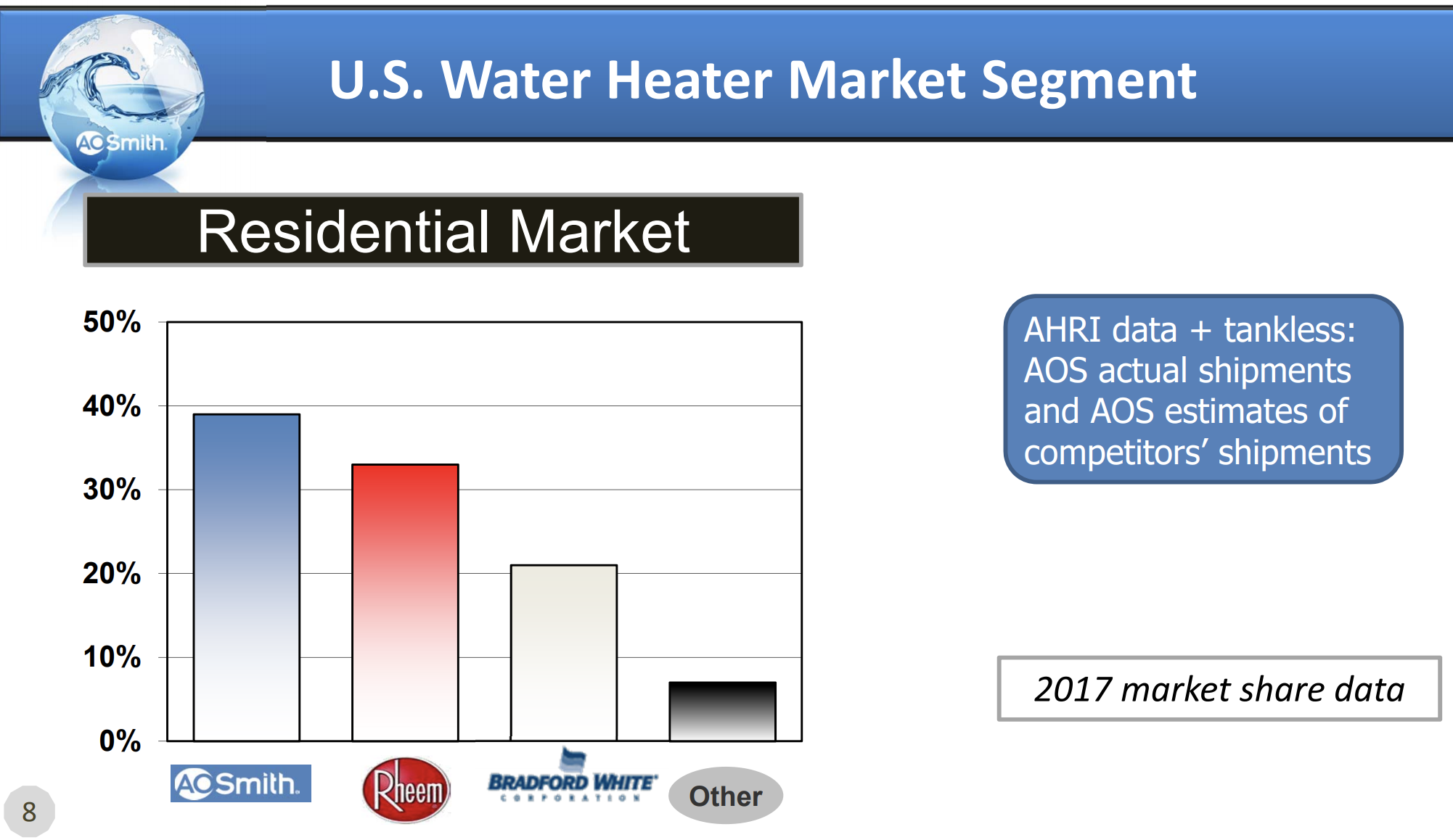

This is why today A.O. Smith is the largest water heater manufacturer in America with almost 40% market share in the U.S. residential market.

Source: A.O. Smith Investor Presentation

In the U.S. commercial market, the company has over 50% market share thanks to its Cyclone water heater which it introduced in 1997. This is the most energy efficient product on the market with 96% thermal efficiency. The Cyclone is so popular it makes up 63% of the company's commercial business in the U.S.

Source: A.O. Smith Investor Presentation

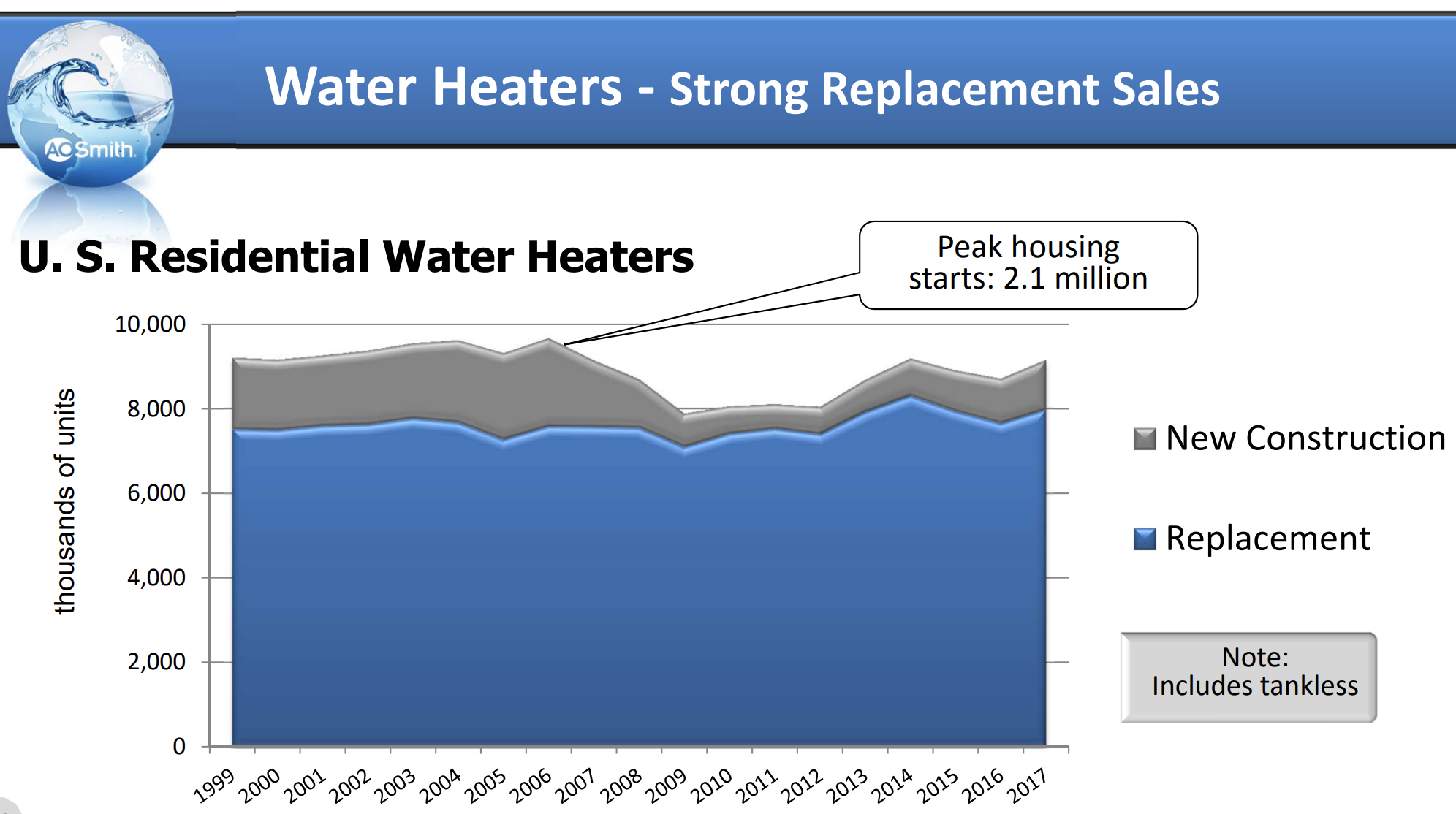

Competitors have a hard time taking meaningful market share from A.O. Smith due to the mature nature of the water heater market. Water heaters need to be replaced every 8 to 12 years, and customers have few reasons to switch suppliers if they are happy with the quality, performance, and price of A.O. Smith's solutions. As a result, the company enjoys substantial replacement sales, which account for the vast majority of the U.S. residential water heater market due to the country's relatively slow population and construction growth.

Source: A.O. Smith Investor Presentation

In the U.S. the company recently expanded into the water purification market via bolt-on acquisitions such as Aquasana ($87 million) and Hague ($45 million). A.O. Smith's North American water treatment business generated $16 million in 2016 sales but more than tripled in 2017 to reach $57 million. While that is just 2% of the company's current sales, the size of the new market and its stronger growth profile make it a compelling long-term opportunity for the business.

However, the real growth driver for A.O. Smith has come from its efforts to deploy its leading water treatment technologies in fast-growing emerging markets, especially China and India.

In China, where the company has been operating for over 20 years and was one of the first U. S. water heater manufacturers to enter the market, A.O. Smith sells water heaters in 8,000 retail locations, including 2,900 on an exclusive basis. Its water purification and air purification systems are sold in more than 7,400 and 3,500 retail locations, respectively. The company also has a fast growing e-commerce business in the country that generated $250 million in 2017 sales (8.3% of total company revenue).

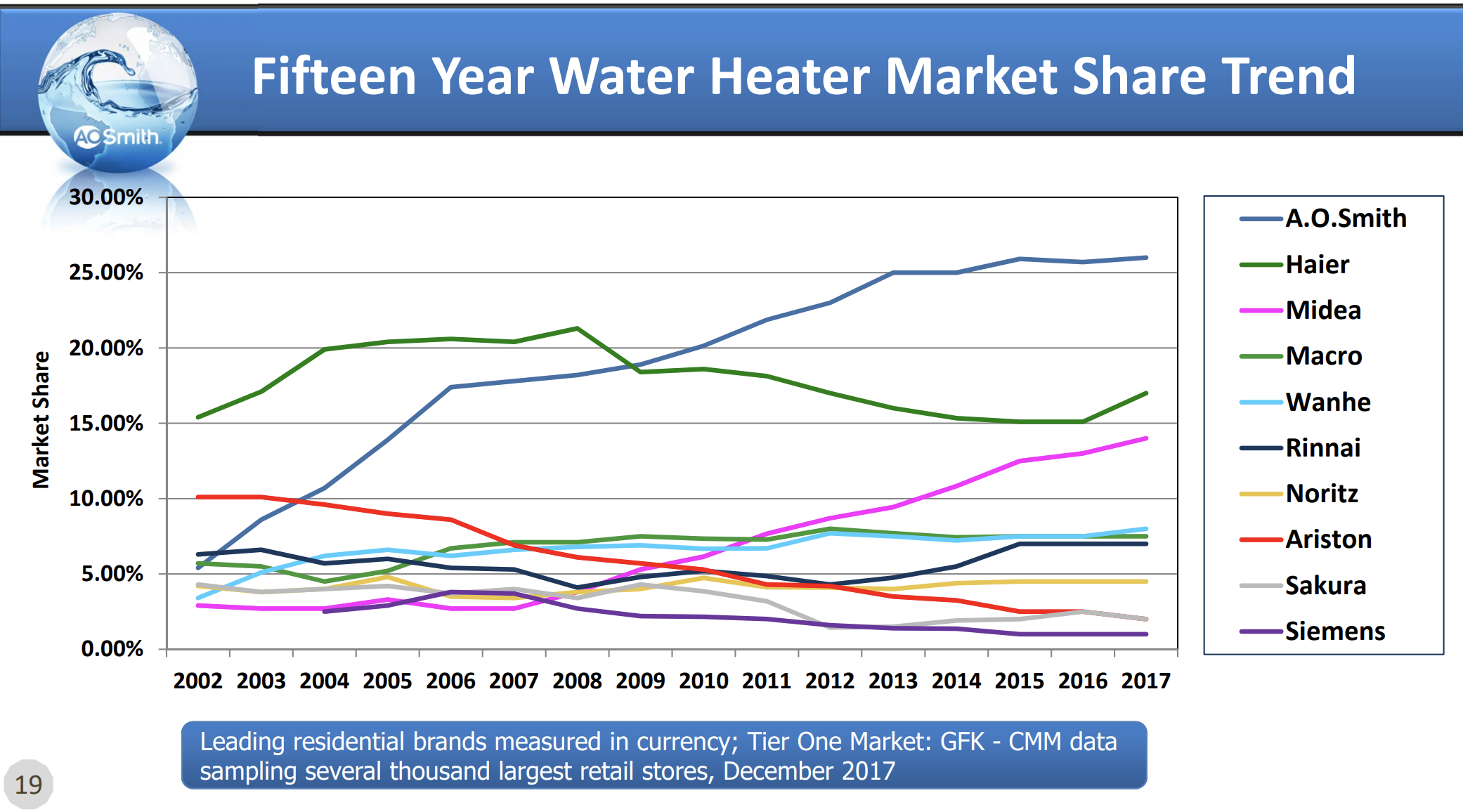

As you can see below, A.O. Smith is seeing booming sales in all of its key products in China thanks to the rapid growth in the country's middle class, which can increasingly afford water heaters, water treatment systems, and air purifiers. In fact, by 2020 it's projected that China's middle class alone with total about 600 million people, nearly double the population of the U.S.

Source: A.O. Smith Investor Presentation

While many American businesses have failed to replicate their success in China, you can see that A.O. Smith has steadily taken market share over the past 15 years. And while China is soon to become A.O. Smith's largest market, the company also has incredible growth potential in India.

Source: A.O. Smith Investor Presentation

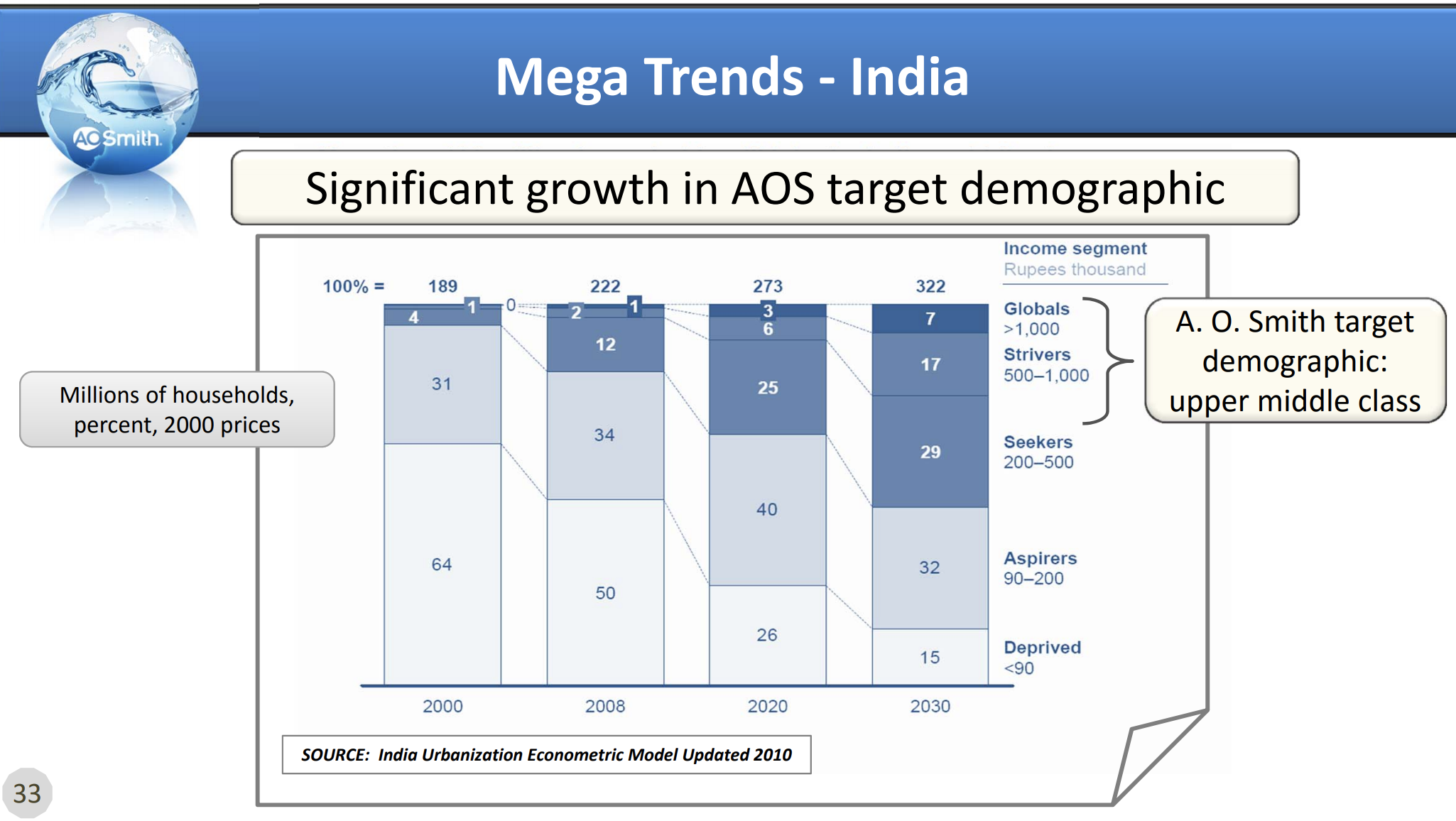

In 2008, A.O. Smith established its first office in India, becoming the first U. S. water heater company to serve the Indian market. The firm began building and selling water heaters and water treatment products in 2010 and 2015, respectively. In 2017, India sales grew 44% to $26 million, or about 1% of total sales.

However, fast growth in India is likely to continue thanks to the country's population growth, especially of its middle class.

Source: A.O. Smith Investor Presentation

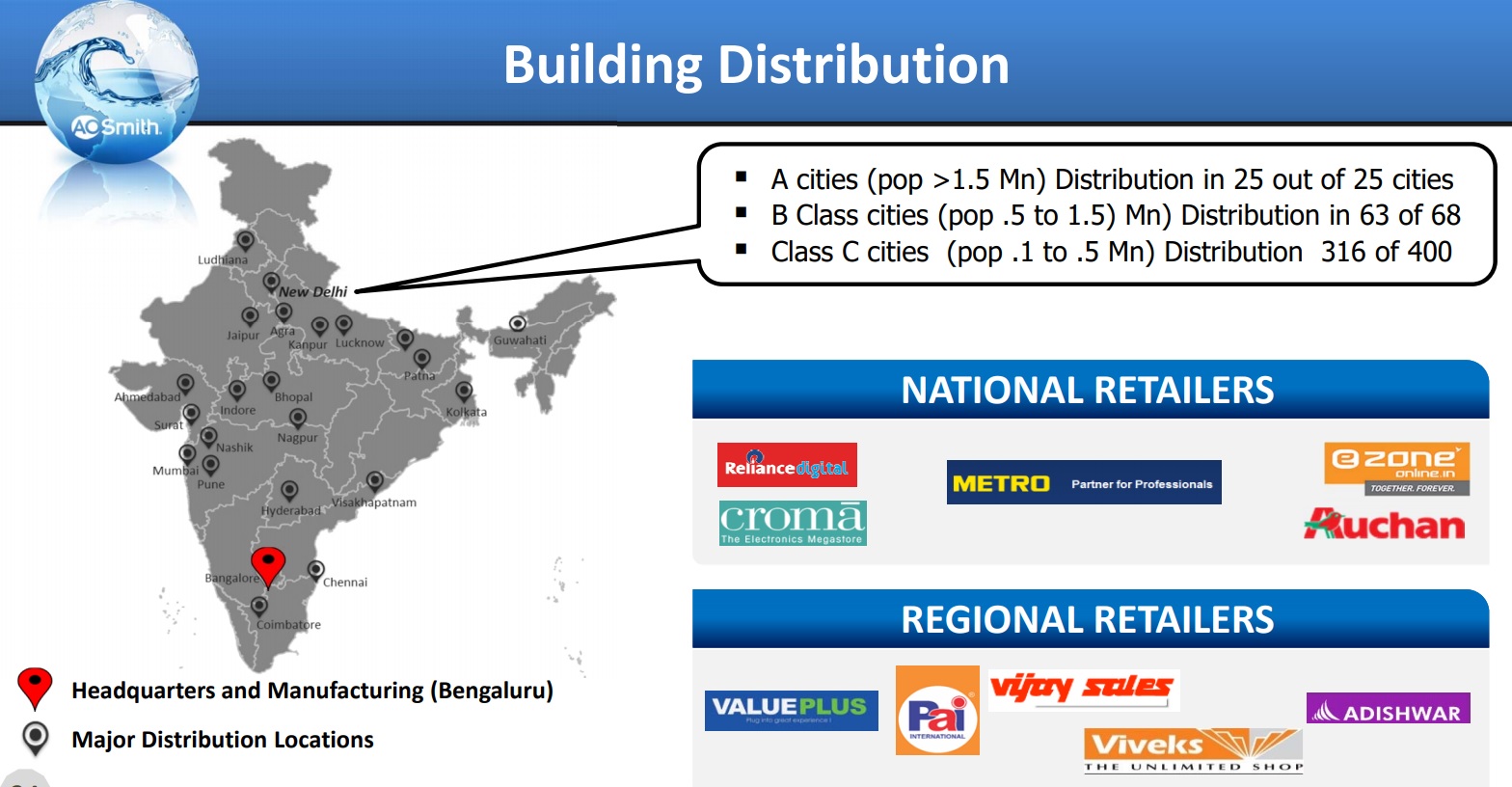

A.O. Smith is poised to see China-like growth rates in India thanks to its already extensive and fast-growing distribution chain in that country. One that includes a presence in the largest 25 cities and strong relationships with the top retailers in India (the country's equivalent to Lowe's and Home Depot).

Source: A.O. Smith Investor Presentation

However, there is more to A.O. Smith's investment thesis than just strong top line growth. Ultimately, it's the bottom line, specifically free cash flow, that pays for sustainable and fast-growing dividends.

Fortunately, A.O. Smith enjoys stellar profitability. The firm generates an operating margin north of 15%, a return on invested capital near 25%, and a free cash flow margin near 10%.

Note that A.O Smith's free cash flow margin would be much higher (about 12.5% or so), but management is greatly increasing spending in India and China to increase manufacturing capacity and continue building its distribution networks. However, the fact that the company's return on invested capital is still double that of most industrial peers shows that A.O. Smith's capital allocation plans have been a big success.

Good capital allocation is one reason the company's profitability is so high, but strong pricing power is another. This is both due to the long-standing relationships A.O. Smith has with its commercial clients (often lasting decades), and the fact that its products are the most efficient and thus cheapest to operate in the long term. Finally, there's the company's strong economies of scale, with A.O. Smith being able to source its inputs from all over the world as well as buy in bulk as the largest player in most of its markets, thus lowering its unit costs.

Running such a fast-growing operation, all while tripling operating margins over the past decade, takes incredible skill. That is provided by A.O, Smith's CEO Ajita Rajendra, who has been with the company for 13 years and is just the 9th chief executive in the company's 144-year history (average CEO tenure 16 years). Mr. Rajendra took over the top spot in 2014 after serving as COO. In total he has 40 years of industry experience, particularly in operating in fast-growing overseas and emerging markets.

In other words, A.O. Smith is well-positioned to benefit from the rise in demand for its products in the world's two largest countries. To help ensure it has the capital to execute on its plans, A.O Smith enjoys one of the industry's top balance sheets. In fact, A.O. Smith is one of the few industrial companies with more cash than debt on its balance sheet.

Combined with its relatively low payout ratio, A.O. Smith has one of the safest dividends on Wall Street while leaving management with plenty of access to capital to continue the company's growth plans.

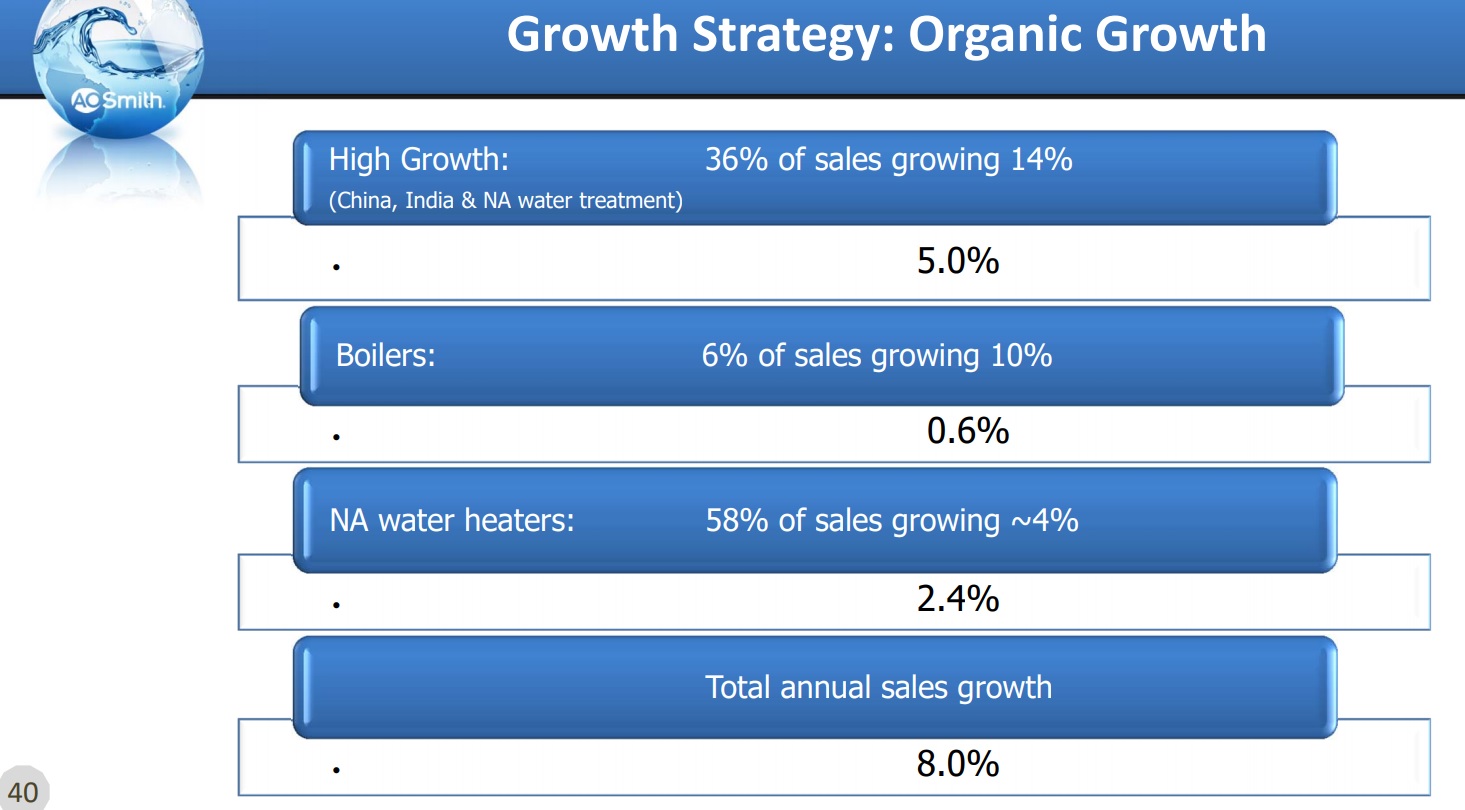

Going forward, A.O. Smith expects to achieve 8% long-term organic growth thanks mainly to the company's dominance in the Chinese market (A.O. Smith has #1 market share in both North America and China) and numerous other major growth markets.

Source: A.O. Smith Investor Presentation

If the company can achieve its sales growth target, A.O. Smith is likely to achieve low double-digit EPS growth given the operating leverage in its business model and continued share buybacks.

While all long-term forecasts need to be taken with a grain of salt, given A.O. Smith's track record thus far and long growth runway in three major growth markets, management's growth projections appear reasonable. As a result, A.O. Smith's dividend could also grow around 11% to 12% annually over the next decade, making it one of the fastest growing dividend aristocrats.

Key Risks

There are four risks to keep in mind with A.O. Smith.

First, this is still a relatively small company with just $3 billion in sales. Much of A.O. Smith's business is highly concentrated with just a few large commercial customers. For example, in 2017 the firm's top five commercial clients made up 38% of revenue, creating the potential for significant revenue loss should one or more of those decide to switch to a rival's products.

Next, be aware that A.O. Smith is exposed to volatile raw material input costs (most notably steel). With the U.S. now imposing 25% steel tariffs, the company could experience significant short-term margin compression for as long as the tariffs remain in effect. However, this issue seems unlikely to impact the firm's long-term earnings power.

The largest potential risk over the short term is also trade related, specifically that if the U.S. and China end up in a full-blown trade ware, then A.O. Smith could potentially face major growth challenges. After all, China is its most important market by far. For example, if China imposes 25% tariffs on its products, that would put A.O. Smith at a distinct disadvantage to its many local rivals in China.

And even if a trade war is averted, the fact that so much of A.O. Smith's future revenue will be coming from China and India (over 50% within a few years) means the company will be exposed to significant currency risk. If the U.S. dollar appreciates against the Chinese Renminbi or Indian Rupee, sales in those markets will translate into fewer U.S. dollars and create growth headwinds for its bottom line, which could also mean slower dividend growth.

Finally, A.O. Smith's business can also be affected over the short term by changes in new construction activity, especially in North America. New buildings require water heaters, which boosts demand for A.O. Smith's products when construction markets are healthy. However, the opposite is also true. Fortunately, A.O. Smith's domestic operations benefit from a large replacement market, which results in somewhat steadier cash flow over a full cycle compared to many other industrial companies.

Closing Thoughts on A.O. Smith

The industrial sector is full of little-known companies with strong dividend growth track records, and A.O. Smith is one of the most impressive. The firm's corporate culture is highly conservative where it should be (safe balance sheet, avoiding large acquisitions), but aggressive where it counts (profitably expanding into fast-growing markets with leading water treatment technologies).

Thanks to the company's long track record of engineering innovation, broad portfolio of trusted brands, global distribution network, and strong economies of scale, A.O. Smith is likely to see significant top and bottom line growth for years to come. That, in turn, spells great news for long-term income investors who are likely to enjoy double-digit dividend increases for the foreseeable future.